Today I want to take a look back at my March 7th Pro Perspectives piece. And then I want to talk about why a power shift in the economy may be underway (again).

Big Picture .. Market Perspectives March 7, 2017

“A big component to the rise of Internet 2.0 was the election of Barack Obama. With a change in administration as a catalyst, the question is: Is this chapter of the boom in Silicon Valley over? And is Snap the first sign?

Without question, the Obama administration was very friendly to the new emerging technology industry. One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007, before Obama announced his run for president, and just as Facebook was taking off after moving to and raising money in Silicon Valley (with ten million users). Facebook was an app for college students and had just been opened up to high school students in the months prior to Obama’s run and the hiring of the former Facebook cofounder. There was already a more successful version of Facebook at the time called MySpace. But clearly the election catapulted Facebook over MySpace with a very influential Facebook insider at work. And Facebook continued to get heavy endorsements throughout the administration’s eight years.

In 2008, the DNC convention in Denver gave birth to Airbnb. There was nothing new about advertising rentals online. But four years later, after the 2008 Obama win, Airbnb was a company with a $1 billion private market valuation, through funding from Silicon Valley venture capitalists. CNN called it the billion dollar startup born out of the DNC.

Where did the money come from that flowed so heavily into Silicon Valley? By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S.

When institutional investors see that kind of money flowing somewhere, they chase it. And valuations start exploding from there as there becomes insatiable demand for these new ‘could be’ unicorns (i.e. billion dollar startups).

Who would throw money at a startup business that was intended to take down the deeply entrenched, highly regulated and defended taxi business? You only invest when you know you have an administration behind it. That’s the only way you put cars on the street in NYC to compete with the cab mafia and expect to win when the fight breaks out. And they did. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation. Uber is valued at $60 billion. That’s more thanthree times the size of Avis, Hertz and Enterprise combined.

Will money keep chasing these companies without the wind any longer at their backs?”

Now, this was back in March. And that was the question — will it keep going under Trump? Can they continue to thrive/ if not survive without policy favors. Most importantly for the billion dollar startup world, will the private equity capital dry up. This is what it’s really all about. Will the money that chased the subsidies from D.C. to Silicon Valley for eight years (i.e. the trillion dollar pension funds) stop flowing? And will it begin chasing the new favored industries and policies under the Trump administration?

It seems to be the latter. And it seems to be happening in the form of a return to the public markets — specifically, the stock market.

And it may be amplified because of the huge disparity in what is being favored. In Silicon Valley, innovation is favored. Profitability? Remember, the 90s tech bubble. The measure of success for those companies was “eyeballs.” How much traffic were they getting to their websites? Today, when you hear a startup founder talk about the success benchmarks, it rarely has anything to do with with revenue or profit. It’s all about headcount (how many people they’ve hired) and money raised (which enables them to hire people). They are validated by convincing investors to fund them (mostly with our pension money).

Now, the other side of this coin: Trumponomics. Remember, among the Trump policies (corporate tax cuts, repatriation, deregulation, infrastructure spend), the most common sense play in the stock market has been flooding money into companies that make a lot of money. Those that make a lot of money have the most to gain from a slash in the corporate tax rate — it falls right to the bottom line. Leading the way on that front, is Apple. They make a lot of money. And they will make a lot more when a tax cut comes, making the stock even cheaper. That’s why it’s up 25% year-to-date. That’s 2.5 times the performance of the broader market.

Meanwhile, let’s take a look back at the Snapchat. Snapchat doesn’t make money. And even after a 1/3 haircut on the valuation, trades about 35 times revenue. And now, as a public company, probably doesn’t get the protection from the venture capital/private equity community that may have significant investments in its competitors. So the competitors (like Facebook) are circling like sharks to copy their business.

What about Uber? The Uber armor may be beginning to crack as well, with the leadership shakeup in recent weeks. Maybe a good signal for how Uber may be doing? Hertz! Hertz has bounced about 20% from the bottom this week.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

For perspective: As of the close yesterday, the Nasdaq was up 18% year to date (just five months in). Gold was in the middle of a three year range. Market interest rates (the U.S. 10-year government bond yield) was just above the middle of the range of the past four years. The dollar was not far off its strongest levels in 15 years.

Today the media has explicitly printed the headline of impeachment for Trump (actually, they’ve run those headlines a various times over the past several months). Nonetheless, stocks (the S&P 500) today are off by 1.6%.

This gets the bears very excited. I saw the story about consumer debt, surpassing 2008 levels, floating all over the internet today. People tried to make the bubble connection — implying another debt crisis was coming.

The real story: Total household indebtedness finally surpassed the previous peak from 2008. That’s precisely what the Fed was attempting to do with zero interest rates. Make existing debt cheaper to manage, and at some point, break the psychology of the debt burden and get people borrowing (at ultra-cheap rates), investing and spending again. Otherwise, our economy and the world economy would have gone into a deflationary spiral.

That said, as I’ve found in my 20 years in this business, people tend to find a story to fit the price. The story hadn’t been fitting the price for much of the past six months. Today, it seems pretty easy. See the chart below of stocks ….

We had the first breakdown of the Trump trend in March, but all it could muster was about a 3% correction. This looks much more like a technical correction (a double top, and trend break today) – than a Trump impeachment trade. I suspect with the earnings catalyst behind us, this is the start of a deeper technical correction, which is healthy in a bull market. And it may take significant progress made in tax reform to see new highs in the broad stock indicies. We shall see.This next chart is the dollar index. This too had a significant trend break today. This translates into a higher euro, which would spell out a story where Europe is improving and the ECB is able in start discussing exit from QE.

What about the Trump/Comey saga? Aren’t people dumping dollars because of that? Not likely. If that were potentially destabilizing to the U.S., it would be destabilizing to the global economy, and people would buy dollars not sell them.

With that in mind, here’s gold. Gold sits on the brink of a big trend break (higher). When looking at gold and the dollar, it’s important to remember this: back in the heat of the crisis, gold and the dollar moved together, higher! That’s opposite of the traditional correlation. They moved higher together because people bought gold and they bought dollars (and dollar denominated assets, like Treasuries) as they viewed it the safest alternative in the world to park money – with the chance of getting it back.

With a break higher in gold looking imminent, and the dollar looking lower, it looks like a more traditional relationship. It’s not communicating crisis.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

We had new record highs again in the Dow today. But remember, yesterday we talked about this dynamic where stocks, commodities and the dollar were strong. But a missing piece in the growing optimism about growth has been yields.

Clearly the 10 year at 2.40ish is far different than the pre-election levels of 1.75%-1.80%. But the extension was quick and has since been a non-participant in the full-on optimism vote given across other key markets.

Why? While stocks can get ahead of better growth, yields can’t in this environment. Higher stocks can actually feed higher growth. Higher yields, on the other hand, can kill it.

But there’s something else at work here. As we know Japan’s policy to target the their 10 year at zero provides an anchor to our interest rates, as the BOJ is in unlimited QE mode. Some of that freshly produced liquidity, and the money displaced by their bond buying, undoubtedly finds a happier home in U.S. Treasuries (with a rising dollar, and a 2.4% yield). That caps yields.

But in large part, the quiet drag on U.S. yields has also come from the rising risks in Europe. The election cycle in Europe continues to threaten a populist Trump-like movement, which is very negative for the European Union and for the survival of the single currency (the euro). That creates capital flight, which has been contributing to dollar strength and flows into the parking place of U.S. Treasuries (which pressures yields, which is keeping mortgage and other consumer rates in check).

These flows are also showing up clearly in the safest bond market in Europe: the German bunds. The 2-year German bund hit an all-time record LOW, today of -91 basis points. Yes, while the U.S. mindset is adjusting for the idea of a 3%-4% growth era, German yields are reflecting crisis and money is plowing into the safest parking place in Europe. The spread between German and French bonds are reflecting the mid-2012 levels when Italy and Spain where on the brink of insolvency — only to be saved by a bold threat/backstop from the European Central Bank.

We talked last week about the prospects for higher gold and lower yields as questions arise about the execution of (or speed of execution) Trump’s growth policies, some of the inflation optimism that has been priced in, may begin to soften. That would also lead to a breather for the stock market. I suspect we will begin to see the coming elections in Europe also contribute to some de-risking for the next couple of months. We already have a good earnings season and some solid economic data and optimism about the policy path priced in. May be time for a dip. But as I’ve said, it would create opportunities– to buy any dip in stocks, and sell any rally in bonds.

To peek inside the portfolio of Trump’s key advisor, join me in our Billionaire’s Portfolio. When you do, I’ll send you my special report with all of the details on Icahn, and where he’s investing his multibillion-dollar fortune to take advantage of Trump policies. Click here to join now.

I talked yesterday about the Fed. As I said, I think we’ll find that the Fed will shift gears again to stay behind the curve on inflation, to let the economy run a little hot. They met today and it was a non-event. They said nothing to build momentum on their rate hike from December.

The news of the day has been Apple (NASDAQ:AAPL) earnings. People over the past couple of years have been calling for the decline in Apple. They’ve said it’s topped. They can’t innovate in the post-Steve Jobs era. The iPhone was magic. But reproducing magic isn’t easy. Once you put a computer in everyone’s pocket, there’s not much more they can do to it with it. These are all of the quips about Apple’s peak. They may be right. But Apple’s peak, at least as a stock, is greatly exaggerated.

They reported a huge positive surprise on earnings yesterday after the close. The stock was up 6% on the day. But even before that, I suspect it has become a much loved stock in the past two months in the “smart money” investor community.

We should see in the coming weeks, as big investors disclose their positioning for the end of Q4, Apple will have returned to a lot of portfolios again. Warren Buffett, an investor that has made his fortune buying when others are selling, built a big stake at the lows of the year last year. And it’s a perfect Buffett stock.

It’s incredibly cheap compared to the market.

The stock still trades at 15x earnings. Much cheaper than the market. Apple trades at 13x next year’s projected earnings. The S&P 500 trades at 16.5x. What about Apple’s monster cash position? Apple has even more cash now — a record $246 billion. If we excluded the cash from the valuation, Apple market cap goes down from $675 billion to $429 billion. That would equate to Apple trading at closer to 9x earnings. Though not an “apples to apples” that valuation would group Apple with the likes of these S&P 500 components that trade around 9 times earnings, like: Dow Chemical, Prudential Financial, Bed Bath & Beyond, a Norwegian chemical company (LBY), and Hewlett Packard Enterprise. It’s safe to say no one is debating whether or not Hewlett Packard is at the pinnacle of its business. Yet, if we strip out the cash in Apple, AAPL shares are trading closer to an HPE valuation.

Add to that, Apple now has a fresh catalyst coming in, Trump policies. The new President Trump is incentivizing Apple (and others) to bring offshore cash hoards back home with a flat 10% tax. And Apple makes money – a lot of it. A cut in the corporate tax rate will be a boon for earnings. Two years ago, Carl Icahn argued that Apple should use (a lot more of) their cash to buyback shares – and, with that, valued the stock at double its current levels.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Remember, it wasn’t too long ago that the world was sitting on every word uttered by a central banker. Those days are likely over — at least to the extreme extent of the past decade. For now, Trump has supplanted central bankers as the most powerful policy maker in the world.

Still, the Fed will meet following their rate hike last month, the second in their very slow hiking cycle – 1/4 point hike twelve months apart. They’ll do nothing this week, but the data tends to be going as desired by the Fed, and other major central banks for that matter (aside from Japan) — meaning, inflation has recovered and is nearing the target zone.

Remember, this time last year, the world was staring down the barrel of DE-flation again. Inflation, central bankers have tools to combat. Deflation is far more difficult, and far less predictable. It can spiral and grind economies to a halt. When consumers are convinced prices will be cheaper in the future, they wait. When they wait, economic activity stalls. With that, deflation tends to create more deflation. The fear of that scenario, and the potential of an irreversible spiral, is why central bankers were cutting rates to negative territory last year.

Where was the imminent deflationary threat coming from? Slow economic activity, but mostly a crash in oil prices.

Central bankers have the tendency to change the rules of the game when it suits them. When inflation is running hot, they may hold off on tightening money by pointing to hot “food and energy” prices. These are temporary influences, as they say. Interestingly, they are much more aggressive, though, when oil prices are creating a deflationary threat – as they did last year.

With that, oil prices have doubled from the lows of last February. So it shouldn’t be too surprising that inflation numbers are rising, and getting close to the desired targets (around 2%) of the central bankers of the U.S., Europe and England.

So will we see a turning point for global central banks (not just the Fed) in the months ahead? The world has already been pricing in the likelihood that the pro-growth policies coming from the Trump administration will take the burden of manufacturing economic recovery off of the central banks.

But we may find that “transitory oil prices” will be the excuse for more inaction by the Fed, and continued QE from the ECB and BOE in the months ahead, which may result in a slower pace of rate hikes than both the Fed projected in December and the market has been anticipating.

Higher rates at this stage: 1) creates problems for the housing recovery, 2) promotes more capital flight from emerging markets like China (which means more dollar strength),and 3) threatens to neutralize the fiscal stimulus and reform coming down the pike for the U.S.

In December, the Fed dialed back their talk about letting the economy run hot (i.e. staying well behind the curve on inflation to make sure recovery is robust). We’ll see if they switch gears again and start explaining away the inflation numbers to oil prices.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

For two full months the Trump rally has consisted of higher stocks, higher yields, a higher dollar and higher commodity prices — all on the prospects of hotter growth and a sustainable period of prosperity ahead.

Since the night of November 8th, it’s been “buy it now, prove it to me later” market. But people are expecting there will be a period of time where the markets begin trading in “prove it to me” mode.

Often we see a “buy the rumor, sell the fact” phenomenon in markets — it’s a reflection of investors pricing new information in anticipation of an event, and then selling into the event on the notion that the market has already valued the new information. With that, the period surrounding the January 20th inauguration could be the “sell the rumor” moment (in fact, we may be working on it now).

Many are hoping it could be the second chance given to those that have been left behind in the great Trump reflation rally. The question is, how deep or shallow that correction might be, and how long or short-lived it might me.

I would argue, it’s going to short-lived and shallow (maybe very shallow), for all of the reasons I’ve discussed in this daily note, not the least of which, is a world starving for a return to meaningful and sustainable growth, and the perception that this is the best chance we’ve had and might have, to get the global economy back on track. Trump’s tone today, in his press conference, indeed, indicated that he would waste no time executing on his plan. That favors a short-and-shallow correction scenario for the Trump rally. And shallow corrections are typical of strong trending markets.

With that said, since the election, here’s a view of key markets (taking the last price before the election night whipsaw):

The yield on the 10-year has gone from 1.85% to over 2.64% on the Trump effect. But despite a surprisingly hawkish Fed on December 14th, and even more hawkish fundamental data since, the high in yields, thus far, was marked the day after the Fed meeting last month. And today yields traded just below 2.33%, the lowest since November 30th! For technicians, the 38.2% (Fibonacci) retracement of the entire move is 2.34%. That would be considered a shallow retracement.

The dollar (index) has gone from 97.68 to 103.82, and today trades at 101.28 which is the lowest level since December 14. Commodities (the broad commodity index) have gone from 183 to 193, and today trades at 191. Both have room for another 1% or so lower. The dollar looks very strong.

What about stocks? The S&P 500 has gone from 2,138 to 2,278, and now trades at 2,262. A shallow retracement for stocks of the Trump rally would be about 2,225 (which is about 2% lower from here). Given the policy outlook, those wishing for something deeper may not get the chance – a couple of percentage points from here may be the gift.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

This morning we got a report that small business optimism hit the highest level since 2004, on the biggest jump since 1980. This follows a big jump in December, which obviously follows the November elections.

Small business owners that have survived the storm over the past nine years, most likely have had credit lines pulled, demand for their products and services crushed, and have slashed their workforce. If they were able to piece it together to continue on, they’ve operated as lean as possible, and they’ve slowly seen it all recover. And finally, over the past couple of years, they’ve likely had banks calling offering them money again. But, given the scars of the financial crisis, taking on debt again (or more debt) in an uncertain world, many have turned it down.

But if you’re going to dip a toe in the water again, take on some risk to grow your business (to expand, to hire, to build inventories), small business owners are saying now is the time. They are buying into what the Trump agenda is promising–a “dynamic booming economy.”

You can see that reflected in this chart…

The survey shows that 50% of small business owners expect the economy to improve. That’s the most in 15 years. With that, they think it’s a good time to expand. And they expect higher sales coming down the pike, so they’ve been building inventories.

As we know, in the recovery that was manufactured by the Fed (and other central banks), Main Street didn’t participate–trillions of dollars spent and little impact on the real economy. But this survey shows that the Trump effect is already doing what nine years, and trillions of dollars of monetary stimulus and intervention, couldn’t do. Most of the small business sentiment data has now returned to pre-crisis levels, just on the pent up demand that has been unleashed by the prospects of a return to prosperity.

This number tends to correlate highly with consumer confidence numbers. Consumer confidence numbers drive consumption. And consumption contributes about two-thirds of GDP. By restoring confidence, the Trump effect on growth can be self-fulfilling.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

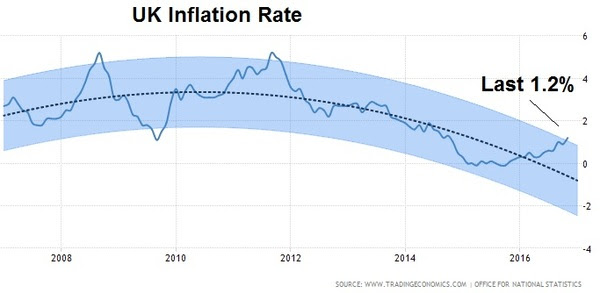

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

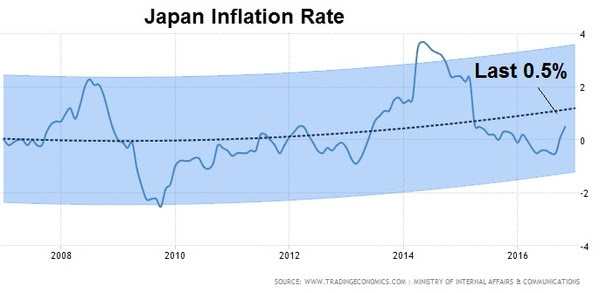

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We talked yesterday about the bad start for global markets in 2016. It was led by China. Today, it was a move in the Chinese currency that slowed the momentum in markets. Yields have fallen back. The dollar slid. And stocks took a breather.

China’s currency is a big deal to everyone. It’s the centerpiece of the tariff threats that have been levied from the U.S. President-elect. I’ve talked quite a bit about that posturing (you can see it again here: Why Trump’s Tough Talk On China May Work).

As we know, China, itself, sets the value of its currency every day. It’s called a managed float. They determine the value. And for the past two years, they’ve been walking it lower — weakening the yuan against the dollar. That’s an about face to the trend of the prior nine years. In 2005, in agreement with their major trading partners (primarily the U.S.), they began slowly appreciating their currency, in an effort to allay trade tensions, and threats of trade sanctions (tariffs).

So what happened today? The Chinese revalued its currency — pegged ithigher by a little more than a percent against the dollar. That doesn’t sound like a lot, but as you can see in the chart, it’s a big move, relative to the average daily volatility. That became big news and stoked a little bit of concern in markets, mostly because China was the sore spot at the open of last year, and the PBOC made a similar move around this time, when global marketswere spiraling.

Why did they do it? This time around, the Chinese have complained about the threat of capital flowing out of the country – it’s a huge threat to their economy in its current form. That’s where they’ve laid the blame, on the two year slide in the value of the yuan. With that, they’ve allegedly been fighting to keep the yuan stable and have been stepping up restrictions on money leaving the country. Today’s move, which included a spike in the overnight yuan borrowing rate, was a way to crush speculators that have been betting against the currency, putting further downward pressure on the currency. But it also likely Trump related – the beginning of a crawl higher in the currency as we head toward the inauguration of the new President Trump. It’s very typical for those under the gun for currency manipulation to make concessions before they meet with trade partners.

So, should we be concerned about the move today in China? No. It’s not another January 2016 moment. But the move did drive profit taking in twobig trends of the past two months: the dollar and U.S. Treasuries. With that, the first jobs report of the year comes tomorrow. It should provide more evidence that the Fed will hike a few times this year. And that should restore the climb in the dollar and in rates.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.