This past week we’ve talked about the recent public disclosures made about the investments of some of the world’s best investors.

The biggest news was Warren Buffett’s new $1 billion plus stake in Apple.

Apple’s stock price peaked in April of last year (following a 65% rolling 12-month return). Much of that run up was driven by activist efforts of Carl Icahn. Icahn influenced sentiment in the stock, but also influenced value creation for shareholders by pressuring Apple management to buy back stock.

But since peaking last April (2015), Apple shares had lost nearly 34% as of earlier this month. Icahn dumped his stake and made it public in late April.

And then we find this past week that Buffett is now long (he’s in).

So should you follow Buffett? Is it the bottom for Apple? And what makes Apple a classic Buffett stock?

First, Buffett has compounded money at 19.2% annualized over a 50 year period. That’s made him the second wealthiest man in the world.

Buffett loves to buy low. He has a long and successful record of buying when everyone else is selling. Buffett purchased his Apple stake last quarter when Apple was near its 52-week low.

But he famously stays away from technology. Why Apple? For Buffett, Apple is a global, dominant brand. That trumps sector. He loves brand name companies with a loyal customer base, and there is probably no company on the planet with a more loyal customer base then Apple. Plus, one could argue that Apple is a consumer services company (with 700 million credit cards on file, charging customers for movies, songs, apps …).

Generally Buffett pays less than 12 times earnings for a company. Of course there are exceptions, but Apple fits this criterion perfectly with a P/E of 10.

Buffett loves companies that have a high return-on-invested-capital (ROIC) and low debt. Apple has an ROIC of 28%, extremely high. Companies with a high ROIC usually have a “wide moat” or a competitive advantage over the rest of the world. That gives them pricing power to drive wide margins.

Apple really is the classic Buffett stock. And now that Buffett has put his stamp of approval on Apple, we believe the stock has bottomed, especially since it’s so cheap compared to the overall stock market. And he’s not the only billionaire value investor who loves Apple. Billionaire hedge fund manager David Einhorn also loves Apple. He increased his Apple stake last quarter to 15% of his entire hedge fund, almost $900 million dollars worth.

Don’t Miss Out On This Stock

In our Billionaire’s Portfolio we followed the number one performing hedge fund on the planet into a stock that has the potential to triple by the end of the month.

This fund returned an incredible 52% last year, while the S&P 500 was flat. And since 1999, they’ve done 40% a year. And they’ve done it without one losing year. For perspective, that takes every $100,000 to $30 million.

We want you on board. To find out the name of this hedge fund, the stock we followed them into, and the catalyst that could cause the stock to triple by the end of the month, click here and join us in our Billionaire’s Portfolio.

We make investing easy. We follow the guys with the power and the influence to control their own destiny – and a record of unmatchable success. And you come along for the ride.

As we’ve discussed over the past few months, markets can be wrong—sometimes very wrong.

On that note, consider that the yield on the U.S. ten–year Treasury was trading closer to 2.30% after the Fed’s first rate hike last December—the first hike in nearly ten years and the symbolic move away from the emergency zero interest rate policy. The ten–year yield has, incredulously, traded as low as 1.53% since. One end of that spectrum is wrong, very wrong.

Remember, as we headed into the last Fed meeting, the ten–year yield was trading just shy of 2% (after a wild ride down from the December hike date). And the communication to that point from the Fed was to expect FOUR rate hikes in 2016.

Of course, in the face of another global economic crisis threat, which was driven by the oil price bust, the Fed did their part and backed off of that forecast—taking two of those hikes off of the table. Still, yields under 2% with even two hikes projected seemed mispriced.

So following a dramatic 85% bounce in oil prices and the threat of cheap oil now behind us (seemingly), as of yesterday afternoon yields still stood around just 1.79%. That’s more than a 1/2 percentage point lower than the levels immediately following the December hike. And that’s AFTER two voting Fed members just said on Tuesday that they should go two or threetimes this year. So with global risks abating, the Fed is beginning to walk back up expectations for Fed hikes.

Confirming that, as of yesterday afternoon, the minutes from the most recent Fed meeting have been disclosed, which now indicate that a June hike is likely assuming things continue along the current path (i.e. no global shock risks emerge).

Still, the yield on the ten–year Treasury is just 1.84%, 5 basis points higher than it was yesterday morning, prior to the Fed minutes.

Why?

The bet is that the Fed is making a mistake raising rates (at all). But at these levels for the ten–year yield, it’s a very asymmetric bet. The downside for yields here is very limited (short of a global apocalypse), the upside is very big. That makes betting on lower yields a very dangerous one, if not a dumb one. When people are positioned the wrong way in asymmetric trades, the adverse moves tend to be violent. I wouldn’t be surprised to see 2.50% on the U.S. ten–year Treasury by the year end.

Don’t Miss Out On This Stock

In our Billionaire’s Portfolio we followed the number one performing hedge fund on the planet into a stock that has the potential to triple by the end of the month.

This fund returned an incredible 52% last year, while the S&P 500 was flat. And since 1999, they’ve done 40% a year. And they’ve done it without one losing year. For perspective, that takes every $100,000 to $30 million.

We want you on board. To find out the name of this hedge fund, the stock we followed them into, and the catalyst that could cause the stock to triple by the end of the month, click here and join us in our Billionaires Portfolio.

We make investing easy. We follow the guys with the power and the influence to control their own destiny – and a record of unmatchable success. And you come along for the ride.

In our Billionaire’s Portfolio we followed the number one performing hedge fund on the planet into a stock that has the potential to triple by the end of the month.

This fund returned an incredible 52% last year, while the S&P 500 was flat. And since 1999, they’ve done 40% a year. And they’ve done it without one losing year. For perspective, that takes every $100,000 to $30 million.

We want you on board. To find out the name of this hedge fund, the stock we followed them into, and the catalyst that could cause the stock to triple by the end of the month, click here and join us in our Billionaires Portfolio.

We make investing easy. We follow the guys with the power and the influence to control their own destiny – and a record of unmatchable success. And you come along for the ride.

We’ve talked a lot about oil, the rebound of which has probably led to the trade of the year. If you recall back on February 8th, we said policymakers finally got the wake up call on the systemic threat of the oil price bust when Chesapeake Energy, the second largest oil and gas producer, was rumored to be pursuing bankruptcy.

This is what we said:

“The early signal for the 2007-2008 financial crisis was the bankruptcy of New Century Financial, the second largest subprime mortgage originator. Just a few months prior the company was valued at around $2 billion.

On an eerily similar note, a news report hit this morning that Chesapeake Energy, the second largest producer of natural gas and the 12th largest producer of oil and natural gas liquids in the U.S., had hired counsel to advise the company on restructuring its debt (i.e. bankruptcy). The company denied that they had any plans to pursue bankruptcy and said they continue to aggressively seek to maximize the value for all shareholders. However, the market is now pricing bankruptcy risk over the next five years at 50% (the CDS market).

Still, while the systemic threat looks similar, the environment is very different than it was in 2008. Central banks are already all-in. We know, and they know, where they stand (all-in and willing to do whatever it takes). With QE well underway in Japan and Europe, they have the tools in place to put a floor under oil prices.

In recent weeks, both the heads of the BOJ and the ECB have said, unprompted, that there is “no limit” to what they can buy as part of their asset purchase program. Let’s hope they find buying up dirt-cheap oil and commodities, to neutralize OPEC, an easier solution than trying to respond to a “part two” of the global financial crisis.”

Chesapeake bounced aggressively, nearly 50% in 10 business days.

And on February 22nd, we said, “persistently cheap oil (at these prices) has become the new “too big to fail.” It’s hard to imagine central banks will sit back and watch an OPEC rigged price war put the global economy back into an ugly downward spiral. And time is the worst enemy to those vulnerable first dominos (the energy industry and weak oil producing countries).”

As we’ve discussed, central banks did indeed respond. The BOJ intervened in the currency markets on February 11, and that (not so) coincidently put the bottom in oil and global stocks. China followed on February 29, with a cut on bank reserve requirements, then ECB cut rates and ramped up their QE and the Fed joined the effort by taking two projected rate cuts off of the table (we would argue maybe the most aggressive response in the concerted central bank effort).

From the bottom on February 8th, Chesapeake shares have gone up five-fold, from $1.50 to over $7. Oil bottomed February 11 and is up 77%. This is the trade of the year that everyone should have loved. If you’re wrong, the world gets very ugly and you and everyone have much bigger things to worry about that a bet on oil and/or Chesapeake. If you’re right, and central banks step in to divert another big disaster (a disaster that could kill the patient) you make many multiples of your risk.

We think it was the trade of the year. The trade of the decade, we think is buying Japanese stocks.

Overnight the BOJ made no changes to policy. And the dollar-denominated Nikkei fell over 1,200 points (more than 7%).

As we said yesterday, two explicit tools in the Bank of Japan’s tool box are: 1) a weaker yen, and 2) higher stocks. I say “explicit” because they routinely have said in their minutes that they expect both to contribute heavily to their efforts. So now Japanese stocks and the yen have returned near the levels we saw before the Bank of Japan surprised the world with a second dose of QE back in October of 2014. So their efforts have been undone. And they’ve barely moved the needle on their objective of 2% inflation during the period. In fact, the head of the BOJ, Kuroda, has recently said they are still only “halfway there” on reaching their goals.

So they have a lot of work left. And if we take them at their word, a weak yen and higher stocks will play a big role in that work. That makes today’s knee-jerk retreat in yen-hedged Japanese stocks a gift to buy.

U.S. stocks have well surpassed pre-crisis, record highs. German stocks have well surpassed pre-crisis, record highs. Japanese stocks have a long way to go. In fact, they are less than “halfway there.”

Join us here to get all of our in-depth analysis on the bigger picture, and our carefully curated stock portfolio of the best stocks that are owned by the world’s best investors.

Heading into today’s inflation data, the prospects of German 10-year government interest rates going negative had added to the heightened risk aversion in global markets. And we’ve been talking this week about how markets are set up for a positive surprise on the inflation front, which could further support the mending of global confidence.

On cue, the euro zone inflation data this morning (the most important data point on inflation in the world right now) came in better than expected. We know Europe, like Japan, is throwing the kitchen sink of extraordinary monetary policies at the economy in an effort to reverse economic stagnation and another steep fall into deflation. And we know that the path forward in Europe, at this stage, will directly affect that path forward in the U.S. and global economy. So, as we said in one of our notes last week, the world needs to see “green shoots” in Europe.

With the better euro zone inflation data today, we may be seeing the early signs of a bottom in this cycle of global pessimism and uncertainty. German yields are now trading double the levels of Monday. And with that, U.S. yields have broken the downtrend of the month, as you can see in the chart below.

Source: Billionaire’s Portfolio, Reuters

With that in mind, today we want to talk about how we can increase certainty in an uncertain world. Aside from the all-important macro influences, even when you get the macro right, when your investing in stocks, you also have to get a lot of other things right, to avoid the landmines and extract something more than what the broad tide of the stock market gives you (which is about 8% annualized over the long term, and it comes with big drawdowns and a very bumpy road).

In our Billionaire’s Portfolio, we like to put the odds on our side as much as possible. We do so by following big, influential investors into stocks where they’ve already taken a huge stake in a company, and are wielding their influence and power to maximize the probability that they will exit with a nice profit.

This is the perfect time to join us in our Billionaire’s Portfolio. We’ve discussed our simple analysis on why broader stocks can and should go much higher from here. You can revisit some of that analysis here. In our current portfolio, we have stocks that are up. We have stocks that are down. We have stocks that are relatively flat. But they all have the potential to do multiples of what the broad market does. And for depressed billionaire-owned stocks, a broad market rally and shift in economic sentiment should make these stocks perform like leveraged call options – importantly, without the time decay. Join us hereto get your portfolio in line with ours.

We talked this week about the way markets are set up for a significant positive perception shift. It’s been led by oil, which had its third consecutive close above $40 today. Yields are another key brick in the foundation that may be laid tomorrow.

As oil prices have been a threat to the global economic and stability outlook over the past few months, yields have also been sending a negative signal to markets. The yield on the German 10-year got very close to the all-time lows this week, inching closer to the zero line (and negative territory). And U.S. 10-year yields, following the Fed’s last meeting, have fallen back from 2% down to as low as 1.68% — just 30 basis points above the all-time low of July 2012, when Europe was on the edge of a sovereign debt blow-up. And remember, this is AFTER the Fed has raised rates for the first time in nine years.

So yields have been signaling an uglier path forward, if not deflation forever in places like Japan and Europe. Of course, the move by Japan to negative interest rates in January was a strong contributor to the perception swoon about the global economy. But a key component in Japan’s move, and in the coordinated actions by central banks over the past two months, has been the threat from the oil price bust. And that is now on the mend. Oil is up 58% from its February low.

Still, global yields are hanging around at the lows.

Tomorrow we get euro zone and U.S. inflation data. As we’ve said, when expectations and perception has been ratcheted down so dramatically, we can get an asymmetric outcome. Earnings expectations are in the gutter. Economic growth expectations are in the gutter. Same can be said for expectations on the outlook for inflation data. In a normal world, hotter than expected inflation is a bad signal for the risk-taking environment. In our current world, hotter than expected inflation would not be a good signal, it would be a very good signal. It would show the economy has a pulse.

Yields in the two key government bond markets are set up nicely for a bottom on some hotter inflation data.

Tuesday, German yields touched 7.5 basis points. Remember, earlier in the month we talked about what happened the last time German yields were this low.

Bond kings Bill Gross and Jeffrey Gundlach said it was crazy. Bill Gross called the German bund the “short of a lifetime” (short bonds, which equates to a bet that yields go higher). He compared it to the opportunity when George Soros broke the Bank of England and made billions shorting the British pound. Gundlach said it was a trade with almost no upside and unlimited downside.

They were both right. In the chart below you can see the explosive move in German rates (in blue) away from the zero line. In the chart below, you can see the 10-year German bond yields moved from 5 basis points to 106 basis points in less than two months — a 20x move. U.S. 10 year yields (the purple line) moved from 1.72% to 2.49% almost in lock-step.

On the move down on Tuesday, the yield on the German bund reversed sharply and put in a bullish outside day (a key reversal signal). Could it have been the bottom into tomorrow’s inflation data?

Coincidentally, the U.S. 10-year looks like a bottom may be in as well.

U.S. yields have a chance to break this downtrend tomorrow on a hotter inflation number.

As we said yesterday, in addition to oil, these are very important charts for financial markets and for the global economic outlook. A bottom in these yields, as well as the continued recovery in oil will be important for restoring confidence in the global economic outlook.

This is the perfect time to join us in our Billionaire’s Portfolio. We have just added the billionaire’s macro trade of the year to our Billionaire’s Portfolio — a portfolio of deep value stocks owned by the best billionaire investors in the world. You can join us here.

As we said yesterday, oil on the mend is the key proxy right now for global economic stability. With that, after closing above $40 yesterday, oil continued its surge today, up 4%. And global stocks had a good day, up 1% in the U.S.

Remember, we get key inflation data over the next couple of days, namely from Europe and the U.S. A hotter inflation number in the U.S. would further support the signal that oil is giving to markets (a positive one).

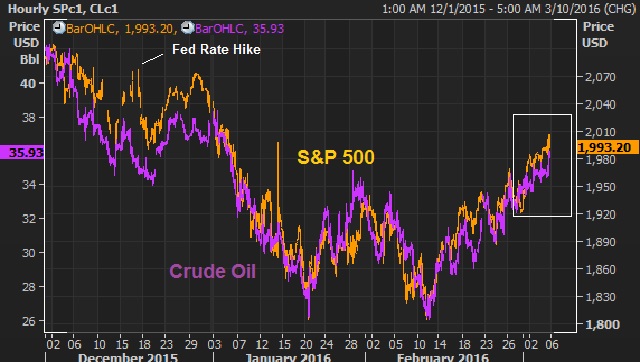

Today we want to look at a few of very key charts. This first chart is an update on the crude oil/stock market relationship. We’ve looked at this a few times over the past few months. The last time we revisited this chart, oil and stocks had started to diverge from stocks with its recent move back into the mid 30s.

So oil is sustaining above $40 for the first time since November. We know three of the top oil traders in the world are betting on $70-$80 oil by next year. We know central banks have stepped in (in coordination) since the low in oil on February 11 and the result has been a 50%+ bounce in oil. Now, technically, oil looks like a technical breakout is here.

In the above chart, you can see oil breaking above the high of March 22 (which was 41.90). In fact, we get a close above that level – technically bullish. And we also now have a technically bullish pattern (an impulsive C-wave of an Elliott Wave structure) that projects a move to $51.50, which happens to be right about where this big trendline comes in.

Now, with the inflation data in the pipeline for the week, we’ve talked about the negative signal that ultra-weak yields are sending to markets. And German yields have been leading the way on that front. But guess what? German yields reversed sharply off of the lows yesterday, and continued higher today, putting in a long term bullish reversal signal (an outside day – technical jargon, but can be very predictive of tops and bottoms). And that coincides with the U.S. 10-year yield, which is on the verge of breaking the recent downtrend and projecting a move back to 2.15%. We’ll take a look at these very important charts for financial markets and for the global economic outlook tomorrow.

These key markets are signaling what could be the beginning of a big shift in sentiment and the beginning of positive surprises in markets and economies, which tends to happen when expectations have been ratcheted down so dramatically, as we discussed yesterday with the sour earnings outlook and pessimistic economic backdrop.

This is the perfect time to join us in our Billionaire’s Portfolio. We have just added the billionaire’s macro trade of the year to our Billionaire’s Portfolio — a portfolio of deep value stocks owned by the best billionaire investors in the world. You can join us here.

Central bank posturing has put a bottom in oil and stocks in the past month. Rising stocks and oil, in this environment, have a way of restoring sentiment and the stability of global financial markets. Those efforts were underpinned by more aggressive stimulus from the European Central Bank last week.

And the Fed furthered that effort today.

Just three months ago, the Fed projected that they would hike rates an additional full percentage point this year. Today they backed off and cut that projection down to just 1/2 percent (50 basis points) by year end.

That’s a big shift. In the convoluted post-QE, post-ZIRP world, that’s almost like easing.

What’s happened in the interim? Janet Yellen was asked that today and said it was: Slowing growth in China … A negative fourth quarter GDP number in Japan … Europe has had weaker growth … and Emerging markets have been weighed down by declines in oil prices.

Aside from the negative GDP print in Japan, none of these were new developments (even Japan was no shocker). Meanwhile, during the period from the Fed’s December meeting to its meeting today, oil did a round trip from $37 to $26 and back to $37.

So what happened? It appears that the Fed completely underestimated the threat of weak oil prices to the global economy and financial system. We’ve talked extensively about the danger of persistently weak oil prices, which, at sub $30 was pushing the world very close to the edge of disaster. That threat became very clear in late January/early February, culminating when the one of the biggest oil and natural gas companies in the world, Chesapeake, was rumored to be pursuing the path of bankruptcy (which was of course denied by the company). It was that moment, it appears, that policymakers woke up to the risk that the oil bust could lead to another global financial crisis — with a cascade of defaults in the energy sector, leading to defaults in weak oil exporting countries, spilling over to banks and another financial crisis.

Today’s move by the Fed, while confusing at best, led to higher stocks and higher oil prices. The market has been pricing in a much more accommodative path for the Fed for the better part of the past three months, and today the Fed dialed down to those expectations (i.e. they have now followed the ECB’s bold easing with some easier policy/guidance of their own), which should provide more fuel for the stabilization of financial markets and recovery of key markets (i.e. the continued bottoming of key industrial commodities, more stable and rising stocks and aggressive recovery in oil).

Were they just that wrong, or are they doing their part in coordinating stimulus from last month’s G20 meeting?

Bryan Rich is a macro trader and co-founder of Billionaire’s Portfolio. If you’re looking for great ideas that have been vetted and bought by the world’s most influential and richest investors, join us at Billionaire’s Portfolio.

Intervention has been the common theme we’ve discussed for the better part of the past two months. And this week, that theme is heating up.

We’ve explained why oil at $30 has posed a threat to the global financial system and global economy. And we explained the parallels of the systemically threatening (current) oil price bust and the 2007-2008 housing bust. But we also noted the key differences, and why and how this “cheap oil” problem could be easily solved, unlike the housing bust.

Heading into today’s inflation data, the prospects of German 10-year government interest rates going negative had added to the heightened risk aversion in global markets. And we’ve been talking this week about how markets are set up for a positive surprise on the inflation front, which could further support the mending of global confidence.

Heading into today’s inflation data, the prospects of German 10-year government interest rates going negative had added to the heightened risk aversion in global markets. And we’ve been talking this week about how markets are set up for a positive surprise on the inflation front, which could further support the mending of global confidence.

{kind=link}