This morning we got a report that smallbusiness optimism hit the second highest level in the 44-year history of the index.

Here’s a look at that history …

optimism

Remember, last year, following the election, this index that measures the outlook from the small business community had the biggest jump since 1980 (as you can see in the chart).

Why were they so excited? For most of them, they had dealt with a decade long crisis in their business, where they had credit lines pulled, demand for their products and services were crushed, healthcare costs were up and their workforce had been slashed. If they survived that storm and were still around, any sign that there could be a radical change coming in the environment was a good sign.

A year ago, with a new administration coming in, half of the smallbusiness owners surveyed, expected the economy to improve. That was the largest agreement of that view in 15 years.

They’ve been right.

Now with an economy that will do close to 3% growth this year, still, about half of small business owners expect the economy to improve further from here.

No surprise, they are more than pleased with the tax cuts coming down the pike. They’ve seen regulatory relief over the past year. And, according the chief economist for the National Federation of Independent Businesses, small business owners see the incoming Fed Chair (Powell) as more favorable toward business (and market determined decisions) than Yellen. And he says, “as long as Congress and the President follow through on tax reform, 2018 is shaping up to be a great year for small business, workers, and the economy.”

This reflects the theme we’ve talked about all year: the importance of fiscal stimulus to bridge the gap between the weak economic recovery that the Fed has manufactured, and a robust sustainable economic recovery necessary to escape the crisis era. This small business survey tends to correlate highly with consumer confidence. Consumer confidence drives consumption. And consumption contributes about two-thirds of GDP. So, by restoring confidence, the stimulative policy actions (and the anticipation of them) has been self-reinforcing.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We have big central bank meetings this week. Let’s talk about why it matters (or maybe doesn’t).

The Fed, of course, has been leading the way in the move away from global emergency policies.

But they’ve only been able to do so (raising rates and reducing their balance sheet) because major central banks in Europe and Japan have been there to pick up where the Fed left off, subsidizing the global economy (pumping up asset prices and pinning down market interest rates) through massive QE programs.

The QE in Japan and Europe has kept borrowing rates cheap (for consumers, corporates and sovereigns) and kept stocks moving higher (through outright purchases and through backstopping against shock risks, which makes people more confident to take risk).

But now economic conditions are improving in Europe and Japan. And we have fiscal stimulus coming in the U.S., into an economy with solid fundamentals. As we’ve discussed, this sets up for what should be an economic boom period in the U.S. And that will translate into hotter global growth. So the tide has turned.

With that, global interest rates, which have been suppressed by these QE programs, will start moving higher when we get signals from the key players, that an end of QE and zero interest rates is coming. The European Central Bank has already reduced its QE program and set an end date for next September. That makes the Bank of Japan the most important central bank in the world, right now. And that makes the meeting next week at the Bank of Japan the most important central bank event.

Let’s talk a bit more about, why?

Remember, last September, the Bank of Japan revamped it’s massive QE program which gave them the license to do unlimited QE. They announced that they would peg the Japanese 10-year government bond yield at ZERO.

At that time, rates were deeply into negative territory. In that respect, it was actually a removal (a tightening) of monetary stimulus in the near term — the opposite of what the market was hoping for, though few seemed to understand the concept. But the BOJ saw what was coming.

This move gave the BOJ the ability to do unlimited QE, to keep stimulating the economy, even as growth and inflation started moving well in their direction.

Shortly thereafter, the Trump effect sent U.S. yields on a tear higher. That move pulled global interest rates higher too, including Japanese rates. The Japanese 10-year yield above zero, and that triggered the BOJ to become a buyer of as many Japanese Government Bonds as necessary, to push yields back down to zero. As growth and the outlook in Japan and globally have improved, and as the Fed has continued tightening, the upward pressure on rates has continued, which has continued to trigger more and more QE from the BOJ – which only reinforces growth and the outlook.

So we have the BOJ to thank, in a pretty large part, for the sustained improvement in the global economy over the past year.

As for global rates: As long as this policy at the BOJ appears to have no end, we should expect U.S. yields to remain low, despite what the Fed is doing. But when the BOJ signals it may be time to think about the exit doors, global rates will probably take off. We’ll probably see a 10-year yield in the mid three percent area, rather than the low twos. That will likely mean mortgage rates back well above 5%, car loans several percentage points higher, credit card rates higher, etc.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We had a jobs report this past Friday. The unemployment rate is at 4.1%. We’re adding about 172k jobs a month on average, over the past twelve months. These are great looking numbers (and have been for quite some time). Yet employees, broadly speaking, still haven’t been able to command higher wages. Wage growth continues to be on the soft side.

With little leverage in the job market, consumers tend not to chase prices in goods and services higher — and they tend not to take much risk. This tells you something about the health of the job market (beneath the headline numbers) and about the robustness of the economy. And this lack of wage growth plays into the weak inflation surprise that has perplexed the Fed. And the weak growth that has perplexed all policy makers (post-crisis). That’s why fiscal stimulus is needed!

And this could all change with the impending corporate tax cut. The biggest winners in a corporate tax cut are workers. The Tax Foundation thinks a cut in the corporate tax rate would double the current annual change in wages.

As I’ve said, I think we’re in the cusp of an economic boom period — one that we’ve desperately needed, following a decade of global deleveraging. And today is the first time I’ve heard the talking heads in the financial media discuss this possibility — that we may be entering an economic boom.

Now, we’ve talked quite a bit about the run in the big tech giants through the post-crisis era — driven by a formula of favor from the Obama administration, which included regulatory advantages and outright government funding (in the case of Tesla). And we’ve talked about the risk that this run could be coming to an end, courtesy of tighter regulation.

Uber has already run into bans in key markets. We’ve had the repeal of “net neutrality” which may ultimate lead big platforms like Google, Twitter, Facebook and Uber, to transparency of their practices and accountability for the actions of its users (that would be a game changer). And we now know that Trump is considering that Amazon might be a monopoly and harmful to the economy.

With this in mind, and with fiscal stimulus in store for next year, 2018 may be the year of the bounce back in the industries that have been crushed by the “winner takes all” platform that these internet giants have benefited from over the past decade.

That’s probably not great for the FAANG stocks, but very good for beaten down survivors in retail, energy, media (to name a few).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

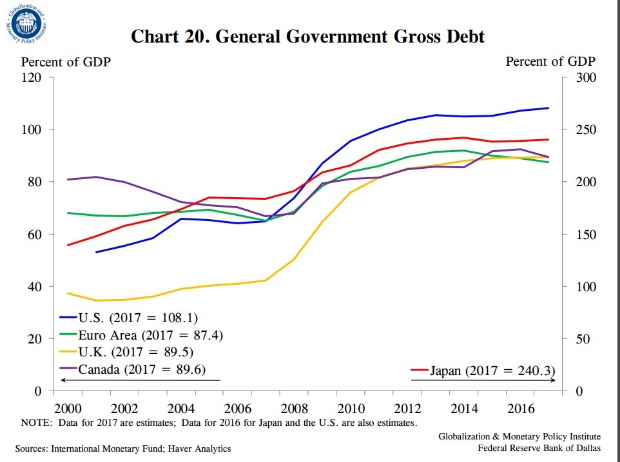

With the potential government shutdown looming, let’s look at some perspective on government debt.

As we discussed early in the week, the policy execution pendulum for the Trump administration has swung over the past four months, from winless to potentially two big wins by the year end.

As I’ve said, with a massive corporate tax cut coming and big incentives for companies to build, invest and bring money back home (from overseas), we should be entering an economic boom period — one we have desperately needed, post-recession, but haven’t gotten.

Still, there are people that hate the tax cut idea. They think the economy is fine shape. And that debt is the problem. The Joint Committee on Taxation is the go to study for those that oppose the tax cuts. The study shows not a lot of growth, and disputes the case that the tax cuts will pay for themselves through growth.

What the headlines that cite this study don’t say, is that the study has huge assumptions that drive their conclusions. Among them, that creating incentives to repatriate $3 trillion in offshore corporate money will only contribute about a fifth of the taxable value of that amount of money. And they assume that the Fed will hike rates at a pace to precisely nullify any gains in economic activity (which wouldn’t be smart, unless they want to go revisit another decade of QE).

Now, with this study in mind, people are fearing the debt implications, on what is already a large debt load. And they fear that global investors might start dumping our Treasuries, as a result.

This has been a misguided fear throughout much of the post-financial crisis environment. Conversely, international investors have flocked into our Treasuries (lending us money), as the safest parking place for their capital. Why?

For perspective on the debt load and the fiscal stimulus decision, as we discussed earlier this week: “The national debt is a big number. But so is the size of our economy – about $19 trillion. Sovereign debt isn’t about the absolute number. It’s about the size of debt relative to the size of the economy. With that, it’s about our ability to service that debt at sustainable interest rates. The choice of austerity in this environment, where the economy is fragile and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession (as it did in Europe). And the outlook for re-emerging would be grim. That would make our debt/gdp far inferior to current levels — and our ability to service the debt, far inferior.”

Add to this, the increase in sovereign debt relative to GDP, has been a global phenomenon, following the financial crisis. Much of it has to do with the contraction in growth and the subsequent sluggish growth throughout the recovery (i.e. the GDP side of the ratio hasn’t been carrying it’s weight).

You can see in the chart above, the increasing debt situation isn’t specific to the U.S.

The euro zone tried the path of austerity back in 2011, and quickly found themselves back in recession, only re-emerging by promising to backstop the failing countries in the monetary union, and launching a massive QE program.

What about the government shutdown threats? Would it derail stocks? Stocks went up about 2% the last time the government shutdown in 2013. Before that was 1995-96 (stocks were flat) – and 1990 (stocks were flat).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

It looks like we’ll get tax cuts approved before year end! And that will give us two of the four pillars of Trumponomics underway in the first year of the new administration.

What a difference four months makes.

Remember, we entered the year with prospects of a big corporate tax cut, a huge infrastructure spend, deregulation and incentives to bring trillions of U.S. corporate money home.

By this summer, the ability to execute on these policies, given the political gridlock and mudslinging, was beginning to look questionable.

The game changer was the hurricanes.

In my note on August 29th, I said: “I think it’s fair to say the optimism toward the President, the administration and Washington policy making has been waning with the lack of policy execution. And from the optics of it all, sentiment couldn’t go much lower. But in markets, turning points (bottoms and tops) in the prevailing trend are often triggered by a catalyst (big trend changes, by some sort of intervention).

With that, the hurricane will likely have little negative impact on overall growth, but it may do something positive for policy making (maybe a turning point).

Given the mess of the political landscape, and an economy that remains vulnerable and in need of fiscal stimulus and structural reform, the crisis in Texas might serve as a needed catalyst: 1) to offer an opportunity for Trump to show leadership in a time of crisis, an opportunity to earn support and approval, and 2) to engage support for rebuilding, not just in Texas but throughout the U.S. (i.e. the much needed economic catalyst of infrastructure spend)…

National crises tend to be unifying. And in the face of national crisis, the barriers to get government spending going get broken down.

So, as we discussed last week, it may be the hurricanes that become the excuse for lawmakers to stamp more spending projects which can ultimately become that big infrastructure spend. And the easing of social tensions and political gridlock on policy making would all be highly positive for the global economic outlook.”

Of course that was followed by the big hurricane in Florida, and then in Puerto Rico. All told, the damages are north of $250 billion.

Congress has approved, to this point, about $60 billion in aid for hurricanes and wildfires (as far as I can track). And that number will likely go much higher — well into nine figure territory (probably more like a quarter of a trillion dollars). For Katrina, the ultimate federal aid disbursed was $120 billion.

On that momentum the first tranche of aid passed back in September, Trump went right to tax cuts. Three months later, and tax cuts are coming.

So, quickly, the policy execution pendulum has swung. This should pop growth nicely next year (and in Q4), which we desperately need to break out of the post-crisis rut of weak demand, slow growth and low inflation.

What about the $20 trillion debt load the media loves to talk about? It’s a big number. So is the size of our economy – about $19 trillion. Sovereign debt isn’t about the absolute number. It’s about the size of debt relative to the size of the economy. With that, it’s about our ability to service that debt at sustainable interest rates. The choice of austerity in this environment, where the economy is fragile and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession (as it did in Europe). And the outlook for re-emerging would be grim. That would make our debt/gdp far inferior to current levels — and our ability to service the debt, far inferior.

On the other hand, with fiscal stimulus underway, don’t underestimate the value of confidence in the outlook (“animal spirits) to drive economic growth higher than the number crunchers in Washington can imagine (the same one’s that couldn’t project the credit bubble, and didn’t project the sluggish 10 years that have followed).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn

Stocks fell sharply this morning, but recovered nearly all the losses from the lows of the day.

Today we got a reminder of the impact that algorithmic trading can have on markets. When the headline hit today about Flynn, here’s what stocks did…

Big institutions have been trading stocks through computer programs for a long time, but the speed at which these algorithms can access markets and information have changed dramatically over the past decade – so has the massive amount of assets deployed through high frequency trading programs. They can remove liquidity very quickly. Combine that with the reduced liquidity in markets that has resulted from the global financial crisis (i.e. the shrinkage of the marketing making community and of hedge fund speculators, and the banning of bank prop trading) and you get markets that can go down very fast. And you get markets that can go up very fast too.

The proliferation of ETFs exacerbates this dynamic. ETFs give average investors access to immediate execution, which turns investors into reactive traders. Selling begets selling. And buying begets buying.

Now, with the Flynn news, Wall Street and the financial media spend a lot of time trying to predict when the market will correct and what will cause it. But as the great billionaire investor, Howard Marks, has said: “It’s the surprises no one can anticipate that move markets. But most people can’t imagine them, and most of the time they don’t happen. That’s why they’re called surprises.”

Still, if you’re not a leveraged hedge fund, this tail-chasing game of trying to pick tops and reduce exposure at the perfect time shouldn’t apply.

More important is the observation that stocks remain cheap at current levels, when we consider valuations in historically low interest rate periods. And we continue to have very low interest rates. So the question is: Is it more likely that corporate earnings will get worse from here, or better from here?

There’s plenty of evidence to suggest the momentum and the fundamental backdrop supports “getting better” from here. And we add to that, the fuel of tax cuts, and earnings should continue to make stocks very attractive relative to a 2.3% ten-year yield.

The Dow is now up 23% on the year. The index that measures the broader market, the S&P 500, is up 18%. This is more than double the performance of the long run compounded average growth rate for the stock market.

People continue to be surprised that policy execution is improving, and that tax cuts are actually coming. And they speculate on whether or not the stock market already has it all priced in. I think the steady rise in stocks is telling them it’s not.

As I’ve said, we remain in an ultra-low interest rate world, where incentives continue to push money into stocks (as the best alternative). And in ultra-low rate environments, historically, the multiple on stocks (the P/E) runs north of 20. It’s 18 right now, on the consensus estimate on next year’s earnings. So on a valuation basis, there’s room. This doesn’t take into account a corporate tax cut that will take the rate from 35% to 20%. That goes right to the bottom line for companies (earnings go UP). When earnings go up, the multiple stocks trade for goes down (stocks get cheaper).

Citibank thinks each 1% cut in corporate taxes will add roughly $2 in S&P 500 earnings. And Citibank says the effective tax rate across the S&P 500 is more like 27%. So a cut to 20% would mean a seven percentage point reduction. This would put next year’s S&P 500 earnings in the mid-$150s, which would put the multiple at 16 to 17 times next year’s earnings.

And don’t forget, we’re getting fiscal stimulus for a reason: to pop economic growth, which has been in a rut (post-crisis), running well south of the 3% long run average growth rate for the economy. The prospects for better growth, means prospects for better earnings. The outlook for better earnings, on a better economy, should also put downward pressure on valuations, making stocks more attractively valued.

In my January 2 note, I said: “there will be profound differences in the world this year, with the inauguration of a new, pro-growth U.S. president, at a time where the world desperately needs growth.” I think it’s safe to say that is playing out—albeit maybe slower and messier than expected.

I also said: “The element that economists and analysts can’t predict, and can’t quantify, is the return of ‘animal spirits.’ This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mistrust of the system. All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset appears to finally be underway. And that gives way to a return of animal spirits, which haven’t been calibrated in all of the forecasts for 2017 and beyond.”

The Fed decision today was a snoozer, as expected. The market continues to think we get a third rate hike for the year in December (fourth since the election).

Thus far, with three hikes, we’ve had just about the equivalent (just shy of 75 basis points) priced-in to the 10-year Treasury market. Yields popped from about 1.70% on election night (just about a year ago) to a high of 2.64%. We’ve had some swings since, but we sit now at roughly 2.40% (70 basis points higher over the past year).

We revisited yesterday, the prospects for some significant wage growth (and therefore inflation), with the fuel of fiscal stimulus feeding into an already tight (but underemployed) labor market.

The Treasury market isn’t pricing that scenario in, at all.

In fact, the yield curve continues to look more like a world that doesn’t fully believe fiscal stimulus is happening (or will happen), and does believe the Fed is more likely damaging the economy through its rate “normalization.”

That’s a bet that continues to underprice the prospects of fiscal stimulus. And, therefore, that’s a bet that continues to be disconnected from the message other key markets are sending. Over the past six months, we’ve talked the case for stocks to go much higher. We’ve talked about the opportunities in European and Japanese stocks (German stocks hitting new record highs and Japanese stocks nearing new 26-year highs today). We’ve talked a lot about the building bull market in commodities. We’ve talked about the positive signals that copper has been sending, as the leading indicator of a global economic turning point. We’ve talked about the outlook for much higher oil prices – oil hit $55 today. (July 30: Explosive Move Coming For Oil And Commodities Stocks).

And oil prices, whether the central banks like to admit it or not, heavily impact inflation, inflation expectations and policy making decisions.

With that, this next chart suggests that market interest rates are about to make a move (higher).

Source: Billionaire’s Portfolio

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Let’s take a look today at what fiscal stimulus might do to inflation.

The central banks have been able to boost asset prices. They’ve been able to restore stability so that people felt confident enough to hire, spend and invest again. But the scars from over-indebtedness have left demand weak. And because of that, despite the recovery of the unemployment to under 5%, the quality of jobs haven’t returned. And, therefore, the leverage to command higher wages hasn’t been there. That’s been the missing piece of the recovery puzzle.

And with that, we’ve had an ultra-low inflation recovery. That sounds great (low inflation).

But inflation at these low levels has had us (through much of the past decade) teetering on the edge of deflation. That’s bad news.

Among the many threats throughout the crisis period, a deflationary spiral was one of the Fed’s most feared. Central bankers can fight inflation (by raising rates). But they can’t fight deflation when consumer psychology takes over. When people hold on to their money thinking things will be cheaper tomorrowthan they are today, that mindset can bring the economy to a dead halt. It’s a formula that can become irreversible.

And that’s what has kept the Fed (and global central banks) sitting at ultra-low levels of interest rates – to keep the recovery momentum moving so that they don’t have to fight a deflationary spiral (as they have in Japan, unsuccessfully, for two decades).

Now, enter fiscal stimulus. We’re getting fiscal stimulus into an already tight employment market.

Real wages (employee purchasing power) has barely budged for two decades. Introducing big tax cuts and government spending into an economy that has low unemployment and the best consumer credit worthiness on record should pop demand. And that should finally give us some wage growth – maybe bigwage growth.

All of the inflationists that thought QE was going to cause hyper-inflation were wrong – they didn’t understand the severity and breadth of the crisis. Now, after global unlimited QE has barely moved the needle on inflation, the inflation hawks have been lulled to sleep. It may be time to wake them up.

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click hereto learn more.

Interest rates and stocks are on the move today (higher), following the vote last night in the Senate to pass the budget. This opens the way for an approval on the tax plan.

As stocks continue to print new record highs, so does policy execution for the Trump administration (the latter the cause, the former the effect).

So we’re seeing more and more of the pro-growth plan fall into place. Markets have been telling us this (betting on this) for a while.

Remember, we talked about the prospects that hurricane aid could kickstart the Trump infrastructure plan (proposed at $1 trillion over 10 years). There’smore progress on that front in the past week.

Among the pillars of Trump’s growth plan, this one (infrastructure/government spending) looked to be among the long shots given the politicians can always play the debt card to fight it. But then the hurricanes hit.

After Irma rolled through Florida the estimated damages for both Harvey and Irma were estimated at $200 billion. Then Hurricane Maria decimated Puerto Rico. Estimated damages there are now $95 billion. I’ve thought we’ll ultimately see a 12-figure package out of Congress in response to the hurricanes. The ultimate federal aid on Katrina was $120 billion.

In September Congress approved $15 billion in aid for hurricane victims. They just approved another $35 billion! This quiet government spending piece, that will substantially grow from here, may turn out to be the most powerful in terms of driving wage growth and economic growth.

So tax reform and infrastructure, two big pillars of Trumponomics continue to progress. And on the deregulation front, Trump has already been aggressively peeling back regulations that have crushed some industries, while ramping UP regulatory scrutiny on Silicon Valley, as we discussed yesterday.

Some of the top venture capitalists in Silicon Valley said this week that they expect to see some failures this year of startups once valued north of a billion-dollar. That’s a result of less money flowing that direction, less government favor, and more money flowing back into publicly traded stocks.

With that in mind, let’s take a look at the chart on Amazon to finish the week …

We talked about Amazon’s miss on earnings back on July 27th as the catalyst to take profit on the FAANG trade (the loved tech giants). The top continues to hold in Amazon.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

The Fed decision today was a snoozer, as expected. The market continues to think we get a third rate hike for the year in December (fourth since the election).

The Fed decision today was a snoozer, as expected. The market continues to think we get a third rate hike for the year in December (fourth since the election).

Let’s take a look today at what fiscal stimulus might do to inflation.

Let’s take a look today at what fiscal stimulus might do to inflation. Interest rates and stocks are on the move today (higher), following the vote last night in the Senate to pass the budget. This opens the way for an approval on the tax plan.

Interest rates and stocks are on the move today (higher), following the vote last night in the Senate to pass the budget. This opens the way for an approval on the tax plan.