Yesterday we talked about the commodities bull market and the move underway in natural gas.

That all continued today, thanks in part to a comment by the U.S. Treasury Secretary, saying “obviously a weaker dollar is good for us.” When the dollar goes down, commodities prices tend to go up, since they are largely priced in dollars. As such, commodities were the top performers of the day – beginning to gain more momentum at multi-year highs.

But as we’ve seen from this chart, this recovery in commodities, which has dramatically lagged in the reflation trade, has a long way to go.

While the markets reacted as if Mnuchin, the Treasury Secretary, was talking down the dollar, the dollar is already in a long-term bear market cycle.

Remember, we looked at this chart (below) of the long-term dollar cycles back in June…

And I said, “if we mark the top of the most recent cycle in early January, this bull cycle has matched the longest cycle in duration (at 8.8 years) and comes in just shy of the long-term average performance of the five complete cycles. The most recent bull cycle added 47%. The average change over a long-term cycle has been 56%. This all argues that the dollar bull cycle is over. And a weaker dollar is ahead. That should go over very well with the Trump administration.”

The dollar is down about 8% since then and is breaking down technically now.

The dollar index is now down 14% in this new bear cycle. And these are the early innings. Based on the dollar cycle, it has a long way to go, and should last for another 5 to 7 years.

So, this dollar outlook is further support for the case for a big run in commodities we’ve been discussing. And as we observed yesterday, in the case of Chesapeake Energy (CHK), the second largest producer of natural gas in the country, the commodities stocks are still extremely underpriced if this scenario for commodities plays out.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

With a government shutdown over the weekend, today I want to revisit my note from last month (the last time we were facing a potential government shutdown) on the significance of the government debt load.

The debt load is an easy tool for politicians to use. And it’s never discussed in context. So the absolute number of $19 trillion is a guarantee to conjure up fear in people – fear that foreigners may dump our bonds, fear that we may have runaway inflation, fear that the economy is a house of cards. So that fear is used to gain negotiating leverage by whatever party is in a position of weakness. For the better part of the past decade, it was used by the Republican party to block policies. And now it’s being used by the Democratic party to try to block policies.

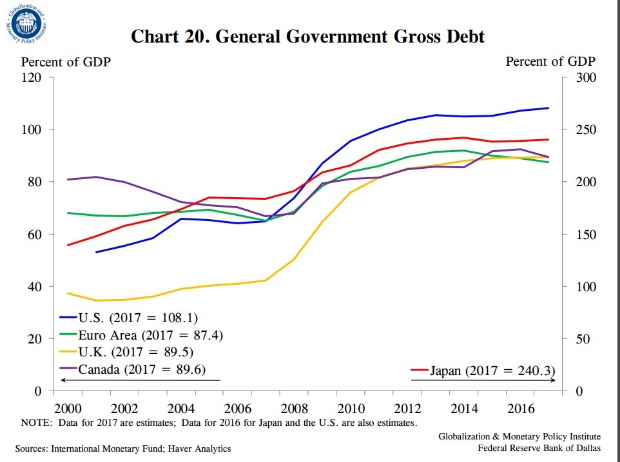

Now, the federal debt is a big number. But so is the size of our economy – both about $19 trillion. And while our debt/GDP has grown over the past decade, the increase in sovereign debtrelativetoGDP, has been a global phenomenon, following the financial crisis. Much of it has to do with the contraction in growth and the subsequent sluggish growth throughout the recovery (i.e. the GDP side of the ratio hasn’t been carrying its weight).

You can see in the chart below, the increasing debt situation isn’t specific to the U.S.

Now, we could choose to cut spending, suck it up, and pay down the debt. That’s called austerity. The choice of austerity in this environment, where the economy is fragile, and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession. Just ask Europe. After the depths of the financial crisis, they went the path of tax hikes and spending cuts, and by 2012 found themselves back in recession and a near deflationary spiral – they crushed the weak recovery that the European Central Banks (and global central banks) had spent, backstopped and/or guaranteed trillions of dollars to create.

The problem, in this post-financial crisis environment: if the major economies in the world sunk back into recession (especially the U.S.), it would certainly draw emerging markets (and the global economy, in general) back into recession. And following a long period of unprecedented emergency monetary policies, the global central banks would have limited-to-no ammunition to fight a deflationary spiral this time around.

Now, all of this is precisely why the outlook for the U.S. and global economy changed on election night in 2016. We now have an administration that is focused on growth, and an aligned Congress to overwhelm the political blocking. That means we truly have the opportunity to improve our relative debt-load through growth.

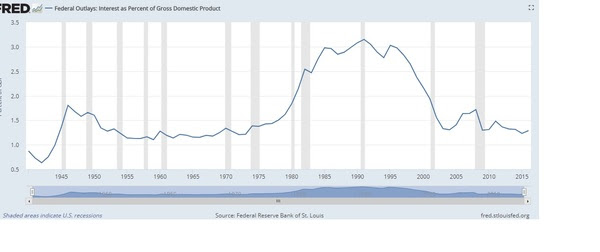

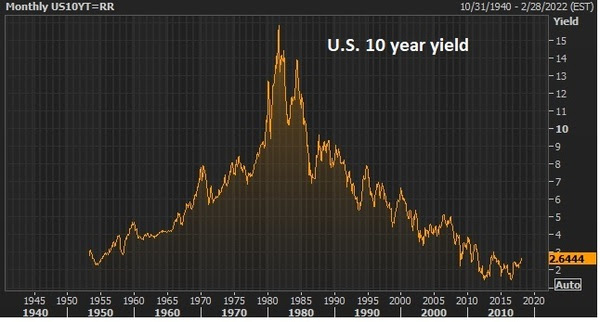

In the meantime, despite all of the talk, our ability to service the debt load is as strong as it’s been in forty years (as you can see in the chart below). And our ability to refinance debt is as strong as it’s been in sixty years.

For help building a high potential portfolio, follow me in our Forbes Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

government shutdown, washington, wall street, economy

Stocks reversed after a hot opening today. With a quiet data week ahead, the focus is on the prospects of a government shutdown.

If this sounds familiar to you, it should. Government debt is the, often played, go-to political football.

It was only last month that we were facing a similar threat. But with some policy-making tailwinds on one side of the aisle, the fight was politically less palatable in December. With that, Congress passed a temporary funding bill to kick the can to this month.

And just three months prior to that, in September, we had the same showdown, same result. The “government shutdown” card was being played aggressively until the hurricanes rolled through. From that point, politicians had major political risk in trying to fight hurricane aid. They kicked the can to December to approve that funding.

Now, the Democrats feel like they have some leverage, and their using the threat of a government shutdown to make gains on their policy agenda. So, how concerned should we be about a government shutdown (which could come on Friday)? Would it derail stocks?

If you recall, there was a lot of fuss and draconian warnings about an impending government shutdown back in 2013. The government was shutdown for 16 days. Stocks went up about 2%. Before that was 1995-1996 (stocks were flat), and 1990 (stocks were flat).

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

We kicked off the New Year continuing to discuss the theme of a hot stock market ahead (again) and a hotter than average economy (finally). Stocks continue to comply, with a big start – led by Japanese stocks today, up 2% on the day and up 4% on the year already.

It’s important to realize, the economic crisis was global. The central bank response was globally coordinated, led by the Fed. And, as we discussed early last year, everyone should hope Trumponomics works, because the global economy will benefit in coordination. And that’s what we’ve been seeing over the past year.

Of course, now we’re getting policy execution on that front, and we’re seeing the rising tide of the U.S. economy lifting all boats.

How high will that tide rise? As I said yesterday, if we add pro-growth policies that are being executed out of Washington, to an economy with near record low unemployment, cheap gas, near record low mortgage rates, record high consumer credit worthiness, record high household net worth, a record high stock market and near record low inflation, it’s hard to imagine the economy can’t do better than the long term average (3% growth) this year.

Let’s take a closer look at that economic growth picture.

Remember, in typical recessions, we should expect to get a big pop in growth to follow, due to policymaker responses to the slowdown and the natural upturn in the business cycle. In the Great Recession, we haven’t gotten it — after TEN years.

For the more than 50 years of history prior to the global financial crisis, U.S. economic growth averaged 3.5% (rolling four quarters). We’ve since averaged just 1.5% (over the past ten years). With that underperformance, the U.S. economy has foregone about $3 trillion dollars in real GDP growth, from being knocked off path by the global economic crisis. We’re due for a period to make up that ground.

On Tuesday we talked about the prospects of a return of “animal spirits” this year, for the first time in a long time. This is what can drive a period of economic growth that does better than the long term average. This animal spirits kicker may be the real theme of 2018.

But what is it?

Economics is about incentives. Economists think you’ll make rational decisions, with the incentive to best serve your interests. But emotions come into play. These emotions might cause you to be more risk-aversein times where policies incentivize you to take more risks, and vice versa.

This “emotion override” has been the problem over the past decade. The Fed gave us all abundant incentives to go out and borrow and spend, to stimulate the economy. But the scars of the housing crash, joblessness and overindebtedness were too great. People saved. They paid down debt. That didn’t trust the outlook. The Fed wanted us to take risk and they got risk aversion.

It has taken a regime change and an ultra-aggressive fiscal stimulus and structural reform response to finally break that mindset. The execution on tax cuts looks like the catalyst that has gotten more people off the fence, and believing in a rosier outlook. But I don’t think anyone would argue that confidence is broadly running hot (animal spirits) – much less, in a state of euphoria (which would justify concern of a top in markets and the recovery).

Robert Shiller (Yale economist) describes animal spirits like this: There are good times when people have substantial trust… They make decisions spontaneously. They believe instinctively that they will be successful.”

We’re not there yet, but we may begin seeing it/feeling it this year. And with that, we may see some hot growth over the coming years.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. And 25% of our portfolio is in commodities stocks. You can join me here and get positioned for a big 2018.

Global markets have started the year behaving very well, supporting my view that we’re in the early innings of an economic boom, and we should get another big year for global stock markets.

But, as we discussed heading into the end of 2017, that view isn’t shared by Wall Street or the Fed. For 2018, the Fed is looking for just 2.5% growth. And Wall Street is looking for just 6% growth in stocks (according to this WSJ piece). That’s less than the long term average return on the S&P 500.

Both continue to, somehow, ignore (or underestimate) the influence of fiscal stimulus, which is hitting into an already fundamentally improving economy.

Wall Street was looking for 3% growth in stocks last year. We got almost 20% (better in the Dow). And the Fed was looking for 2.1% growth last year. It will be closer to 3% for full year 2017.

They thought Trump couldn’t get policies legislated. Now we have big tax cuts, meaningful deregulation, the beginnings of a government spending program (started by natural disaster aid), and a massive incentive for companies to repatriate trillions of dollars.

If we add that to an economy with near record low unemployment, cheap gas, near record low mortgage rates, record high consumer credit worthiness, record high household net worth, a record high stock market and near record low inflation, it’s hard to imagine the economy can’t do better than the long term average (3% growth) this year.

As we’ve discussed, we’ve yet to experience the explosive bounce in economic growth that is typical of post-recession environments. This is set up to be that kind of year — maybe something north of 4%, which should finally move the needle on inflation. If that’s the case, despite the quadrupling of the stock market from the 2009 bottom, money may just be in the early stages of moving out of bonds and cash, and back into stocks.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. And 25% of our portfolio is in commodities stocks. You can join me here and get positioned for a big 2018.

We are off to what will be a very exciting year for markets and the economy.

Over the past two years I’ve written this daily piece, discussing the bigslow-moving themes that drive markets, the catalysts for change, and the probable outcomes. When we step back from all of the day to day noise that has distracted many throughout the time period, the big themes have been clear, and the case for higher stocks has been very clear. That continues to be the case as we head into the New Year.

As I’ve said, I think we’re in the early stages of an economic boom. And I suspect this year, we will feel it — Main Street will feel it, for the first time in a long time.

And I suspect we’ll see a return of “animal spirits.” This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mis-trust of the system. All along the way, throughout the recovery period, and throughout a quadrupling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset has been tough. But with the likelihood of material wage growth coming this year (through a hotter economy and tax cuts), we may finally get it. And that gives way to a return of animal spirits, which haven’t been calibrated in all of the economic and stock market forecasts.

With this in mind, we should expect hotter demand and some hotter inflation this year (to finally indicate that the global economy has a pulse, that demand is hot enough to create some price pressures). With that formula, it’s not surprising that commodities have been on the move, into the year-end and continuing today (as the New Year opens). Oil is above $60. The CRB (broad commodities index) is up 8% over the past two weeks – and a big technical breakout is nearing.

This is where the big opportunities lie in stocks for the New Year. Remember, despite a very hot performance by the stock market last year, the energy sector finished DOWN on the year (-6%). Commodity stocks remain deeply discounted, even before we add the influence of higher commodities prices and hotter global demand. With that, it’s not surprising that the best billionaire investors have been spending time building positions in those areas.

This year is set up to handsomely reward the best stock pickers.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. And 25% of our portfolio is in commodities stocks. You can join me here and get positioned for a big 2018.

Remember, this time last year, the biggest Wall Street investment banks told us stocks would do just 3% in 2017.

They were looking for about 2,300 on the S&P 500. The most aggressive forecast was 2,500 — coming from the Canadian bank, RBC (Royal Bank of Canada).

Here’s another look at the snapshot of those projections for 2017:

They undershot by a lot. The S&P finished just shy of 2,700 for the year. And S&P 500 earnings came in around $131. Wall Street was looking for $127.

But their big miss was underestimating the outlook for “multiple expansion.” The reason: They continue to underestimate the demand for stocks, in a world where ultra-low yields continue to incentivize people to reach for higher returns (i.e. opt for the choice of more risk for more return).

Investors will pay more for each dollar of future earnings if they expect to earn a higher future rate of return. And they have expected just that over the past few years, because 1) central banks promised to keep pumping up asset prices through QE and to continue warding off any shock risks that could derail the recovery for the economy and stocks, and 2) we’ve had the major shift away from austerity, which has promoted a weaker than typical recovery out of recession (and worse, stall speed growth) and toward big and bold fiscal stimulus (one that can potentially return the economy to a more normal, higher long term growth rate).

That’s why the P/E on stocks can and should rise well north of 20 times earnings in this environment, just as it has over the past three years.

The P/E on the S&P 500 was 20 in 2015, 22 in 2016 and 23 for 2017 (on trailing earnings). In each case, we came into the year, with the market undervaluing earnings — given what people have proven to be willing to pay up for them.

The market is now valuing the New Year’s earnings at 19 times earnings. And that ignores the probability that actual earnings can come in much better than estimates next year, given the corporate tax cut. That would ratchet down that “19 times” earnings valuation – making stocks cheaper.

For help building a high potential portfolio for 2018, follow me in TheBillionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up 45% over the past two years. Join me here!

Last year this time, as we ended 2016, and looked ahead to 2017, it was clear that the dominant theme for the year ahead would be Trumponomics.

We had a global economy that had been propped up by central banks for the better part of eight years, and growth that was proving to be dangerously slow — with growing risks of a stall and another downward spiral.

That was clear in the summer of 2016, when global interest rates started to diving deeply into negative territory. That meant people were happy to pay governments for the security of parking their money in government bonds.

There was a clear lack of optimism about economic conditions and what the future may look like.

That changed with Trump’s election and his commitment to launch an assault on economic stagnation.

It flipped the switch on the lack of optimism that had been paralyzing business activity. And that optimism has led to a hotter economy this year than most expected, despite the lack of substantial policy action (which we didn’t get until later in the year).

So what will next year look like?

As we discussed yesterday, we have tax cuts that should drive corporate earnings and warrant another double digit year for the stock market (close to 20%).

And that doesn’t take into account the impact to corporate earnings from personal tax cuts, a healthier job market with employees that can command higher wages and companies that are confident to take cash and invest in new projects. So, by design, we have incentives coming into the economy for 2018 that will boost demand. And another pillar of Trumponomics, infrastructure, will be the focus early next year, which will fuel more jobs, more economic activity.

All of this and the Fed is projecting just 2.5% growth next year. And Wall Street and the economist community tend to anchor their forecasts on the Fed. But the Fed doesn’t have a very good record in forecasting – especially in recent history.

They overestimated growth and the outlook throughout much of the recovery period. Instead we got stagnation.

But in the past 18 months or so, they flipped the script. They became the “new normal” believers that we’re in for long-term slower growth.

With that, they underestimated the outlook for 2017, even with the prospects of fiscal stimulus coming (they ignored it, and continue to). They were looking for 2.1% growth. It will be closer to 3% for the full year 2017. And next year, while they are looking for 2.5%, we could have something closer to 4%. That’s my bet.

Remember, we’ve talked about the fundamental backdrop, with the addition of fiscal stimulus, that could have us in the early stages of an economic boom period. I think we’ll feel that, for the first time in a long time, in 2018.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

While the President’s pro-growth plan had some wins this year, it was a slow start.

Going after healthcare first was a mistake. Fortunately, a pivot was made, and we now have a big tax bill delivered. And we have what will likely exceed a couple hundred billion dollars in government spending on hurricane/natural disaster aid underway (the early stages of a big government spending/ infrastructure package).

Last year this time, I predicted that Trump’s corporate tax cut would cause stocks to rise 39%. That’s a big number, that’s only been done a handful of times since the 1920s. We got a little better than half way there.

But, here’s the good news: We got there on earnings growth, ultra-low rates and an improving economy. All of that still stands for next year, PLUS we will have the addition of an aggressive tax cut that will be live day one of 2018.

With that, my analysis from last year still stands! Let’s walk through it (yet) again.

S&P 500 earnings grew by 10% this year. S&P 500 earnings are expected to grow at about the same rate next year. And that’s before the impact of a huge cut in the corporate tax rate. The corporate tax rate now goes from 35% to 21% – and for every percentage point cut in that rate, we should expect it to add at least a dollar to S&P 500 earnings.

With that, the forecast on S&P 500 earnings for next year is $144. If we add $14 to that (for 14 percentage points in the corporate tax rate) we get $158. That would value stocks on next year’s earnings, at today’s closing price on the S&P 500, at just 17 times earnings (just a touch higher than the long-term average). BUT, the Fed has told us that rates will continue to be ultra-low next year (relative to history). When we look back at ultra–low interest rate periods, the valuation on stocks runs higher than average—usually north of 20 times earnings.

If we take the corporate tax cut driven earnings of $158 and multiply it times 20, we get 3,160 on the S&P 500. That’s 18% higher than current levels. This analysis doesn’t incorporate the impact of a potentially hotter than expected economy next year (thanks to the many other areas of fiscal stimulus). So, as we’ve discussed throughout the year, the backdrop continues to get better and better for stocks.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Last week we had the merger of Fox and Disney, and the repeal of the Net Neutrality rule. And the tax bill continues to inch toward the finish line.

That said, this would typically be the time of year when markets go quiet as money managers close the books on the year, decision makers at companies go on holiday and politicians do the same.

But that wasn’t the case last year, as President-elect Trump was holding meetings in Trump towers and telegraphing policy changes. And it may not be the case this year, as the tax plan may be approved before year end. The final votes are said to come next week, and the bill is tracking to be on the President’s desk by Christmas.

With that, and with the lack of market liquidity into the year end, we may get a further melt-up in last trading days of the year.

Yesterday we talked about the other side of the Net Neutrality story that doesn’t get much acknowledgement in the press. In short, the tech giants that have emerged over the past decade, to dominate, have done so because of regulatory favor. This favor has decimated industries and has dangerously consolidated power into the hands of few. The repeal of this rule is turning that regulatory tide.

It looks like the playing field might be leveling. That means a higher cost of doing business may be coming for Silicon Valley, with fewer advantages and more competition from the old-economy brands that have been investing to compete online. That means potentially slower earnings growth for the big internet giants, for those that are making money, and an even more uncertain future for those that aren’t (e.g. Tesla).

With this in mind, at the moment Amazon is valued at twice the size of Walmart. Uber is valued at almost 40 times the size of Hertz. And Tesla, which has lost$2.5 billion over the past five years is valued the same as General Motors, which has made$43billion over the same period.

Next year could be the year these valuation anomalies correct.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.