Remember, this (animal spirits) is the element that economists and analysts can’t predict, and can’t quantify. It’s not in the forecasts. This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mistrust of the system. All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindsethas been underway since the night of the election. And that gives way to a return of animal spirits.

Higher stock prices tend to beget higher stock prices. Trust me, individual investors that haven’t been believers will be calling their financial advisors and logging in to their online brokerage accounts over the coming days. Institutional investors that haven’t been believers, that have been underweight stocks, will be beefing up exposure if they want to compete with their peers (and keep their jobs).

And not only do higher stock prices lead to higher stock prices, but higher stock prices tend to make people feel more confident about the economy, which begets a better economy.

Add to this, the psychological value of Dow 20,000 could finally be a turning point in the divergence of sentiment toward the Trump Presidency. It may serve as a validation marker for those that have been on the fence. And for those in opposition, as I’ve said before, growth solves a lot of problems! When the college grad that’s been relegated to a 10-year career as a barista begins to see signs of opportunity for a better career and a better future, in a stronger economy, the sands of Trump sentiment can shift quickly.

Cleary, Trump entered with a game plan that can pop economic growth. And he’s going 100 miles an hour at executing on that plan. For markets, what he’s doing is creating a sense of certainty for investors. They know what he’s promised, and now they know that he appears to intend on delivering on those promises. And the coordination of growth policies, along with ultra-easy monetary policy (even with tightening in view) serves as risk mitigators for markets. It should limit downside risk, which is what investors care most about. How?

Remember, even at Dow 20,000, stocks are still extremely cheap.

Here’s a review on why …

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 48% by the middle of this year. We’re still making up for the lost growth of the past decade. And there’s a lot of ground to make up.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year. That’s an S&P 500 earnings estimate of $133.64 times a P/E of 20 equals 2,672 on the S&P 500.

Reason #3: The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 37% higher.

With this in mind, we are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The S&P 500 traded up to new record highs today. This morning the new President had three more big American business leaders (the car makers) in the White House for a face-to-face.

The three big American car makers all had big stock performance on the day, and their leaders walked away with very positive remarks (not dismay). It turns out that logical business operators like the prospects of doing business with the tailwinds of pro-growth economic policies.

Now, with Obamacare on the chopping block for the new administration, today let’s take a look what healthcare stocks might do.

Healthcare stocks in general have been beaten up since July of 2015, when a Republican Congress brought a vote to repeal Obamacare. The S&P 500 is up 7% from that date. The XLF (the ETF that tracks healthcare stocks) is down 9% in the same period.

Before that, Obamacare had been a money printing machine for much of the healthcare industry.

In this chart below, of the health insurance provider, Aetna, you can see the impact of Obamacare on the stock.

And here’s a look at the hospital company, HCA, also a big winner under Obamacare.

So what happens under Trump care? Trump has said he wants to keep people insured. It sounds like a rework to a more competitive system, rather than a tear down and rebuild. The first sign of visibility on a new plan is probably the greenlight to buy the healthcare ETF, and maybe the under performers in the Obamacare era.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The new President Trump has wasted no time on carrying out his plan on trade. He met with 12 major U.S. company leaders today and told them that they would pay to build outside of the U.S., but (importantly) they would save to build here. And he wrote an executive order to withdraw from the Trans-Pacific Partnership, and one to renegotiate NAFTA.

There are plenty of people that have focused on the risks and the dangers with the Trump trade policies. Meanwhile, those most directly affected aren’t quite as draconian on the outlook — quite the opposite. The executives that have walked out of Trump Tower, and now the White House have largely been optimistic. The same is said for trade partners. Whether they mean it or not, they understand the value of doing business with the U.S. consumer.

As I’ve said, there are clear opportunities for win-wins – especially in a world that must rebalance trade to avoid more cycles of the booms and busts, like the boom-bust we experienced over the past two decades. The administration has the leverage of power (with a Republican Congress), but they also have the leverage of rewards. Despite what the media tells us, behind closed doors the new administration seems to negotiate by carrot rather than stick. Trump comes to meetings bearing gifts, and that creates buy-in.

When you bring American CEOs in and tell them that you’re going to give them a 20 percentage point tax cut, you’re going to slash the regulation burden (by “75%” as he said today), you’re going to give them a 30+ percentage point tax cut on repatriating offshore money, and your going to launch a trillion dollar infrastructure spend, all in an effort to juice the economy to a 4%+ growth rate, they’re going to be very excited — even if you tell them they can no longer access the cheapest production in the world.

In the end, they’d rather have a hot economy to sell into, than a stagnant economy, even if it comes with a higher cost of production. And we may find that, in the end, the after-tax profit margins of these big U.S. corporates may be better given all of these incentives, even if they make things here. Better revenues, and maybe better margins to go with it.

Remember, the optimism of U.S. small business owners made the biggest jump since 1980 on the prospects of growth-friendly Trump policies. GDP equals Consumption + Investment + Government Spending + Net Exports. Ultra easy monetary policies have made borrowing cheap, saving expensive and created the economic stability necessary to get hiring over the past several years. That has all kept consumption going.

The “build it here” policies are a recipe for capital investment to finally ramp up. Add to that, a big government infrastructure spend, and we’re getting the pieces of the puzzle in place to see much better economic growth. A hotter U.S. economy will mean a hotter global economy. With that, I suspect net exports will ultimately pick up as well, with a healthier, more sustainable global economy.

On that note, if we look at the USD/Mexican Peso exchange rate as a gauge of trade partner health, we’ve seen the peso hit hard through the campaigning period under the protectionist fears of a Trump administration. Interestingly, since the inauguration, the peso has been strengthening, even as President Trump signed an executive order today to renegotiate NAFTA. The message behind that usually means: the U.S. does better, Mexico does better.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

dell, whirlpool, ford, johnson and johnson, lockheed, arconic, u.s. steel, tesla, under armour, international paper, corning, trump, white house

President Trump officially took office today. From the close of business on November 8th, as people across the country were still voting, the S&P 500 has climbed 6% – from election night through today. The dollar index has risen 2.8. The broad commodities index is up 6%. The 10 year Treasury note is down 4% — which means the yield is UP from 1.80% to about 2.50%.

His policy agenda has clearly been a game changer.

But if you recall, the broad sentiment going into the election was that a Trump Presidency would cause a stock market crash. These were people that weren’t calibrating the meaningful shift in sentiment that came from projecting pro-growth policies in a world that has been starved for growth. That event (the election) alone did more to cure the global deflation risk than the trillions of dollars that central banks have been pouring into the global economy.

But many still aren’t buying it. I don’t often read financial news. I’d rather look at the primary sources (the data or hear from the actors themselves/ the horse’s mouth) and interpret for myself. But today, I had a look across the web. Four of the five top headlines on a major financial news site, on inauguration day, ranged from negative to doom-and-gloom — all laying blame on the dangers of Trump.

Because Trump has talked tough on trade, the common threat most refer to is a potential trade war. But remember, Trump has also talked tough on U.S. companies moving jobs overseas. Thus far, he hasn’t created enemies, he’s gotten concessions and has created allies. He’s used leverage, and he’s negotiated win-wins. Expect him to do the same with trade partners. With pro-growth policies coming down the pike and a meaningful pop in U.S. economic growth coming, no country, especially in the current state of the global economy, will want to be locked out of trade with the United States.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The Treasury Secretary nominee was being “grilled” by Congress today. I want to talk a bit about this hearing because it brings up the subject of the housing crisis. The who and the whys.

First, Mnuchin is a Wall Street guy. Even worse, he’s a hedge fund and Goldman Sachs guy. That’s like blood in the water for the sharks in Congress. They get to put on a show with live TV cameras in the room, publicly showing disgust for Mnuchin (and those like him), to cozy up the less informed segment of the country. And they get to project the blame for many things in life on the rich and their “bottom-line” business world.

This is a stark contrast to a decade ago. The media, especially, was in the business of making guys like this out to be super heroes. They wrote about them as mythical creatures – the world’s gene pool winners: the best and the brightest.

But times have changed.

In the hearing today, Mnuchin was accused of everything from tax evasion to unfairly kicking an 80-year old woman out of her house in Florida. Sounds like a really bad guy.

Though it appears that he had IRS compliant offshore accounts (not tax evasion, but tax compliant). And his company had purchased defaulted mortgages, claimed the collateral (the house) and sold the collateral for a profit.

So, just as you and me may take a tax deduction for our children, and just as an individual may sell his/her house for a profit, perhaps Mnuchin made rational financial decisions and followed the laws that were created by Congress.

So if we can’t blame Mnuchin and Goldman Sachs for nearly blowing up the global economy, who can we blame.

With all of the complexities of the housing bubble and the subsequent global financial crisis, it can seem like a web of deceit. But it all boils down to one simple actor. It wasn’t Wall Street. It wasn’t hedge funds. It wasn’t mortgage brokers. These entities were operating, in large part, from the natural force of economics: incentives.

It wasn’t even the government’s initiative to promote home ownership that led to the proliferation of mortgages being given to those that couldn’t afford them.

So who was the culprit?

It was the ratings agencies.

Housing prices were driven sky high by the availability of mortgages. Mortgages were made easily available because the demand to invest in mortgages, to fund those mortgages, was sky high.

But what drove that demand to such high levels?

When the mortgages were combined together in a package (securitized as a mix of good mortgages, and a lot of bad/higher yielding mortgages), they were bought, hand over fist, by the massive multi-trillion dollar pension industry, banks and insurance companies. Yes, the guys that are managing your pension funds, deposit accounts and insurance policies were gobbling up these mortgage securities as fast as they could, but ONLY because the ratings agencies were stamping them all with a top AAA rating. Who would encourage such a thing? Congress. In 1984 they passed a law making it okay for banks, pension funds and insurance companies to buy/treat high rated secondary mortgages like they would U.S. Treasuries.

So as investment managers, in the business of building the best performing risk-adjusted portfolio possible, and in direct competition with their peers, they couldn’t afford NOT to buy these securities. They came with the safest ratings, and with juicy returns. If you don’t buy these, you’re fired.

To put it all very simply, if these securities were not AAA rated, the pension funds would not have touched them (certainly not to the extent).

With that, if the there’s no appetite to fund the mortgages, the ultra-easy lending practices never happen, and housing prices never skyrocket on unwarranted and unsustainable demand. The housing bubble doesn’t build, doesn’t bust, and the financial crisis doesn’t happen.

That begs the question: Why did the ratings agencies give a top rating to a security that should have received a lower rating, if not much lower?

First, it’s important to understand that the ratings agencies get paid on the products they rate BY the institutions that create them. That’s right. That’s their revenue model. And only a group of these agencies are endorsed by the government, so that, in many cases, regulatory compliance on a financial product requires a rating from one of these endorsed agencies.

So as I watched the grilling session of Mnuchin today by Congress, these are the things that crossed my mind.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

As we kick off inauguration week, we have a continuation of this “buy the rumor, sell the fact” trade going on in markets.

We often see this phenomenon–it’s a reflection of investors pricing new information in anticipation of an event, and then selling into the event on the notion that the market has already valued the new information. And as we discussed last week, it looks like we’ve already been working on this “sell the fact” phase. Stocks have stalled, the dollar has pulled back a bit and global interest rates have slid off of the post-election highs. But as I said, these retracements should be shallow and short-lived.

Why? Because we appear to finally be in an environment where optimism (not hope) is outweighing fear. Contrary to the narrative of skepticim coming from the media, the markets, the data and the players are all sending very positive signals on the policy outlook.

The media has warned about the dangers of Trump’s rhetoric. Meanwhile, those that have been most directly targeted haven’t become enemies, they’ve quickly become allies and advocates of the Trump administration, making concessions and buying into the growth outlook. We’ve seen it at the corporate level (from GM to Alibaba). And we’ll likely see it at the sovereign level. The threats of taxes and fines have leveraged jobs with U.S. corporates. Tariffs can leverage better trade deals in a world and time that everyone can greatly benefit from better U.S. growth, which can ultimately lead to better and more sustainable global growth.

On the data front, small business optimism is running at the highest level in 37 years. And, as we’re getting into the heart of earnings seasons, the positive surprises are already coming in bigger and at a hotter pace. That’s for the fourth quarter, with just a sliver of post-election certainty priced in.

Add to that, the most troubled industries through the post-financial crisis period have been energy and financials. Financials now have the tailwind of rising interest rates and an outlook for softer regulation. Energy companies have spent that past couple of years cutting costs and reducing debt in the oil price crash. With oil back above $50 and with good prospects to go higher as they ramp up production, they will become earnings machines. This is all fuel for hotter earnings and higher stocks.

Plus, on the earnings note, people are just beginning to wake up to the fact that a better growth environment and a dramatic cut in the corporate tax rate will pump up broad market earnings next year–perhaps as much as 15%-20% better than what’s already projected for 2017.

With all of this in mind, it’s unlikely that investors will retrench over the coming months and wait for proof that Trump promises will be kept and Trump policies will be executed well. Instead, following the swearing in of the new President on Friday, we’ll probably see the “reflation” rally resume.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Jobs, jobs everywhere there’s jobs. The President-elect yesterday said he will be the “greatest job creator God ever created.”

Since December, when the President-elect announced that Carrier, an air conditioner manufacturer in Michigan, would keep 1,000 jobs in the U.S. instead of moving them to Mexico, other companies have been lining up to announce big, bold hiring plans.

It was immediately clear that Carrier won priceless exposure and good-will. From that point, the Japanese billionaire Masayoshi Son took a visit to Trump Tower and followed with an announcement that his Softbank technology holdings company would invest $50 billion in U.S. businesses and create 50,000 new jobs. Softbank owns more than 80% of Sprint, and Sprint has followed with an announcement of 5,000 jobs to come.

Alibaba’s founder Jack Ma visited Trump Tower yesterday and left saying he would create 1 million jobs in the U.S.

Amazon, who’s CEO Jeff Bezos had a visit to Trump Tower last month, said today they plan to add 100k jobs.

Not to be outdone, Taco Bell (part of YUM Brands), said today it would add 1.6 million jobs in the U.S. Does this mean Taco Bell is about to go on a massive expansion increasing their store count by 5x — putting a Taco Bell on every corner in America?

Or, is this all just a public relations ploy? Are they all hoping to gain favor with the administration? Yes and yes. But it’s also all self-reinforcing. A better outlook for jobs is driving confidence. Confidence can drive a better outlook for jobs. More employed, more confident consumers can drive economic growth. And better growth drives more jobs.

Now, all of this said, the headline unemployment number is already down to 4.7% (near what is considered “normal”). The number that measures underemployed and those that have stopped looking is down to 9.2%. It’s much higher than the headline rate, but relative to history, it’s returning close to normal levels too. With the prospects of hotter growth coming, and new job creation, we could be headed for a very tight labor market. What does that mean? Higher wages are coming, to finally begin making up for two decades of wage stagnation.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

For two full months the Trump rally has consisted of higher stocks, higher yields, a higher dollar and higher commodity prices — all on the prospects of hotter growth and a sustainable period of prosperity ahead.

Since the night of November 8th, it’s been “buy it now, prove it to me later” market. But people are expecting there will be a period of time where the markets begin trading in “prove it to me” mode.

Often we see a “buy the rumor, sell the fact” phenomenon in markets — it’s a reflection of investors pricing new information in anticipation of an event, and then selling into the event on the notion that the market has already valued the new information. With that, the period surrounding the January 20th inauguration could be the “sell the rumor” moment (in fact, we may be working on it now).

Many are hoping it could be the second chance given to those that have been left behind in the great Trump reflation rally. The question is, how deep or shallow that correction might be, and how long or short-lived it might me.

I would argue, it’s going to short-lived and shallow (maybe very shallow), for all of the reasons I’ve discussed in this daily note, not the least of which, is a world starving for a return to meaningful and sustainable growth, and the perception that this is the best chance we’ve had and might have, to get the global economy back on track. Trump’s tone today, in his press conference, indeed, indicated that he would waste no time executing on his plan. That favors a short-and-shallow correction scenario for the Trump rally. And shallow corrections are typical of strong trending markets.

With that said, since the election, here’s a view of key markets (taking the last price before the election night whipsaw):

The yield on the 10-year has gone from 1.85% to over 2.64% on the Trump effect. But despite a surprisingly hawkish Fed on December 14th, and even more hawkish fundamental data since, the high in yields, thus far, was marked the day after the Fed meeting last month. And today yields traded just below 2.33%, the lowest since November 30th! For technicians, the 38.2% (Fibonacci) retracement of the entire move is 2.34%. That would be considered a shallow retracement.

The dollar (index) has gone from 97.68 to 103.82, and today trades at 101.28 which is the lowest level since December 14. Commodities (the broad commodity index) have gone from 183 to 193, and today trades at 191. Both have room for another 1% or so lower. The dollar looks very strong.

What about stocks? The S&P 500 has gone from 2,138 to 2,278, and now trades at 2,262. A shallow retracement for stocks of the Trump rally would be about 2,225 (which is about 2% lower from here). Given the policy outlook, those wishing for something deeper may not get the chance – a couple of percentage points from here may be the gift.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

This morning we got a report that small business optimism hit the highest level since 2004, on the biggest jump since 1980. This follows a big jump in December, which obviously follows the November elections.

Small business owners that have survived the storm over the past nine years, most likely have had credit lines pulled, demand for their products and services crushed, and have slashed their workforce. If they were able to piece it together to continue on, they’ve operated as lean as possible, and they’ve slowly seen it all recover. And finally, over the past couple of years, they’ve likely had banks calling offering them money again. But, given the scars of the financial crisis, taking on debt again (or more debt) in an uncertain world, many have turned it down.

But if you’re going to dip a toe in the water again, take on some risk to grow your business (to expand, to hire, to build inventories), small business owners are saying now is the time. They are buying into what the Trump agenda is promising–a “dynamic booming economy.”

You can see that reflected in this chart…

The survey shows that 50% of small business owners expect the economy to improve. That’s the most in 15 years. With that, they think it’s a good time to expand. And they expect higher sales coming down the pike, so they’ve been building inventories.

As we know, in the recovery that was manufactured by the Fed (and other central banks), Main Street didn’t participate–trillions of dollars spent and little impact on the real economy. But this survey shows that the Trump effect is already doing what nine years, and trillions of dollars of monetary stimulus and intervention, couldn’t do. Most of the small business sentiment data has now returned to pre-crisis levels, just on the pent up demand that has been unleashed by the prospects of a return to prosperity.

This number tends to correlate highly with consumer confidence numbers. Consumer confidence numbers drive consumption. And consumption contributes about two-thirds of GDP. By restoring confidence, the Trump effect on growth can be self-fulfilling.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

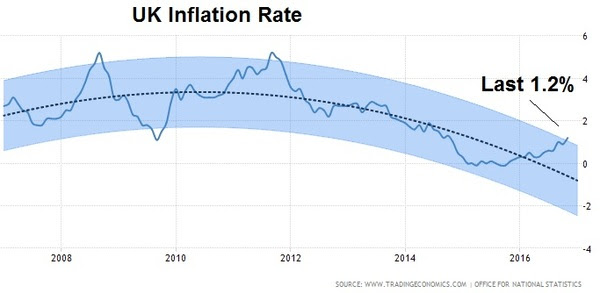

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

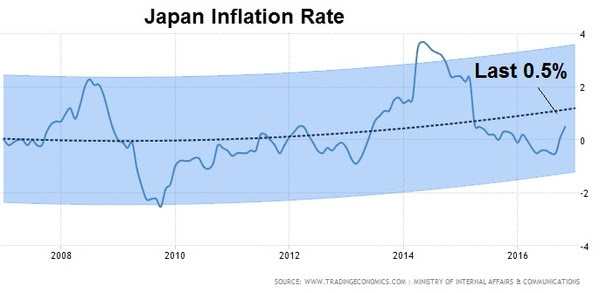

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

President Trump officially took office today. From the close of business on November 8th, as people across the country were still voting, the S&P 500 has climbed 6% – from election night through today. The dollar index has risen 2.8. The broad commodities index is up 6%. The 10 year Treasury note is down 4% — which means the yield is UP from 1.80% to about 2.50%.

President Trump officially took office today. From the close of business on November 8th, as people across the country were still voting, the S&P 500 has climbed 6% – from election night through today. The dollar index has risen 2.8. The broad commodities index is up 6%. The 10 year Treasury note is down 4% — which means the yield is UP from 1.80% to about 2.50%.