Last week, we talked a lot about oil, as OPEC was meeting to deliberate on the status of their agreement to cut production.

While oil prices have been rising aggressively over the past year, the markets haven’t been paying a lot of attention — distracted by Trump watching.

But then Trump put it on the front burner, with another jab at OPEC on Twitter. And the media and Wall Street began trying to deduce the OPEC outcome. In the end, they misinterpreted. OPEC’s agreement to go from overcutting to complyingwith the initial levels of production cuts, means they are still cutting.

So, the market is still undersupplied in a world where demand has proven to be underestimated. That’s a formula for higher prices.

That’s what we’ve had for the past year, and that’s what we’ve gotten since OPEC’s official statement on Friday. In my note last Friday, I said “the lack of enough action from OPEC may serve as a catalyst to push oil much higher from here. That, of course, serves OPEC’s interests.”

Oil prices have exploded! We’ve seen a $10 pop since Friday morning. That’s 15% in a week. And I suspect it’s going to keep going.

Remember, we’ve talked about the prospects for $100 oil this year. Leigh Goehring, one of the best research-driven commodities investors on the planet has been telling us that since last year. And he’s looking spot-on at the moment.

Bottom line: This script is precisely what we’ve been talking about, here in my daily ProPerspectives note, since the price of oil was in the $40s. We’ve talked about the prospects for a return to $80 oil, and maybe even as high as $100 oil. And it looks more and more possible, given the surging demand and the supply shortfall.

How can you play it. On this thesis for oil, in my Billionaire’s Portfolio, we added SPDR Oil and Gas ETF (symbol XOP) and Phillips 66 (symbol PSX) back when oil prices were deeply depressed (in 2016). We followed the activism of policymakers (both central banks and OPEC). And in the case of PSX, we also followed Warren Buffett.

Both are up big, but have a lot more room to run. Oil and gas stocks (which comprise the XOP) have yet to reflect the supply shortfall in the oil market, much less the booming demand that is coming from an improving global economy (which many have underestimated).

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We’ve talked about the case for a shakeout in Amazon. It was up big today on news that it would be buying a big online pharmacy.

That worked to curtail the slide in the stock (for now). But it only exacerbates the building regulatory scrutiny and the President’s wrath against Amazon’s developing monopoly and power (much of which has been garnered overtime from the unfair advantages Amazon has enjoyed from operating as an internet company).

If there’s one thing we know about Trump as a President, he’s done what he says he’s going to do. And he’s had plenty of verbal threats directed squarely at Amazon. We can only assume that he will carry out the offensive he’s been promising — against a company that has crushed industries by price wars.

On a similar note, let’s talk about China. As we’ve discussed quite a bit, China’s rapid economic ascent in the world came through currency manipulation. They held their currency down, to underprice the world on exports. And as the world stood by and watched (and bought lots of stuff from them), they became the world’s second largest economy, and the accumulated the largest war chest of foreign currency reserves.

China is to the world, as Amazon is to corporate America. And Trump is attempting to deal with them both head on.

Interestingly, China is quietly fighting back, via the currency. The go to tool in China is currency devaluation.

That’s what they’ve been doing over the past three months. And that has accelerated in just the past 10 days – they’ve devalued by almost 4% against the dollar. This is something to watch closely. A big one-off devaluation out of China would be a geopolitical cage rattling.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

While the media continues to be stuck on the global jawboning about trade. We’ve been talking about the continued domestic “leveling of the playing field.”

We’ve seen the verbal and Twitter shots taken by Trump at the tech giants since he’s been in office. And the threats have slowly been materializing as policy.

Late last year, we talked about the repeal of the Net Neutrality rule. And now we have the Supreme Court ruling that subjects internet sales to state tax.

Before you know it, the tech giants (Facebook, Amazon, Netflix, Google …) may actually be held to a similar standard that their “old economy” competitors are held to. They may have to pay for real estate (i.e. bandwidth). They may be liable for content on their site, regardless of who created it. And they may be scrutinized more heavily for anti-competitive practices.

That means, the costs may go UP for these companies. And the cost may go UP for consumers. But a more balanced and stable economy and society may come with it.

So, the balance of power is shifting, just as people were becoming convinced that Amazon was taking over the world. As we’ve discussed, if the market starts pricing OUT the prospects of Amazon becoming a monopoly, then the jaws may be closing on this chart …

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We’ve talked about the big OPEC decision this week, and the prospects for oil prices.

When we get a market that thinks they know the outcome, we get a market that begins leaning too hard in one direction. And that creates an market outcome that can be asymmetric (i.e. lopsided). That’s what we had today.

In this case, Trump’s verbal attacks on OPEC’s price manipulation generated a media frenzy surrounding the OPEC meeting. And with the media swarming, the oil ministers seemed happy to oblige with commentary and pontification. And that set expectations for the outcome.

And this morning, OPEC released their communique, but it was far from the clean production increase the market was looking for. With that, we got this chart …

It went straight up. Oil was up almost 6% on the day and nearing $70 again. And this lack of enough action (as we should expect) from OPEC, to balance the oil market, may serve as a catalyst to push oil much higher from here (which serves OPEC’s interests).

And as we discussed yesterday, with high oil prices now squarely on the radar (for Trump, the media and the market), we may begin seeing oil prices weigh on stock prices.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We talked yesterday about the big influence of oil. And how the swings of the past few years have directly impacted the global economy.

Too low was threatening another global financial crisis. Now, too high is threatening to choke off the strength of the economic recovery.

Both high and low prices have been manipulated by OPEC. And we now await a decision from OPEC nations on whether or not a they will hike production to curb the level of oil prices. For a group that operates for their best interest, it doesn’t seem to be in their best interest. That decision will be announced tomorrow at a press conference.

Given the attention the Trump has given to OPEC and oil prices recently, a negative surprise (i.e. no production hike) may trigger the oil price/stock market inverse correlation trade (oil goes up, stocks go down).

On that note, we have some negative momentum going into tomorrow. Before today’s close, the Nasdaq was up 14% year-to-date. Meanwhile, the S&P 500 is up just around 3%. That’s a lopsided market.

But today we get a big outside day (key reversal signal) in the Nasdaq futures.

And the catalyst for this technical reversal setup was the Supreme Court ruling today that internet sales should be subject to state tax.

We’ve talked about the building scrutiny from the Trump administration facing the tech giants. This is another “level the playing field” step. If Amazon is pricing in the prospects of taking over everything (i.e. monopoly), this is the shot across the bow.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We’ve talked about the case for much higher oil prices since I started writing this daily note back in January of 2016. And we’ve since had a triple off of the February 2016 bottom.

The crash in oil prices from 2014 to 2016 was induced by OPEC as an effort to crush the competitive U.S. shale industry. While they nearly succeeded, these oil producing countries nearly killed their own economies in the process. So, in effort to drive oil prices higher, to salvage oil revenues, they had to flip the switch in late 2016, cutting production for the first time since 2008. And they did so, in a market that was already undersupplied. And in a world where demand has been underestimated, and growing.

So now, we’ve had this big recovery – nearly a round trip back to those 2014 levels.

The problem? The oil price crash was a threat to the global economy, as bankruptcies were lining up and deflationary forces were returning in the global economy. But now, current oil prices (and higher) are threatening to the recovery too, specifically the economic gains from fiscal stimulus.

And that’s on the wrong side of Trump. So, we’re seeing pressure on OPEC from the White House.

Will OPEC comply?

They are meeting now to determine whether or not they stick with current policy, or make an increase to production.

The expectations have been set for an increase. But there is dissension in the ranks at OPEC. If they surprise markets and maintain current output (i.e. no increase), we could see oil move much higher, and quickly. That would throw a wrench in almost everything. Remember, Trump’s tough positioning has a lot to do with the leverage he gets from a strong economy. $100 oil would threaten the economic outlook, and change the face of trade negotiations and the geopolitical environment.

We will likely hear leaks on Friday and probably hear a decision from OPEC on Saturday.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

The big approval on the AT&T takeover of Time Warner has opened the door to big industry consolidation coming down the pike.

When Trump won the election in November of 2016, by December, the billionaire Japanese business man Masayoshi Son was meeting with the President-elect in Trump Towers. Son owns more than 80% of Sprint and was wanting to merge with TMobile to challenge the duopoly in the wireless carrier industry (AT&T and Verizon). The prospects of this deal (a merger) were killed by the Obama administration, as antitrust enforcers warned it would put the dominance of the wireless industry in too few hands (from four to three) – making it less competitive. That deal had new prospects with Trump. So Son got on a plane.

He clearly knew the Trump administration was going to be very pro-business. And the likelihood of getting a deal blessed under Trump’s watch (relative the outgoing administration) improved dramatically on election day.Indeed, deal making is hot under Trump. Last year, there were over 18,000 merger and acquisition transaction in North America — the highest on record. This year, a little less than half way through the year, and we’ve had a little less than half the volume of last year. And Son’s deal with TMobile is now in the queue for FCC approval.

And of course, we now have the 21st Century Fox bidding war. The company had already agreed to sell (most of) itself to Disney. But when the AT&T deal was approved, Comcast stepped in an upped the ante. All of these deals have everything to do with keeping their footing in the “Information Revolution.” If not, they get made irrelevant by the tech giants. They are fighting to maintain their moat on internet infrastructure, but they are also fighting to keep their dominant position in content, while going head-to-head with the new players, in taking that content direct-to-consumers.

Meanwhile, the market seems to be pricing in future dominance and monopolies in the FAANG stocks. These deals are making that less likely.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Last week we stepped through all of the components of economic output and talked about the setup for positive surprises. Keep in mind, the economy is running at near a 3% pace already. And if Trumponomics is just in the early stages of materializing in the data on consumption, investment, government spending and exports, then we may be in for a big growth number.

On Friday we talked about the exports (i.e. the trade) component. On that note, the media was stirring over the combative tone from G7 events over the weekend. What I heard was the potential for big movement (i.e. gains on U.S. exports, which will drive gains in GDP). Trump went in and proposed taking down all trade barriers. That’s negotiating from an extreme. And that typically brings about movement. Quickly, trade partners were discussing “reducing” barriers.

With hotter than expected growth coming, how will that effect Fed policy?

We will soon see. The Fed meets this week. They continue their path of normalizing rates. They’ve hiked once in 2015, once in 2016, three times in 2017 and once, thus far, this year. The market is nearly fully pricing in a second hike for the year on Wednesday. And expectations are for another hike in September. We’ll see this week if they’re adjusting uptheir growth forecasts.

As for the rate path: Remember, Powell is a Trump appointee, and from what we’ve heard from him thus far, he sounds like someone that’s not going to risk chipping away at the recovery by jumping ahead with overly aggressive rate hikes. Unlike the last regime, he will likely take a “whites of inflation’s eyes” approach.

We’ve talked about the set up for positive surprises in the data. We’ve looked at the first two components of GDP (consumption and investment) both of which are set up for positive surprises. Today let’s look at government spending.

It’s typical for debt to balloon in economic downturns. Not only did our debt/gdp ratio balloon in the U.S. but it ballooned everywhere. With that, as the global economy was being propped up by central banks, for the better part of the past decade, the politicians were reluctant to help on the fiscal side. Instead, they went the other way. They went the path of austerity. They focused on debt when the economy desperately needed growth.

Fiscal tightening in a widespread global recession is a recipe for tipping it all into depression. That required the central banks to do more, and more, and more to keep the economy from entering into a deflation spiral — fighting the drag of fiscal belt tightening. And it all began tipping over the edge in mid-2016.

But that changed with Trump election. Trumponomics has been all about restoring growth and breaking from the rut of economic stagnation. And a key pillar in that plan has been infrastructure and government spending.

On that note, he’s been pushing for a trillion dollar infracture spend over 10 years. And as we’ve discussed, while adding debt isn’t popular for the politicians to approve, natural disasters last year gave them an excuse to approve spending packages. Fast foward just six months and we’ve had more than $200 billion in aid approved from Congress. And now we’ve had an increase of $400 billion in government spending as part of the lastest government budget.

So the government spending piece has been in motion. And expect the rest of the world to follow. As we’ve discussed in recent weeks, we’ve seen the populist push back across the world, from Grexit, to Brexit, to the Trump vote, and now to the “Italy first” movement. The real fight in the “populist movement” is against economic stagnation. And much of that is due to mistakes on policy in response to the global economic crisis. And the core mistake has been austerity. Growthsolves a lot of problems.

What about the debt?

The media loves to talk about the $20 trillion dollar debt load, as if we are going to default and/or the rest of the world is going to dump our Treasuries and send interest rates skyrocketing and implode our economy.

Government debt and deficits are judged (by global trade partners, allies, global allocators of capital) on a relative basis – size relative to GDP. Again, our debt relative to GDP has ballooned since the global financial crisis. But it also has for everyone else in the world. That’s why people/countries are still plowing money into our Treasury market for virtually no return, because lending the U.S. money is still the safest place and way to preserve wealth.

The only alternative in this post global financial crisis environment is to focus on growth. Growth can solve a lot of problems, including the debt and deficit relative to GDP problems. As growth goes up, our debt relative to size of the economy goes down.

If we get the economy back on a sustainable growth path, then, in good times, we can work on the structural flaws that led us to the crisis. That’s the only option.

So, when we look at the components of GDP, the policy execution in Washington has been driving lift-off in all of the components. And yet the experts have still underetimated the potential for a growth boom. We’ve talked about the positive surprises that are coming down the pike in consumption, investment and govenment spending. Tomorrow, we’ll take a look at the trade piece.

We’ve talked the past couple of days about economic growth and the likelihood that we’re just beginning to see the positive surprises from Trumponomics materialize in the economic data.

Yesterday we talked about the consumption component of GDP. Today, we’ll take a look at investment.

Businesses invest when they’re confident about the outlook. And that was anything but the case for the decade following the global financial crisis.

Why? Because the politicians spent their time playing politics in Washington, instead of addressing an economy that was in desperate need of fiscal stimulus and structural change. Instead, they swung the regulatory pendulum too far in the opposite direction. And they played political football with debt and deficits, instead of acting to restore growth and stability. They stifled growth, just as the Fed was desperately throwing everything at the economy to keep it going. And it was all coming to a head by mid-2016 when global interest rates started turning negative.

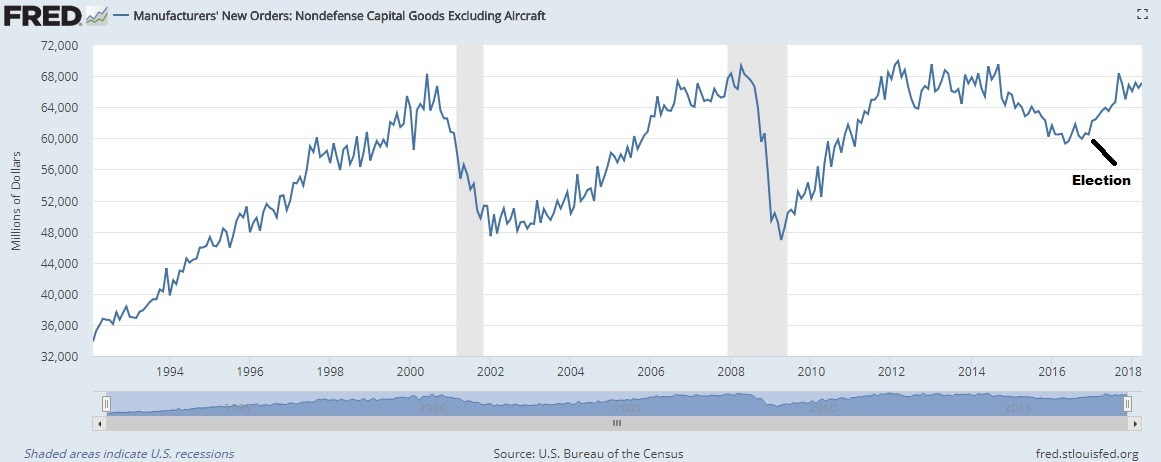

But with the election came optimism. There was at least a chance of a return of good economic times (not just domestically but globally). We had a President with an aggressive economic stimulus plan, and a Congress in place to approve it. With that, small business optimism popped and has soared to record highs.

And companies are now investing again. Capital goods orders (the chart below) are nearing record highs again.

Get this: An ISM survey shows businesses were forecasting just 2.7% capital spending growth for 2018 when they were asked back in December. When they were asked again last month, they revised that number UP to 10.1% growth. A big positive surprise coming down the pike.

Again, as with the consumption picture we talked about yesterday, not only is the back drop solid, but we have stimulus that is still in the early stages of feeding through the economy, which is setting the table forpositive surprises in the economic data as we head toward the second half of the year.

And with that, we finally have the pieces in place for the aggressive bounce back in growth that is characteristic of post-recession recoveries. And that should continue to fuel stocks.