We’ve talked the past couple of days about economic growth and the likelihood that we’re just beginning to see the positive surprises from Trumponomics materialize in the economic data.

The formula for GDP is consumption + investment + government spending + net exports. So you can see in these components, the direct targeting of economic stimulus in the Trump economic plan to drive growth: tax cuts, deregulation, repatriation, infrastructure and trade negotiations.

Now, consumption makes up about two-thirds of GDP. Let’s look at consumption today, and we’ll step through the other contributors to GDP over the next few days.

First, what is the key long-term driver of economic growth over time? Credit creation. When credit is used to buy productive resources, wealth goes up. And when wealth goes up consumption tends to go up. With that in mind, in the chart below you can see the sharp recovery in consumer credit (in orange) since the depths of the economic crisis (this excludes mortgages). And you can see how closely GDP (the purple line, economic output) tracks creditgrowth.

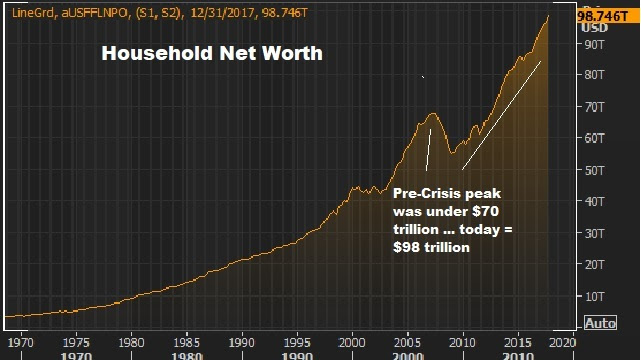

And we have well recovered and surpassed pre-crisis levels in householdnetworth — sitting at record highs now (up another $2 trillion since we last looked at it) …

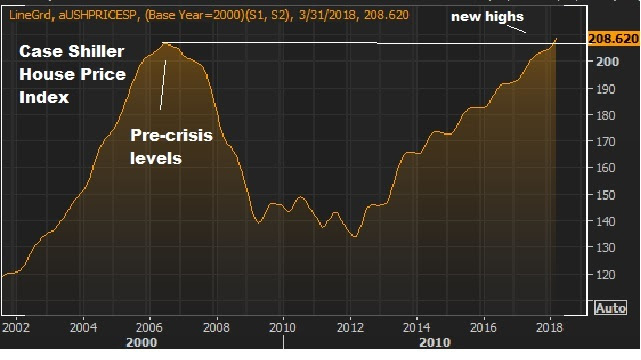

A large contributor to the state of consumption is the recovery and stability in housing. We are now back to new highs on the broad housing index …

When we consider this solid backdrop, remember, we’ve yet to have a return of ‘animal spirits’ — a level of trust and confidence in the economy that fuels more aggressive hiring, spending and investing.

And with that, as we discussed yesterday, while we are in the second longest post-War economic expansion, we’ve yet to have the aggressive bounce back in growth that is characteristic of post-recession recoveries.

But we now have the pieces in place to see the return of animal spirits and a big pop in economic growth. And that should continue to fuel for much higher stock prices. And there are stocks that will do multiples of what the broader stock market does.

There has been a lot of attention over the past couple of days on China and trade relations.

China has moved down tariffs on auto and auto parts imports. And a source today said the government has “encouraged” China’s largest oil refiner to buy more U.S. crude oil. Based on the reports, China is now taking about 8 times the daily volume of U.S. crude imports, compared to averages a few months ago.

These are concessions! This is a distinct power shift. Not long ago, the world was afraid to rattle the cage of China. They (global trading partners) tiptoed around touchy matters like Chinese currency manipulation prior to the global financial crisis a decade ago, and even more so after the crisis.

But now, you can see the leverage that has been created by Trump. This is exactly what we talked about the day after the election.

Here’s an excerpt from my November 9, 2016 ProPerspectives note, back when the experts were predicting Draconian outcomes for poking the China giant: “As we’ve seen with Grexit and Brexit, the votes came with dire warnings, but have resulted in creating leverage. Trump’s complaints about China are right. And a threat of slapping a tariff on Chinese goods creates leverage from which to negotiate.”

Now, we have an economy that is leading the global economic recovery. China wants and needs to be part of it. And we have a President that has a loud bark, and the credibility to bite. And that is creating movement. Let’s revisit, also from one of my 2016 notes, why this China negotiation is so important …

TUESDAY, SEPTEMBER 27, 2016

China’s biggest and most effective tool is and always has been its currency. China ascended to the second largest economy in the world over the past two decades by massively devaluing its currency, and then pegging it at ultra-cheap levels.

Take a look at this chart …

In this chart, the rising line represents a weaker Chinese yuan and a stronger U.S. dollar. You can see from the early 1980s to the mid-1990s, the value of the yuan declined dramatically, an 82% decline against the dollar. China trashed its currency for economic advantage—and it worked, big time. And it worked because the rest of the world stood by and let it happen.

For the next decade, the Chinese pegged its currency against the dollar at 8.29 yuan per dollar (a dollar buys 8.29 yuan).

With the massive devaluation of the 1980s into the early 1990s, and then the peg through 2005, the Chinese economy exploded in size. It enabled China to corner the world’s export market, and suck jobs and foreign currency out of the developed world. This is precisely what Donald Trumpis alluding to when he says ‘China is stealing from us.’

China’s economy went from $350 billion to $3.5 trillion through 2005, making it the third largest economy in the world.

This next chart is U.S. GDP during the same period. You can see the incredible ground gained by the Chinese on the U.S. through this period of mass currency manipulation.

And because they’ve undercut the world on price, they’ve become the world’s Wal-Mart (sellers to everyone) and have accumulated a mountain for foreign currency as a result. China is the holder of the largest foreign currency reserves in the world, at more than $3 trillion dollars (mostly U.S. dollars). What do they do with those dollars? They buy U.S. Treasurys, keeping rates low, so that U.S. consumers can borrow cheap and buy more of their goods—adding to their mountain of currency reserves, adding to their wealth and depleting the U.S. of wealth (and the cycle continues).

This is the recipe for big trade imbalances — lopsided economies too dependent upon either exports or imports. And it’s the recipe for more cycles of booms and busts … and with greater frequency.”

Again, China has to be dealt with. And we’re starting to see signs of progress on that front. Good news.

Over the past 24-hours, global markets were obsessed with the President’s move to renew sanctions on Iran. The oil market swung around. And so did stocks, to a degree.

These are important events. They are news-worthy events. And they carry plenty of shock-value. But, without underplaying the importance, we’ve seen this movie (bold change) a lot over the past 16 months, under the Trump presidency. And despite the risks that many have feared along the way, we’re seeing a better economy, healthier companies and healthier consumers. And we’re seeing the potential for reform in the trade imbalances that led to the financial crisis.

It’s the tough talk, tough positioning and the “credibility to act” that is producing results. And Trump is working from a position of strength, leveraging the biggest economy in the world, and an economy that is leading the global economic recovery. And he continues to tick the boxes on his game plan of change (global and domestic).

But the risks from the bold change has only provided more fodder for those skittish investors that don’t believe in the growth story. That continues to reinforce their views of an ugly outcome in global financial markets. And that continues to keep investors under-exposed to stocks.

However, with the fundamental backdrop strong, and valuations cheap (relative to low interest rate environments), that should keep the cash from the doubters chasing stock prices as they move higher.

At the end of last week, I said “it looks like the all-clear signal has been given to stocks.”

Well, we had some more discomfort to deal with this week, but that statement probably has more validity today than it did last Friday.

With that, let’s review the events and conditions of the past two weeks, that build the case for that all-clear signal.

As of last Friday, more than half of first quarter corporate earnings were in, with record level positive surprises in both earnings and revenues (that has continued). And we got our first look at first quarter GDP, which came in at 2.3%, better than expected, and putting the economy on a 2.875% pace over the past three quarters.

What about interest rates? After all, the hot wage growth number back in February kicked the stock market correction into gear. The move in the 10-year yield above 3% last week started validating the fears that rising interest rates could quicken and maybe choke off the recovery. But last week, we also heard from the ECB and BOJ, both of which committed to QE, which serves as an anchor on global rates (i.e. keeps our rates in check).

Fast forward a few days, and we’ve now heard from the last but most important tech giant: Apple. Like the other FAANG stocks, Apple also beat on earnings and on revenues.

Still, stocks have continued to trade counter to the fundamentals. And we’ve been waiting for the bounce and recovery to pick up the pace. What else can we check off the list on this correction timeline? How about another test of the 200-day moving average, just to shake out the weak hands? We got that yesterday.

Yesterday, in the true form of a market that is bottoming, we had a sharp slide in stocks, through the 200-day moving average, and then a very aggressive bounce to finish in positive territory, and on the highs of the day. That took us to this morning, where we had another jobs report. Perhaps this makes a nice bookend to the February jobs report. This time, no big surprises. The wage growth number was tame. And stocks continued to soar, following through on yesterday’s big reversal off the 200-day moving average.

With all of this, it looks like “the all-clear signal has been given to stocks.”

As we’ve discussed, the proxy on the “tech dominance” trade is Amazon. That’s the proxy on the stock market too. And it’s not going well. The President hammered Amazon again over the weekend, and again this morning.

Here’s what he said …

Remember, we had this beautiful heads-up on March 13, with the reversal signal in Amazon.

That signal we discussed in my March 13 note has now predicted this 15.8% decline in the fourth largest publicly traded company. And it’s dictating the continued correction in the broader market.

If you’re a loyal reader of this daily note, you’ll know we’ve been discussing this theme for the better part of the last year. The regulatory screws are tightening. And the tech giants, which have been priced as if they are, or would become, perfect monopolies, are now in the early stages of repricing for a world that might have more rules to follow, hurdles to overcome and a resurrection of the competition they’ve nearly destroyed.

As we know, Uber has run into bans in key markets. We’ve had the repeal of “net neutrality” which may ultimate lead big platforms like Google, Twitter, Facebook and Uber, to transparency of their practices and accountability for the actions of its users. Trump is going after Amazon, as a monopoly and harmful to the economy. Tesla, a money burning company, is being scrutinized for its inability to mass produce — to deliver on promises. For Tesla, if sentiment turns and people become unwilling to continue plowing money into a company that’s lost $6 billion over the past five years (while contributing to the $18 billion wealth of its CEO), it’s game over.

With that said, this all creates the prospects for a big bounce back in those industries that have been damaged by tech “disruption.” And this should make a stock market recovery much more broad-based than we’ve seen.

With the sharp decline in stocks today, we’ve retested and broken the 200-day moving average in the S&P 500. And we close, sitting on this huge trendline that describes the rise in stocks from the oil-crash induced lows of 2016.

Today we neared the lows of the sharp February decline. I suspect we’ll bottom out near here and begin the recovery. And that recovery should be fueled by very good Q1 earnings and a good growth number — brought to us by the big tax cuts.

We talked yesterday about the important inflation data. That was in line this morning. And with that, the big 3% level on the benchmark 10-year government bond yield remains well preserved.

But stocks soured anyway on the day, and it was led by the Nasdaq.

Let’s take a closer look at the Nasdaq.

This is where the big tech giants, Apple, Microsoft and Amazon have led the charge back in the index back to new record highs over the past couple of days. Those three stocks represent about a third of the index (and contribute heavily to the S&P 500 too).

But as the three tech giants led the way up, they cracked today, and we now have some very compelling signals that another down leg for stocks may be here.

First, as the broader financial markets are still licking the wounds of the sharp correction, and still jittery, Apple hit a record high valuation of $925 billion this week (sniffing near the trillion dollar valuation mark). And then it did this today…

As you can see in this chart above, Apple put in a huge bearish reversal signal (an outside day).

So did Microsoft (a huge bearish reversal signal).

So did Amazon, after breaching record levels of $1600 over the past two days …

And, not surprisingly, same is said for the Nasdaq – a big reversal signal…

The S&P 500 had the same reversal pattern.

For perspective, if we avoided the distraction of the big cap weighted indices, the Dow chart tells us the downtrend in stocks from the late January highs remains well intact.

As we discussed yesterday, stocks have fully recovered the decline that people were attributing to Trump’s trade barrier announcement last week.

With that, the tariff hysteria seems to have subsided a bit, as they struggle for evidence to support their hyperbole. Perhaps people may start acknowledging that we are now in a higher volatility environment, and that we will be slowly working out of this recent price correction until corporate earnings and economic growth data start confirming the benefits of tax cuts.

Interestingly, they seem to hate the trade threat, far more than the love the tax incentives and the pro-growth initiatives. And while trade is a complicated issue, everyone seems to suddenly have an expert opinion on it. And everyone is an expert on the Smoot-Hawley Act (which, by the way was a tariff on over 20,000 goods) and depression-era economics.

If they indeed were reflective about the economy, I think they would agree that we (and the world) desperately need growth initiatives to save us from terminal central bank life support (which wouldn’t be so terminal given they have fired all of their bullets to keep us afloat as long as they did). And they would know that we are in for a perpetual cycle of booms and busts (repeat of the credit bubble and burst) if the trade imbalances (mainly between China overproducing and the U.S. overconsuming) ultimately are not corrected.

Now, as more of the conversation on trade turns more toward China, I want to revisit an excerpt from my note in December of 2016 (when Trump was President-elect):

MONDAY, DECEMBER 19, 2016 — “While many think Trump will provoke a military conflict, that’s far from a certainty. With the credibility to act, however, Trump’s tough talk on China creates leverage. And from that leverage, there may be a path to a mutually beneficial agreement, where the U.S. can win in trade with China, and China can win. But it may get uglier before it gets better. In the end, growth solves a lot of problems. A hotter growing U.S. economy (driven by reform and fiscal stimulus), will ultimately drive much better growth in the global economy. And China has a lot to gain from both. Though in a fair-trade environment, they won’t get as much of the pie as they’ve gotten over the past two decades. But it has the chance of leading to a more balanced and sustainable economy in China, which would also be a win for everyone.”

Now, why not just focus on China now? Because they will continue to abuse other countries. And those open trade channels will still allow that product to enter the U.S. As we discussed yesterday, the global economy has been damaged by China’s currency/trade policy, yet the rest of the world has been relying on the U.S. to lead the fight. They need to join the fight to create the leverage to make it ultimately work – so that the global economy can find a sustainable path of recovery and robust growth.

Stocks continue to swing around, and in wider ranges than we’ve seen in a while. We should expect this type of action following a sharp technical correction–a correction that shook many of the players out of the market, that were contributors to suppressing volatility in recent years (the short vol ETFs among them).

Now, as I’ve said in the past, people always search for a story to fit the price. Despite the fact that stocks have been swinging around, with little or no story for them to attribute, they were quick to pounce on Trump’s announcement about steel tariffs, and have since blamed every down tick in the stock market for it. And they’ve run wild with trade war scenarios. For those trying to capitalize on that fear scenario, it shows how uninformed, naive or intellectually dishonest they are (most the latter). They like to evaluate it as if there is no context or history.

Where have they all been the past 20-plus years?

China has been manipulating the global markets through their cheap currency policy for the better part of the past 25 years. In pinning down their currency, they cornered the world’s export market. And in the process, they emerged as the second largest economy in the world. They also accumulated the world’s largest reserve of foreign currencies, which they plowed into global credit markets (mainly our Treasurys) to fuel cheap credit, which ultimately led to the global credit bubble and bust (the global financial crisis). We buy their cheap stuff. They take our dollars and buy Treasurys, supplying more credit to us to buy more of their cheap stuff. And so the cycle goes.

Currencies are the natural balancing mechanism to prevent this bubble/global imbalance from forming. When freely traded in an open economy, the market demand for yuan, given the aggressive growth in the economy, would have driven the value of China’s currency higher, making its exports less attractive, and therefore slowing their breakneck growth and wealth accumulation in China, and its ability to fuel global credit. But of course, the government determines the value of the yuan, and keeping the currency cheap is part of the economic model in China (still).

For those that fear retaliation (a historic response to protectionism), this is retaliation… for 20 years of wealth transfer.

The tariff threats address metals, but the currency is a key tool that makes it all happen. For those that like to play it as a political football, Trump is not the architect of the plan. A staunch democratic Senator from New York, Charles Schumer, led the push in Congress for a bill in 2005 to impose a 35% tariff on China. That’s what ultimately led to the agreement by the Chinese to allow their currency to weaken (somewhat). With that, I want to revisit my note from late September 2016 (prior to the elections) for a little more backstory on Why Trump Is Right About China (read more here).

If you are hunting for the right stocks to buy on this dip, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

As we discussed yesterday, the minutes from the most recent Fed meeting (which was still under Yellen) gave us some clues about the tone of a Powell-led Fed. They acknowledged the lift they expected from fiscal policy, which we didn’t hear all of last year, despite the clear telegraphing of it from the Trump administration. Powell was Trump appointed. And it looks like the Fed messaging will now reflect that.

This is from his prepared remarks today:

“The economic outlook remains strong. The robust job market should continue to support growth in household incomes and consumer spending, solid economic growth among our trading partners should lead to further gains in U.S. exports, and upbeat business sentiment and strong sales growth will likely continue to boost business investment. Moreover, fiscal policy is becoming more stimulative. In this environment, we anticipate that inflation on a 12-month basis will move up this year and stabilize around the FOMC’s 2 percent objective over the medium term. Wages should increase at a faster pace as well.”

So he’s bullish on economic output, wage growth and therefore, inflation. That’s bullish for rates. And, for the moment, what’s bullish for rates is bearish for stocks.

Oddly, on the same day Powell had his first testimony to Congress, the two former Fed chairs (Bernanke and Yellen) thought it was acceptable to host a chat about monetary policy this afternoon at the Brookings Institute.

It looked a bit like a partisan counter-punch. The same two former Fed Chairs that were, not long ago, begging Congress for fiscal stimulus to take some of the burden off of monetary policy, continue to (now) criticize the move. In fact, in Powell’s statement, he called the lack of fiscal response from Congress in past years, a headwind: “some of the headwinds the U.S. economy faced in previous years have turned into tailwinds: In particular, fiscal policy has become more stimulative.”

The takeaway from our first look at Powell: He doesn’t sound like a guy that will risk choking off the benefits of fiscal stimulus with overly aggressive “normalization” of monetary policy. That’s good.

If you are hunting for the right stocks to buy on this dip, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

With the big decline and wild swings in the stock market, earnings season has gotten little attention.

We’ve now heard from 80% of the companies in the S&P 500 on Q4. According to FactSet, 75% of the companies have beat on earnings. And 78% have had positive revenue surprises.

Now, earnings estimates are made to be broken. And they tend to be beaten at a rate of about 70% of the time. But the same cannot be said for revenues. This has been a key missing piece in the economic recovery. Companies have been cutting costs, refinancing and trimming headcount, all in an effort to manufacture margins and profitability. But revenues, the true gauge of business activity and demand, had been dead for the better part of the past decade.

It was just last year that we finally saw some decent revenue growth coming in from the earnings reports. And this most recent quarter, revenue growth is running at the hottest rate since FactSet has been keeping records. That’s a very good sign for the economic outlook.

And corporate earnings are running 15.2% higher than the same period the year prior. That’s the hottest earnings growth we’ve seen since 2011. More importantly, that’s four percentage points higher than analysts were projecting at the end of the year–with knowledge of the tax cut legislation.

With that said, remember, just last Friday, we had a moment during the day when the forward P/E on the S&P 500 hit 16.2. But if the fourth quarter is any indication, those forward earnings (estimates) will likely get ratcheted UP over the coming quarters, but will still undershoot. That will keep downward pressure on the P/E. Stocks are cheap.

If you are hunting for the right stocks to buy, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.