|

May 9, 5:00 pm EST

Yesterday we talked about the tool China will use to offset tariffs, if a deal does not materialize and the tariff penalty increases.

They will devalue their currency.

With a “no deal” potential outcome, there’s a lot of wealth in China looking for ways out.

In recent years, they have found a way out through Bitcoin. And, no coincidence, Bitcoin is again on the move.

With that, let’s take a look at the timeline on Bitcoin…

The 2016-2017 ascent of Bitcoin coincided perfectly with the crackdown on capital flight in China. In late 2016, with rapid expansion of credit in China, growing non-performing loans, a soft economy and the prospects of a Trump administration that could put pressure on China trade, capital was moving aggressively out of China.

That’s when the government stepped UP capital controls — restricting movement of capital out of China, from transfers to foreign investment.

Of course, resourceful Chinese still found ways to move money. Among them, buying Bitcoin. And that’s when Bitcoin started to really move (from sub-$1,000 to over $19,000). China cryptocurrency exchanges were said to account for 90% of global bitcoin trading.

Chinese capital flows were confused for Silicon Valley genius.

But in late 2017, China cracked down on Bitcoin – with a total ban. A few months later, Bitcoin futures launched, which gave hedge funds a liquid way to short the madness. Bitcoin topped the day the futures contract launched.

So, as Chinese officials visit the White House for a deal or no deal on trade, China has been moving their currency lower — and bitcoin has (again) been moving higher. Perhaps the Chinese are finding new ways to buy Bitcoin.

If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential.

Join now and get your risk free access by signing up here.

|

May 7, 5:00 pm EST As we get closer to the hard deadline on a U.S./China trade deal, markets are adjusting for the potential of a no deal/ tariff escalation. What does that look like? U.S. stocks are now off 2% from the highs of the year. That still puts us up 15% year-to-date. The bigger adjustment is coming in China. As we discussed yesterday, China is in the position of weakness in these negotiations. The U.S. economy is strong. China’s economy has been very weak. A more expensive and indefinite trade dispute puts downward pressure on both economies (and the global economy), but it puts the Chinese in dangerously slow economy — which becomes politically dangerous for the Chinese Communist Party. As such, here’s what Chinese stocks have done in the past eight days …

|

|

|

And, perhaps as a warning shot, China is starting to move their currency. As we’ve discussed, China has used their currency (a weak currency) as the primary tool to achieve their extraordinary economic ascent over the past two decades — cornering the world’s export market. We should expect, when their backs are against the wall, with a dim economic outlook, they will go back to weakening the yuan. That’s what they have been doing since Trump’s tariff threat on Sunday. They adjusted down the yuan yesterday by almost 1%. That doesn’t sound like much, within China’s currency regime, it’s a big move. We saw a one-off move like that once last year. The other time was August of 2015, which led to fears that China might devalue the yuan. That set off a global market rout. With the above said, China is sending Hui for the meetings that are scheduled to run Thursday and Friday. Hui has been the point-man on trade negotiations. His presence, in light of the tariff threats, give some encouragement that China has intentions to get a deal done. If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential. Join now and get your risk free access by signing up here. |

|

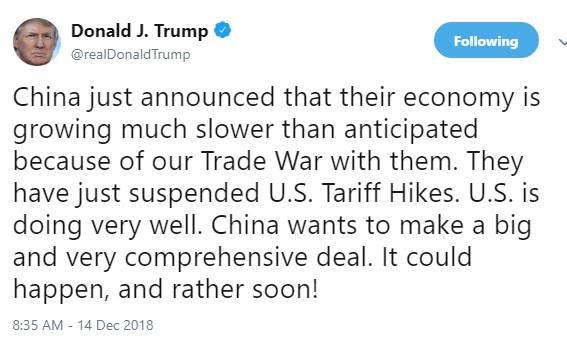

May 6, 5:00 pm EST Late last week, the White House floated the idea that a trade agreement with China could come by this coming Friday (May 10). And then Trump did this yesterday …

|

|

|

Why would Trump risk complicating a deal, even more, by threatening China with a deadline/ tariff increase? Because he has leverage. He has a stock market near record highs, and a strong economy and the winds of ultra-easy global monetary policy at his back. China, on the other hand, has an economy running in recession-like territory, with key data just (recently) bouncing from global financial crisis era levels. And Chinese stocks, after soaring 34% since January 4th, have given back 12% from the highs, in just seven days. And they’ve just fired a ton of fiscal and monetary policy bullets to stimulate the economy – which could be diluted by a more expensive and indefinite trade war. So, Trump has a win-win going into the week. If the threat works, he gets a deal done, and likely gives less to get it done. If China backs off, stocks go down, and he gets the Fed’s rate cut he’s been looking for – stocks go back up. If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential. Join now and get your risk free access by signing up here. |

|

|

|

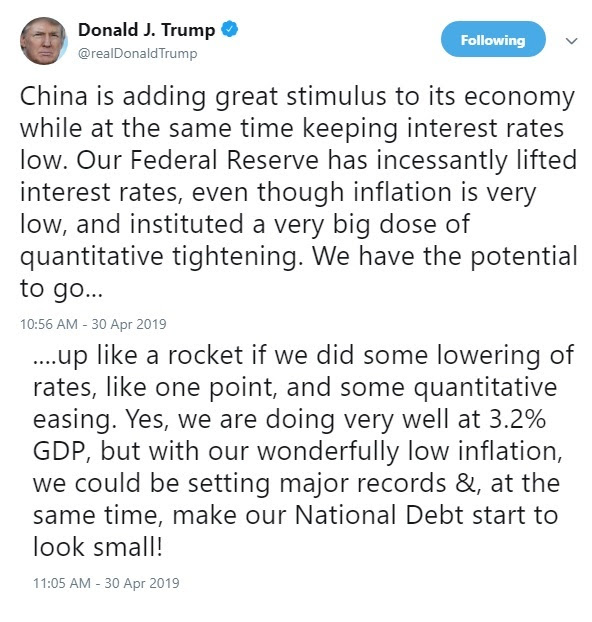

December 14, 5:00 pm EST

We’ve talked about the struggling Chinese economy this week.

As I’ve said, much of the key economic data in China is running at or worse than 2009 levels (the depths of the global economic crisis).

And the data overnight confirmed the trajectory: lower.

As we’ve discussed, this lack of bounce in the Chinese economy (relative to a U.S. economy that is growing at better than 3%) has everything to do with Trump squeezing China.

He acknowledged it today in a tweet ….

The question: Has China retaliated with more than just tit-for-tats on trade? Have they been the hammer on U.S. stocks? It’s one of the few, if not only, ways to squeeze Trump. As we discussed last week, when the futures markets re-opened (at 6pm) on the day of mourning for the former 41st President, there was a clear seller that came in, in a very illiquid period, with an obvious motive to whack the market. It worked. Stocks were down 2% in 2 minutes. The CME (Chicago Mercantile Exhange) had to halt trading in the S&P futures to avert a market crash at six o’clock at night.

Now, cleary stocks have a significant influence on confidence. You can see confidence wane, by the day, as stocks move lower. And, importantly, confidence fuels the decisions to spend, hire and invest. So stock market performance feeds the economy, just as the economy feeds stock market performance. The biggest threat to a fundamentally strong economy, is a persistently unstable stock market. In addition, sustaining 3% growth in the U.S. will be difficult if the rest of the world isn’t participating in prosperity.

With that in mind, in my December 1 note, I said “it may be time for Trump to get a deal done (with China) and solidify the economic momentum needed to get him to a second term, where he may then readdress the more difficult structural issues with China/U.S. relations.” That seems even more reasonable now.

We have two 12% declines in stocks this year. And you can see the fear beginning to set in. With that, the best investors in the world have made their careers by “being greedy when others are fearful” (Warren Buffett) or “buying when most people are selling and selling when most people are buying” (Howard Marks). There is clear value in stocks right now.

December 12, 5:00 pm EST

We talked about the China trade story yesterday.

In a nutshell, Trump has capitalized on an aligned Congress (in the first half of the mid-term) to stoke the U.S. economy. And that has strengthened the leadership position of the U.S. coming out of the decade long post-global economic crisis period.

With that, Trump has used the leverage of global economic leadership (in a vulnerable global economic period) to force change in China. And as we observed yesterday (in the charts of Chinese GDP, industrial production, domestic investment and retail sales), he’s getting movement because the Chinese economy was sputtering before the trade crackdown, and is now running out of gas. Much of the key economic data in China is running at or worse than 2009 levels (the depths of the global economic crisis). We get new data on industrial production, domestic investment and retails sales out of China tonight. This should provide more information on how the Chinese economy is being squeezed.

As for stocks, we have eleven trading days remaining for the year. The S&P 500 finishes today down about 1% for the year, and down 3.4% month-to-date. On the quarter, stocks are down 9% — the worst fourth quarter since 2008. If we look back at monthly returns, dating back to 1950, stocks have finished UP in December 75% of the time, for an average gain of 1.5%. Only two times have stocks has worse December performance over the near 70 year period (2002 and 1957).

And remember, as we discussed earlier this week, it’s not just stocks. It’s a zero (or near zero) return year for all major asset classes this year. Stocks, bonds, gold, real estate … nothing is working. The winner on the year has been cash.

|

October 8, 5:00 pm EST China was on holiday last week (Golden Week). So today, with China back to work, we saw the response in Chinese markets, for the first time, to the spike in global bond yields (and the slide in global stocks). Chinese stocks fell by 3.7%. The yuan slid back to the 21-month lows. And the PBOC stepped in with the fourth cut of the year to its reserve ratio. Now, China has been running sub-7% growth since late 2015. And in China, that’s recession like economic activity. The Chinese government’s sensitivity to this level of growth is clear through the behavior of the central bank’s use of RRR cuts and the currency (the yuan). Cutting the required reserves for banks is a way to stimulate the economy – to promote lending. Weakening the currency is a way to stimulate exports. You can see in the chart below, that has been the path for both (the currency and the RRR) since late 2015. |

|

| You can also see in the chart, a period where the yuan strengthened sharply. What gives?

That was China’s response to the Trump election. The Chinese ran the currency back UP, in hopes of pacifying Trump and staying above the trade dispute fray. It didn’t work. As we know, they have found themselves at the center of Trump’s trade offensive. As such, they have dug in, and returned to weakening the yuan — the best way they know, to defend/drive growth in their economy (i.e. undercut the world on price). The USD/CNY rate here will probably become the most important market to watch in the coming days and weeks. A return to 7 yuan per dollar would be the weakest level of the Chinese currency since 2008, pre-Lehman. That will cause some geopolitical fireworks. Attention loyal readers: The Billionaire’s Portfolio is my premium advisory service. And I’d like to invite you to join today, as we are beginning what I think will be a tremendous run for value stocks into the end of the year. It’s a great deal for the money. Just click here to subscribe, and get immediate access to my full portfolio of billionaire-owned stocks. When you join, you’ll get immediate access to every recommendation–past, present and future–in the portfolio. And I’ll deliver my in-depth notes on our portfolio and the bigger picture every week, directly to your inbox.

|