For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

Brexit. Russia. Trump’s protectionist threats. Trump’s inability to get policies legislated. The French election.

The bears, those looking for a recession around the corner and big slide in stocks, are losing ammunition for the story.

With the threat of instability from the French election now passed, these are two of the more intriguing catch-up trades.

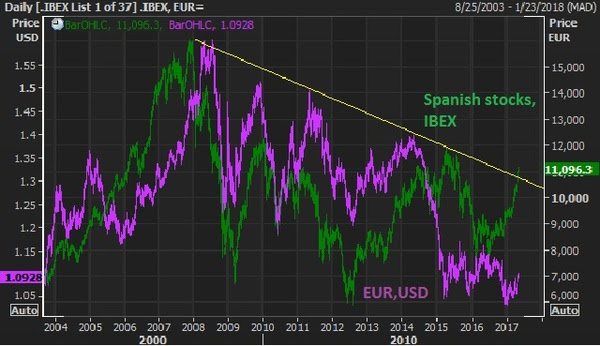

In the chart above, the green line is Spanish stocks (the IBEX). U.S., German and UK stocks have not only recovered the 2007 pre-crisis highs but blown past them — sitting on or near (in the case of UK stocks) record highs. Not only does the French vote punctuate the break of this nine year downtrend, but it has about 45% left in it to revisit the 2007 highs. And the euro, in purple, could have a dramatic recovery with the cloud of French elections lifted, which was an imminent threat to the future of the single currency.Next … Japanese stocks. While the attention over the past five months has been diverted toward U.S. politics and policies, the Bank of Japan has continued with unlimited QE. As U.S. rates crawl higher, it pulls Japanese government bond yields with it, moving the Japanese market interest rate above and away from the zero line. Remember, that’s where the BOJ has pegged the target for it’s 10 year yield – zero. That means they buy unlimited bonds to push the yield back down. That means they print more and more yen, which buys more and more Japanese stocks.

The Nikkei has been one of the biggest movers over the past couple of weeks (up almost 10%) since it was evident that the high probability outcome in the French election was a Macron win.Again, German, U.S., and UK stocks are at or near record highs. The Nikkei has been trailing behind and looks to make another run now, with 25,000 in sight.If you need more convincing that stocks can go much higher, Warren Buffett reiterated over the weekend that this low interest rate environment and outlook makes stocks “dirt cheap.” Last year he made the point that when interest rates were 15% [in the early 1980s], there was enormous pull on all assets, not just stocks. Investors have a lot of choices at 15% rates. It’s very different when rates are zero (or still near zero). He said, in a world where investors knew interest rates would be zero “forever,” stocks would sell at 100 or 200 times earnings because there would be nowhere else to earn a return.

Buffett essentially said at zero interest rates into perpetuity, the upside on the stock market (and any alternative asset class with return) is essentially infinite, as people are forced to find return by taking risk. Why you would buy a treasury bond that has no growth, and little-to-no yield and the same or worse balance sheet than high quality dividend stock.

This “forcing of the hand” (pushing investors into return producing assets) is an explicit objective by the interest rate policies of the Fed and the other major central banks of the world. They need us to buy stocks. They need us to spend money. They need economic growth.

If you have an brokerage account, and can read a weekly note from me, you can position yourself with the smartest investors in the world. Join us in The Billionaire’s Portfolio.

As we discussed last week, we should expect more volatility in markets in the coming months, with the continued discovery surrounding Trump Policies (timing, size) and with UK/EU Brexit negotiations officially opening. That’s a dose of unknowns which should send stocks swinging around quite a bit more than we’ve seen for the past four months.

Remember, on Friday I noted the message the bond market was sending — with market interest rates (U.S. 10 year yields) closing the week, and quarter, at 2.39%. That’s almost a quarter point lower than the high that followed the March rate hike (the third in the Fed’s “normalization” process). And it’s about 10 basis point lower than where the 10 year stood going into the December 2015 rate hike. That’s a negative signal. And I suspect stocks will get that message.

With that said, the first day of the second quarter opened today with a slide in stocks, a slide further in yields and a rise in the price of gold.

When stocks go down, people get nervous and buy downside protection. That tends to spike implied volatility. There’s an index that measures that called the VIX.

Let’s talk about the VIX…

The VIX measures the implied volatility of options on the S&P 500. This is a key component in the price investors pay for downside protection on their portfolios.

So what is implied volatility? Implied volatility measures both actual volatilityand the options market maker community’s expectations (or perception of certainty) about future volatility. When market makers feel confident about the stability in markets, implied vol is lower, which makes the price of options cheaper. When they aren’t confident in stability, implied vol goes up, which makes the price of an option go up. To compensate those that are taking the other side of your trade, for the lack of predictability, you pay a premium.

You can see in the chart below, vol is very, very low — but has been ticking up.

Still, it takes a significant event – a high dose of uncertainty – to create a spike in implied volatility.

That spike tends to correlate well with a sharp slide in stocks. Otherwise, we’re looking at a garden-variety correction in stocks — and that’s what this low vol environment is spelling out.

This will be an interesting week. We had almost three months of optimism priced into global markets following the November 8th elections. And then the tide turned when Trump gave his speech to the join sessions of Congress.

This is the buy-the-rumor sell-the-fact phenomenon we’ve discussed. People bought on anticipation of a big policy shift. And now they’re taking profit (raising cash) waiting to see it all executed — the prove-it-to-me phase.

I think we’re beginning to see the same phenomenon unfold in the Brexit saga. Brexit came before Trump, but the cycle has been slower and longer. Much like the Trump trend, the Brexit news started with an initial “sell everything” on the fear of the unknown, but soon thereafter, the “buy on anticipation of something better” prevailed. But it’s looking very vulnerable now to a turn in the tide.

On Friday, we looked at this next chart. This trend higher in UK stocks looks much like the Trump trend in U.S. stocks – a nice 45 degree climb from June of last year.

But as we discussed on Friday, the “prove-it-to-me” phase looks set to arrive this week in the Brexit story. With that, here’s what the chart looks like today …

This nine-month trend line in UK stocks gave way today – in part because of the softening in expectations about Trump policies, but largely because the UK Prime Minister is expected to officially notify the European Union on Wednesday, of the UK’s exit from the EU. Again, this would start the clock on the two year wind-down of the UK constituency in the EU. And the official negotiations will begin, on what the UK/EU relationship will look like – namely, on trade.

Expect the negotiations to be ugly in the early stages. Why? Because there is a lot to lose if it looks too easy. The future of the European Union and the common currency (the euro) hang in the balance on these negotiations. The most important job of EU officials, at this stage, is keeping other EU members from hitting the eject button, following the lead of the UK. A domino effect of exits would kill the EU and it would be the end of the euro. And that would have huge, destabilizing global ramifications.

With all of this in mind, it’s very likely that after long period of ultra-low volatility in markets, things will be a little more dicey in the months ahead. That should keep pressure on yields and should keep the correction in U.S. stocks intact.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Over the past week, I’ve talked about the potential for disruption in what has been very smooth sailing for financial markets (led by stocks). While the picture has grown increasingly murkier, markets had been pricing in the exact opposite – which makes things even more vulnerable to a shakeout of the weak hands.

With that, it looked like we are indeed working on a correction in stocks. But it’s not just because stocks are down. It’s because we have some very important technical developments across key markets. The Trump trend has been broken.

Let’s take a look at the charts …

The above chart is the S&P 500. We looked at a break in the futures market last week. Today we get a big break in the cash market. This trendline represents the nice 45 degree climb in stocks since election night on November 8th. We have a clean break today.

Stocks ran up on the prospects that Trumponomics can end the decade long malaise in, not just the U.S. economy, but the global economy too. With that, the money that has been parked in U.S. Treasuries begins to leave. Moreover, any speculators that were betting the U.S. would follow the world into negative rate territory run for the exit doors. That sends Treasury bond prices lower and yields higher (as you can see in the chart above). So today, we also get a break of this “Trump trend” in rates as well (the yellow line). Remember, this is after the Fed’s rate hike last week — rates are moving lower, not higher.

Next up, gold …

I talked about gold yesterday — as being the clearest trade (higher) in an increasingly murkier picture for global financial markets. You can see in the chart above, gold is now knocking on the door of a break in this post-election Trump trend.

Remember, we’ve talked about the buy-the-rumor sell-the-fact phenomenon in markets. The beginning of the Trump trend in stocks started on election night (buying “the rumor” in anticipation of pro-growth policies). The top in stocks came the day following the President’s speech to the joint sessions of Congress (selling “the fact”, entering the “show me” phase).

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recent addition to the portfolio – a stock that one of the best activist investors in the world thinks will double.

We had a heavy event calendar last week for markets, with the Fed, BOJ and BOE meetings. And then we had the anticipation of the G-20 Finance Minister’s meeting as we headed into the weekend.

As I said to open the week last week, markets were pricing in a world without disruptions. But disruptions looked likely. Still, the week came and went and stocks were little changed on the week, but yields came in lower (despite the Fed’s third rate hike) and the dollar came in lower (again, despite the Fed’s third rate hike).

Is that a signal?

Maybe. But as we discussed on Friday, the divergence between market rates and the rate the Fed sets is part central bank-driven Treasury buying (from those still entrenched in QE — Japan, Europe), and part market speculation that higher rates are threatening to the economy, and therefore traders sell short term Treasuries (rates go higher) and buy longer term Treasuries (rates go lower). With that, the Fed has been ratcheting the Fed Funds rate higher, now three times, but the 10 year government bond yield is doing nothing.

As for the dollar, if your currency has been weak, no one wanted to head into a G-20 Finance Ministers meeting and sit across the table from the new Treasury Secretary under the Trump administration (Mnuchin) and be drawn into the fray of currency manipulation claims. With that, the dollar weakened across the board last week.

All told, we had little disruption last week, but things continue to look vulnerable this week. Today we have the FBI Director testifying before Congress and acknowledging an open investigation of Trump associates contacts with Russia during the election. Fed officials have already been out in full force today make a confusing Fed picture even more confusing. And it sounds like the UK will officially notify the EU on March 29 that they will exit.

With all of the above in mind, and given the growth policies from the Trump administration still have little visibility on “when” they might get things done, the picture for markets has become muddied.

This all makes stocks vulnerable to a correction, though dips should be met with a lot of buying interest. Perhaps the clearest trade in this picture that’s become more confusing to read, is gold.

Gold jumped on the Fed rate hike last week, and Yellen’s more hawkish tone on inflation. If she’s right, gold goes higher. If she’s wrong, and the Fed has made a big mistake by hiking three times in a world that still can’t sustain much growth or inflation, gold probably goes higher on the Fed’s self-inflicted wounds to the economy.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Following the Fed yesterday, we heard from the Bank of Japan overnight, and the Bank of England this morning. As for Europe, we heard from the ECB last week.

Coming into this week we’ve had this ongoing dynamic, for quite some time, of the Fed going one way on rates (up) and everyone else going the other way (cutting rates, QE, etc.).

That’s been good for the dollar, as global capital tends to flow toward areas with rising interest rates and better growth prospects. That combination tends to mean a rising currency and rising investment values. What really determines those flows though, is the perception of how that policy spread, between countries, may change. Most recently, that perceived change in the spread has been in favor of it growing, i.e. Fed policy tighter or at least stable, while other spots of the world considering even easier on monetary policy.

That divergence in policy has been bad for currencies like the euro, the pound and the yen. But that hit to the currency is part of the recipe. It promotes higher asset prices, better exports and growth. And as Bernanke says, QE tends to make stocks go up, which helps.

Still, those stocks have lagged the strength in U.S. stocks. With that, over the past six months or so, I’ve talked about the opportunities in European and Japanese stocks for a catch up trade.

While U.S. stocks have continued to set new record highs, stocks in Europe and Japan have yet to regain the highs of 2015 — when the global economy was knocked off course, first by slowing China and a surprise currency devaluation, and later by a crash in oil prices.

With that, if you think Trumponomics marked the end of the decade long deleveraging period (post-financial crisis), and that the Fed is signaling that by ending emergency level monetary policy, then the rest of the world should follow. That means the next move in Europe, Japan, the UK will be toward normalization, not toward more emergency policies.

That means the expectations on the policy gap narrows. With that, we may have seen the bottom in the euro. If negative interest rates and an election cycle that has parties that are outright promising to destroy the euro can’t push it to parity, what can? If it can’t go lower, it will go higher.

And if the euro has bottomed and the next move for the central bank in Europe is tapering, the first step toward ending emergency policies, then this stock market in Europe looks the most intriguing for a big catch up trade – still about 20% off of the 2015 highs and well below the pre-crisis all time highs.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

As we head into the Fed tomorrow, stocks have fallen back a bit today.

Yesterday we looked at the nice 45 degree climb in stocks since Election Day. And the big trendline that looked vulnerable to any disruption in the optimism that has led to that climb. That line gave way today, as you can see.

The run up, of course, was on the optimism about a pro-growth government, coming in after a decade of underwhelming growth. The dead top in stocks took place the day after President Trump’s first speech before the joint sessions of Congress. There is a phenomenon in markets where things can run up as people “buy the rumor/news” and then sell-off as people “sell the fact.”

It’s a reflection of investors pricing new information in anticipation of an event, and then selling into the event on the notion that the market has already valued the new information. It looks like that phenomenon may be transpiring in stocks here, especially given that the timeline of tax reform and infrastructure spending looks, now, to be a longer timeline than was anticipated early on.

And as we discussed yesterday, it happens to come at a time where some disruptive events are lining up this week: from a Fed rate hike, to Dutch elections, to Brexit, to G20 protectionist rhetoric.

Stocks are up 6% year-to-date, still in the first quarter. That’s an aggressive run for the broad stock market, and we’re now probably seeing the early days of the first dip, on the first spell of profit taking.

What about oil? Oil and stocks traded tick for tick for the better part of last year, first when oil crashed to the mid-$20s, and then when oil proceeded to double from the mid-$20s. Over the past few days, oil has fallen out of it’s roughly $50-$55 range of the Trump era. Is it a drag on stocks and another potential disrupter? I don’t think so. Oil became a risk to stocks and the global economy last year because it was beginning to trigger bankruptcies in the American shale industry, and was on pace to spread to banks, oil producing countries and the global financial system. We now have an OPEC production cut under the belt and a highly influential oil man, Tillerson, running the State Department. With that, oil has been very stable in recent months, relative to the past three years. It should stay that way – until demand effects of fiscal policy start to show up, which should be very bullish for oil.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

This week will be a huge week for markets. Stocks continue to hover around record highs. Rates (the 10 year yield) sit at the highest level in three years.

This snapshot alone suggests a world that continues to believe that pro-growth policies “trump” all of the risks ahead. At the very least, it’s pricing in a world without disruptions. But disruptions look likely.

Here’s a look at stocks as we enter the week. Still in a 45 degree uptrend since the election.

But if we take a longer term look, this trendline looks pretty vulnerable to any surprise.

Let’s take a look at the disruptions risks:

There was a chance that the official execution of Brexit may have come as soon as tomorrow — the UK leaving the European Union by triggering Article 50 of the Treaty of Lisbon. That looks unlikely now, but could come in the coming weeks. To this point the Bank of England has done a good job of responding and promoting stability which has led to financial markets pricing in an optimistic outcome.

We have the Fed on Wednesday. They will hike for the third time in the post-financial crisis era. We don’t know at what point higher interest rates, in this environment, might choke off growth that is coming from the fiscal side.

This next chart looks like rates might run to 3% on the 10-year. That would do a number on housing, IF tax reform and an infrastructure spend out of the White House come later than originally anticipated (which is the way it looks).

We also have the Bank of Japan and Bank of England meeting on rates this week. Let’s hope they have a very boring, staying the path, message. That would mean extremely stimulative policies for the foreseeable future 1) in the case of Japan, to continue to promote global liquidity and anchor global yields, and 2) in the case of the UK, to continue to promote stability in the face of uncertainty surrounding Brexit.

Keep this in mind: The Bank of Japan’s big QE launch in 2013 is a huge reason the Fed was able to end QE in the first place, and start its path of normalization. The BOJ launched in April of 2013. Bernanke telegraphed “tapering” a month later. The Fed officially ended tapering on October 29, 2014. Stocks fell 10% into that official ending of Fed QE. On October 31, 2014 (two days later), the BOJ surprised the world with bigger, bolder QE (a QE2). Stocks rallied.

Finally, to end the week, we have a G-20 finance ministers meeting. This is where all of the trade and dollar rhetoric from the new administration will be front and center. So the news/event outlook looks like some waves should be ahead. But any dip in stocks would be a great buying opportunity.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

One of the best investors on the planet, David Tepper, was on CNBC this morning. Let’s talk about how he sees the world and how he is positioned.

What I appreciate about Tepper: He’s a common sense guy.

And his common sense view of the world happens to be in alignment with the view and themes we discuss here every day. So he agrees with me – another thing I appreciate about him.

As you know, Wall Street and the media are always good at overcomplicating the investment environment with their day-to-day hyper analysis. Because of that, they tend to forge a path that moves further and further away from the simple realities of the big picture. That’s actually good. Because it creates opportunity for those that can avoid those distractions.

Right now, as we’ve discussed, the big picture is straight forward. We have a President that wants deregulation, tax cuts and a big infrastructure spend. And we have a Congress in place that can approve it. And this all comes at a time when the world has been in a decade long economic slog following the global financial crisis – in desperate need of growth. With that, we have a Fed that still has rates at very, very low levels. And the ECB and BOJ are still priming the pump with QE.

This is precisely Tepper’s view. He says the bowl is still full, i.e. the stimulus from the monetary policy side is still full, and now we get stimulus coming in from the fiscal side. What more could you ask for (my words) to pump up growth and asset prices, which will likely spill over into a pop in global growth. Still, people are underestimating it. And as he says, the Fed is underestimating it.

Are there risks? Yes. But the probability of growth, with the above in mind, well outweighs the probable downside scenarios. What about execution risk? Even if tax reform and infrastructure are slow to come, Tepper says deregulation is a done deal. It drives earnings and “animal spirits.”

He likes stocks. He likes European stocks. And I think he really likes Japanese stocks, but he stopped short of talking about it (my deduction).

Among the risks: Inflation picking up too fast, which would require the Fed to move faster, which could choke off growth (undo or neutralize fiscal stimulus).

This is why, among other reasons, Tepper’s favorite trade is short bonds. – i.e. higher interest rates. If he’s right and economic growth has a big pop, he wins. If the risk of hotter inflation materializes and rates move faster, he wins.

For context, this is the guy that literally changed global investing sentiment in late 2010 when he sat in front of a camera on CNBC, in a rare high profile TV interview (maybe first), when investing sentiment was all but destroyed by the global financial crisis and the various landmines that kept popping up. Tepper said in a very confident voice that the Fed, by telegraphing a second round of QE, had just given us all a free put on stocks (i.e. the Fed is protected the downside, it’s a greenlight to buy stocks). For all of the market jockeys that were constantly focusing on the many problems in the world, that commentary from Tepper, for some reason, woke them up.

For perspective on Tepper: Here’s a guy that is probably the best investor in the modern era. He’s returned between 35%-40% annualized (before fees) for more than 20 years. He made $7.5 billion in 2009 betting on financial stocks that most people thought were going bankrupt. And he was telling everyone that what the Fed is doing will make ‘everything’ go up. It sparked, in 2010, what is known as the “Tepper rally” in stocks.

When Tepper speaks it’s often smart to listen. And he likes the Trump effect!

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Since going public last week, Snap has had a valuation north of $30 billion. It’s been getting hammered from the highs over the past couple of days. A big component to the rise of Internet 2.0 was the election of Barack Obama. With a change in administration as a catalyst, the question is: Is this chapter of the boom in Silicon Valley over? And is Snap the first sign?

Without question, the Obama administration was very friendly to the new emerging technology industry. One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007, before Obama announced his run for president, and just as Facebook was taking off after moving to and raising money in Silicon Valley (with ten million users). Facebook was an app for college students and had just been opened up to high school students in the months prior to Obama’s run and the hiring of the former Facebook cofounder. There was already a more successful version of Facebook at the time called MySpace. But clearly the election catapulted Facebook over MySpace with a very influential Facebook insider at work. And Facebook continued to get heavy endorsements throughout the administration’s eight years.

In 2008, the DNC convention in Denver gave birth to Airbnb. There was nothing new about advertising rentals online. But four years later, after the 2008 Obama win, Airbnb was a company with a $1 billion private market valuation, through funding from Silicon Valley venture capitalists. CNN called it the billion dollar startup born out of the DNC.

Where did the money come from that flowed so heavily into Silicon Valley? By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S.

When institutional investors see that kind of money flowing somewhere, they chase it. And valuations start exploding from there as there becomes insatiable demand for these new “could be” unicorns (i.e. billion dollar startups).

Who would throw money at a startup business that was intended to take down the deeply entrenched, highly regulated and defended taxi business? You only invest when you know you have an administration behind it. That’s the only way you put cars on the street in NYC to compete with the cab mafia and expect to win when the fight breaks out. And they did. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation. Uber is valued at $60 billion. That’s more than three times the size of Avis, Hertz and Enterprise combined.

Will money keep chasing these companies without the wind any longer at their backs? The favor in the new administration looks more likely to go toward industrials and energy. That would leave the pumped up valuations in some of these internet businesses, that operate with no real plan on how to make money, with a long way to fall.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.