4/2/20

Two months ago a short selling research firm alleged that there was misreporting of financials at the Chinese coffee giant, Luckin Coffee. The company denied the report as unsubstantiated speculation with malicious intent.

This morning the company reported that it has suspended its COO and several other employees for misconduct related to fabricating transactions. These are precisely the claims that were made two months ago.

The stock was down more than 80% this morning.

Who was the biggest loser?

It’s the top shareholder and angel investor in Luckin, the Chinese billionaire Lu Zhengyao.

Zhengyao is a serial entrepreneur. He founded the rental car company Car Inc. in 2007 and took it public in 2014 on the Hong Kong Stock Exchange. His former COO is credited with founding the Starbucks competitor, Luckin Coffee in 2017. In 2019, the company IPO’d on the Nasdaq.

Zhengyao was the angel investor behind the company and holds 484 million shares. At yesterday’s close, that stake was valued at over $12 billion. At the lows this morning, it was valued at $2.2 billion. Learn more about the stakes of billionaire investors here.

April 23, 5:00 pm EST

Yields continue to grind higher toward 3%. That has put some pressure on stocks, despite what continues to be a phenomenal earnings season. This creates another dip to buy.

Yesterday, we talked about a reason that people feel less good about stocks, with yields heading toward 3%. [Concern #1] It conjures up memories of the “taper tantrum” of 2013-2014. Yields soared, and stocks had a series of slides.

My rebuttal: The domestic and global economies are fundamentally stronger and much more stable. But maybe most importantly, the economy (still) isn’t left to stand on its own two feet, to survive (or die) in a normalizing interest rate environment. We have fiscal stimulus doing a lot of heavy lifting.

Let’s look at a couple of other reasons people are concerned about stocks as yields climb:

[Concern #2] Maybe this is the beginning of a sharp run higher in market interest rates — like 3% quickly becomes 4%?

My Rebuttal: Very unlikely given the global inflation picture, but more unlikely with the Bank of Japan still buying up global assets in unlimited amounts (Treasuries among them, through a variety of instruments). They can/and are controlling the pace, for the benefit of stimulating their own economy and for the benefit of stimulating and maintaining stability in, the global economy.

[Concern #3] I hear the chatter about how a 3% 10-year note suddenly creates a high appetite for Treasuries over stocks at this point, especially from a risk-reward perspective (i.e. people are selling stocks in favor of capturing that scrumptious 3% yield).

My Rebuttal: In this post-crisis environment, a rise toward 3% promotes the exact opposite behavior. If you are willing to lend for 10-years locked in at a paltry rate, you are forgoing what is almost certainly going to be a higher rate decade than the past decade. If you need to exit, you’re going to find the price of your bonds (very likely) dramatically lower down the road. Coming out of a zero-interest rate world, bond prices are going lower/not higher.

Remember this chart …

The bond market has become a high risk-low reward investment. Meanwhile, with earnings set to grow more than 20% this year, and stock prices already down 7% from the highs of the year, we have a P/E on stocks that continues to slide lower and lower, making stocks cheaper and cheaper. That makes stocks a far superior risk/reward investment, relative to bonds – especially with the prospects of the first big bounce back in economic growth we’ve seen since the Great Recession.

If you are hunting for the right stocks to buy on this dip, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers.

May 19, 2017, 4:00pm EST Invest Alongside Billionaires For $297/Qtr

| Stocks continue to bounce back today. But the technical breakdown of the Trump Trend on Wednesday

still looks intact. As I said on Wednesday, this looks like a technical correction in stocks (even considering today’s bounce), not a fundamental crisis-driven sell-off.

With that in mind, let’s take a look at the charts on key markets as we head into the weekend.

Here’s a look at the S&P 500 chart….

For technicians, this is a classic “break-comeback” … where the previous trendline support becomes resistance. That means today’s highs were a great spot to sell against, as it bumped up against this trendline.

Very much like the chart above, the dollar had a big trend break on Wednesday, and then aggressively reversed Thursday, only to follow through on the trend break to end the week, closing on the lows.

On that note, the biggest contributor to the weakness in the dollar index, is the strength in the euro (next chart).

The euro had everything including the kitchen sink thrown at it and it still could muster a run toward parity. If it can’t go lower with an onslaught of events that kept threatening the existence of the euro, then any sign of that clearing, it will go higher. With the French elections past, and optimism that U.S. growth initiatives will spur global growth (namely recovery in Europe), then the European Central Bank’s next move will likely be toward exit of QE and extraordinary monetary policies, not going deeper. With that, the euro looks like it can go much higher. That means a lower dollar. And it means, European stocks look like, maybe, the best buy in global stocks.

A lower dollar should be good for gold. As I’ve said, if Trump policies come to fruition, inflation could get a pop. And that’s bullish for gold. If Trump policies don’t come to fruition, the U.S. and global growth looks grim, as does the post-financial crisis recovery in general. That’s bullish for gold.

This big trendline in gold continues to look like a break is coming and higher gold prices are coming.

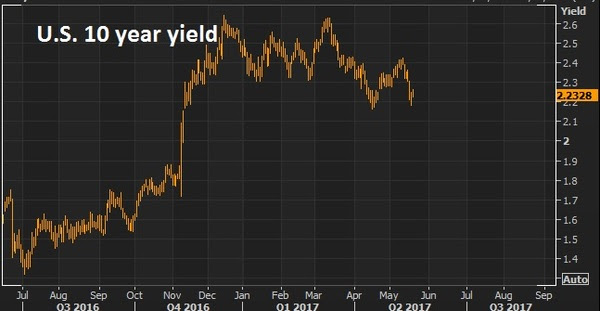

With all of the above, the most important chart of the week is probably this one …

The 10 year yield has come all the way back to 2.20%. The best reason to wish for a technical correction in stocks, is not to buy the dip (which is a good one), but so that the pressure comes out of the interest rate market (and off of the Fed). The run in the stock market has clearly had an effect on Fed policy. And the Fed has been walking rates up to a point that could choke off the existing economic recovery momentum and, worse, neutralize the impact of any fiscal stimulus to come. Stable, low rates are key to get the full punch out of pro-growth policies, given the 10 year economic malaise we’re coming out of. Invitation to my daily readers: Join my premium service members at Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse portfolio of the most high potential stocks.

|

May 11, 2017, 4:00pm EST Invest Alongside Billionaires For $297/Qtr

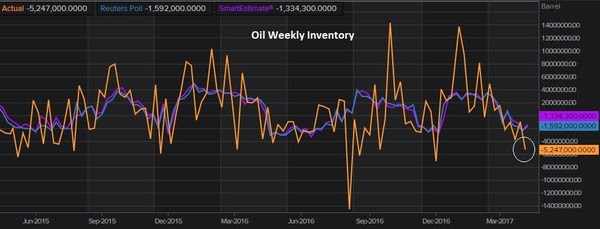

| Oil has been on the move the past few days. Was this recent dip a gift to buy?The oil inventory report yesterday showed a big drawdown on oil inventories. The market expectation was for about a drawdown of 1.5 million barrels. It came in at 5 million.

That has oil on a big bounce for the week. It’s trading about 8% higher than it was at the lows of last Friday. But we still sit below the 200 day moving average and below the key $50 level (the comfort zone for those producers, namely the shale industry, to fire back up idle capacity).

The weakness in oil has a lot to do with weakness across broader commodities. And broader commodities typically correlates well with what Chinese stocks are doing.

You can see in the chart above, how closely the two track. This bottom in commodities has/had everything to do with the outlook for a big infrastructure spend out of the Trump administration. It’s yet to bubble up toward the top of the action list. With that, the momentum has either stalled on this trade, or it’s a pause before another leg higher in this early stage multi-year rebound. My bet is on the latter.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Join us today and get our full recommendation on this stock, and get your portfolio in line with our BILLIONAIRE’S PORTFOLIO. |

May 10, 2017, 4:00pm EST Invest Alongside Billionaires For $297/Qtr

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine. As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

Those that oppose it warn that it will lead to another financial crisis. On that note, I want to revisit my take from earlier this year on the cause of the crisis that almost destroyed the global economy.

“With all of the complexities of the housing bubble and the subsequent global financial crisis, it can seem like a web of deceit. But it all boils down to one simple actor. It wasn’t Wall Street. It wasn’t hedge funds. It wasn’t mortgage brokers. These entities were operating, in large part, from the natural force of economics: incentives.

It wasn’t even the government’s initiative to promote home ownership that led to the proliferation of mortgages being given to those that couldn’t afford them.

So who was the culprit?

It was the ratings agencies.

Housing prices were driven sky high by the availability of mortgages. Mortgages were made easily available because the demand to invest in mortgages, to fund those mortgages, was sky high.

But what drove that demand to such high levels?

When the mortgages were combined together in a package (securitized as a mix of good mortgages, and a lot of bad/higher yielding mortgages), they were bought, hand over fist, by the massive multi-trillion dollar pension industry, banks and insurance companies. Yes, the guys that are managing your pension funds, deposit accounts and insurance policies were gobbling up these mortgage securities as fast as they could, but ONLY because the ratings agencies were stamping them all with a top AAA rating. Who would encourage such a thing? Congress. In 1984 they passed a law making it okay for banks, pension funds and insurance companies to buy/treat high rated secondary mortgages like they would U.S. Treasuries.

So as investment managers, in the business of building the best performing risk-adjusted portfolio possible, and in direct competition with their peers, they couldn’t afford NOT to buy these securities. They came with the safest ratings, and with juicy returns. If you don’t buy these, you’re fired.

To put it all very simply, if these securities were not AAA rated, the pension funds would not have touched them (certainly not to the extent). With that, if the there’s no appetite to fund the mortgages (no money chasing it), then the ultra-easy lending practices never happen, and housing prices never skyrocket on unwarranted and unsustainable demand. The housing bubble doesn’t build, doesn’t bust, and the financial crisis doesn’t happen.

That begs the question: Why did the ratings agencies give a top rating to a security that should have received a lower rating, if not much lower?

First, it’s important to understand that the ratings agencies get paid on the products they rate BY the institutions that create them. That’s right. That’s their revenue model. And only a group of these agencies are endorsed by the government, so that, in many cases, regulatory compliance on a financial product requires a rating from one of these endorsed agencies.”

Keep this in mind as the fear mongering over the talk of repeal of rework of Dodd Frank heats up.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Join us today and get our full recommendation on this stock, and get your portfolio in line with our BILLIONAIRE’S PORTFOLIO.

|

January 25, 2017, 1:30pm EST Invest Alongside Billionaires For $297/Qtr

The Dow broke 20,000 today. I want to talk about why it’s a big deal.

As we discussed when we entered the new year, “Trump’s Plan Is A Recipe For Restoring Animal Spirits.” Watch out, it’s coming.

Remember, this (animal spirits) is the element that economists and analysts can’t predict, and can’t quantify. It’s not in the forecasts. This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mistrust of the system. All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset has been underway since the night of the election. And that gives way to a return of animal spirits.

Higher stock prices tend to beget higher stock prices. Trust me, individual investors that haven’t been believers will be calling their financial advisors and logging in to their online brokerage accounts over the coming days. Institutional investors that haven’t been believers, that have been underweight stocks, will be beefing up exposure if they want to compete with their peers (and keep their jobs).

And not only do higher stock prices lead to higher stock prices, but higher stock prices tend to make people feel more confident about the economy, which begets a better economy.

Add to this, the psychological value of Dow 20,000 could finally be a turning point in the divergence of sentiment toward the Trump Presidency. It may serve as a validation marker for those that have been on the fence. And for those in opposition, as I’ve said before, growth solves a lot of problems! When the college grad that’s been relegated to a 10-year career as a barista begins to see signs of opportunity for a better career and a better future, in a stronger economy, the sands of Trump sentiment can shift quickly.

Cleary, Trump entered with a game plan that can pop economic growth. And he’s going 100 miles an hour at executing on that plan. For markets, what he’s doing is creating a sense of certainty for investors. They know what he’s promised, and now they know that he appears to intend on delivering on those promises. And the coordination of growth policies, along with ultra-easy monetary policy (even with tightening in view) serves as risk mitigators for markets. It should limit downside risk, which is what investors care most about. How?

Remember, even at Dow 20,000, stocks are still extremely cheap.

Here’s a review on why …

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 48% by the middle of this year. We’re still making up for the lost growth of the past decade. And there’s a lot of ground to make up.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year. That’s an S&P 500 earnings estimate of $133.64 times a P/E of 20 equals 2,672 on the S&P 500.

Reason #3: The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 37% higher.

With this in mind, we are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

This past week we’ve talked about the recent public disclosures made about the investments of some of the world’s best investors.

The biggest news was Warren Buffett’s new $1 billion plus stake in Apple.

Apple’s stock price peaked in April of last year (following a 65% rolling 12-month return). Much of that run up was driven by activist efforts of Carl Icahn. Icahn influenced sentiment in the stock, but also influenced value creation for shareholders by pressuring Apple management to buy back stock.

But since peaking last April (2015), Apple shares had lost nearly 34% as of earlier this month. Icahn dumped his stake and made it public in late April.

And then we find this past week that Buffett is now long (he’s in).

So should you follow Buffett? Is it the bottom for Apple? And what makes Apple a classic Buffett stock?

First, Buffett has compounded money at 19.2% annualized over a 50 year period. That’s made him the second wealthiest man in the world.

Buffett loves to buy low. He has a long and successful record of buying when everyone else is selling. Buffett purchased his Apple stake last quarter when Apple was near its 52-week low.

But he famously stays away from technology. Why Apple? For Buffett, Apple is a global, dominant brand. That trumps sector. He loves brand name companies with a loyal customer base, and there is probably no company on the planet with a more loyal customer base then Apple. Plus, one could argue that Apple is a consumer services company (with 700 million credit cards on file, charging customers for movies, songs, apps …).

Generally Buffett pays less than 12 times earnings for a company. Of course there are exceptions, but Apple fits this criterion perfectly with a P/E of 10.

Buffett loves companies that have a high return-on-invested-capital (ROIC) and low debt. Apple has an ROIC of 28%, extremely high. Companies with a high ROIC usually have a “wide moat” or a competitive advantage over the rest of the world. That gives them pricing power to drive wide margins.

Apple really is the classic Buffett stock. And now that Buffett has put his stamp of approval on Apple, we believe the stock has bottomed, especially since it’s so cheap compared to the overall stock market. And he’s not the only billionaire value investor who loves Apple. Billionaire hedge fund manager David Einhorn also loves Apple. He increased his Apple stake last quarter to 15% of his entire hedge fund, almost $900 million dollars worth.

Don’t Miss Out On This Stock

In our Billionaire’s Portfolio we followed the number one performing hedge fund on the planet into a stock that has the potential to triple by the end of the month.

This fund returned an incredible 52% last year, while the S&P 500 was flat. And since 1999, they’ve done 40% a year. And they’ve done it without one losing year. For perspective, that takes every $100,000 to $30 million.

We want you on board. To find out the name of this hedge fund, the stock we followed them into, and the catalyst that could cause the stock to triple by the end of the month, click here and join us in our Billionaire’s Portfolio.

We make investing easy. We follow the guys with the power and the influence to control their own destiny – and a record of unmatchable success. And you come along for the ride.

We look forward to welcoming you aboard!