With a Fed decision queued up for tomorrow, let’s take a look at how the rates picture has evolved this year.

The Fed has continued to act like speculators, placing bets on the prospects of fiscal stimulus and hotter growth. And they’ve proven not to be very good.

Remember, they finally kicked off their rate “normalization” plan in December of 2015. With things relatively stable globally, the slow U.S. recovery still on path, and with U.S. stocks near the record highs, they pulled the trigger on a 25 basis point hike in late 2015. And they projected at that time to hike another four times over the coming year (2016).

Stocks proceeded to slide by 13% over the next month. Market interest rates (the 10 year yield) went down, not up, following the hike — and not by a little, but by a lot. The 10 year yield fell from 2.33% to 1.53% over the next two months. And by April, the Fed walked back on their big promises for a tightening campaign. And the messaging began turning dark. The Fed went from talking about four hikes in a year, to talking about the prospects of going to negative interest rates.

That was until the U.S. elections. Suddenly, the outlook for the global economy changed, with the idea that big fiscal stimulus could be coming. So without any data justification for changing gears (for an institution that constantly beats the drum of “data dependence”), the Fed went right back to its hawkish mantra/ tightening game plan.

With that, they hit the reset button in December, and went back to the old game plan. They hiked in December. They told us more were coming this year. And, so far, they’ve hiked in March and June.

Below is how the interest rate market has responded. Rates have gone lower after each hike. Just in the past couple of days have, however, we returned to levels (and slightly above) where we stood going into the June hike.

But if you believe in the growing prospects of policy execution, which we’ve been discussing, you have to think this behavior in market rates (going lower) are coming to an end (i.e. higher rates).

As I said, the Hurricanes represented a crisis that May Be The Turning Point For Trump. This was an opportunity for the President to show leadership in a time people were looking for leadership. And it was a chance for the public perception to begin to shift. And it did. The bottom was marked in Trump pessimism. And much needed policy execution has been kickstarted by the need for Congress to come together to get the debt ceiling raised and hurricane aid approved. And I suspect that Trump’s address to the U.N. today will add further support to this building momentum of sentiment turnaround for the administration. With this, I would expect to hear a hawkish Fed tomorrow.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

As for oil: From the depths of the oil price crash last year, remember, we discussed the prospects for a huge bounce. Oil prices at $26 were threatening to undo the trillions of dollars of work central banks and governments had done to stabilize the global economy. Central banks couldn’t let it happen. After a series of coordinated responses (from the BOJ, China, ECB and the Fed), oil bottomed and quickly doubled.

Also at that time, two of the best oil traders in the world were calling the bottom and calling for $70-$80 oil by this year (Pierre Andurand and Andy Hall). Another commodities king that called the bottom: Leigh Goehring.

Goehring, one of the best commodities investors on the planet, has also laid out the case for $100 oil by next year. He says he’s “wildly bullish” oil in his recent quarterly investor letter at his new fund, Goehring & Rozencwajg.

Goehring argues that the IEA inventory numbers are flawed. He thinks oil the market is already over-supplied and is in a draw, as of May of last year. With that, he thinks the OPEC cuts will ultimately exacerbate the deficit and send prices aggressively higher. He says “we remain ‘wildly’ bullish and believe that there is a very high probability of oil prices reaching triple digits in the first half of 2018.”

Follow This Billionaire To A 172% WinnerIn our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

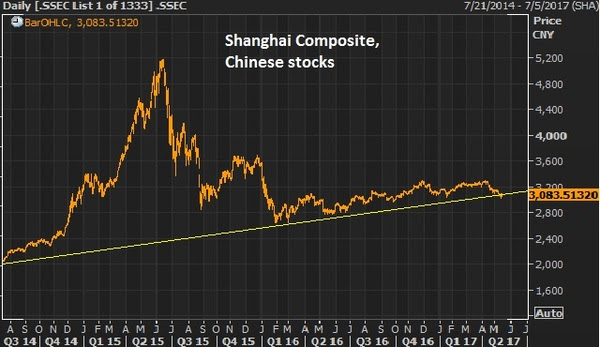

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

Let’s take at the chart…

While the agreements out of China were said not to touch on steel and industrial metals, the first steps of cooperation could put a bottom in the slide in metals like copper and iron ore. These are two commodities that should be direct beneficiaries in a world with better growth prospects, especially with prospects of a $1 trillion infrastructure spend in the U.S. With that, they had a nice run up following the election but have backed off in the past couple of months, as the infrastructure spend appeared not to be coming anytime soon.

Here’s copper and the S&P 500…

Trump policies are bullish for both. Same said for iron ore…

This is right in the wheelhouse of Wilbur Ross, Trump’s Secretary of Commerce. He’s made it clear that he will fight China’s dumping of steel on the U.S. markets, which has driven steel prices down and threatened the livelihood of U.S. steel producers. Keep an eye on these metals next week, and the stocks of producers.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

We had new record highs again in the Dow today. But remember, yesterday we talked about this dynamic where stocks, commodities and the dollar were strong. But a missing piece in the growing optimism about growth has been yields.

Clearly the 10 year at 2.40ish is far different than the pre-election levels of 1.75%-1.80%. But the extension was quick and has since been a non-participant in the full-on optimism vote given across other key markets.

Why? While stocks can get ahead of better growth, yields can’t in this environment. Higher stocks can actually feed higher growth. Higher yields, on the other hand, can kill it.

But there’s something else at work here. As we know Japan’s policy to target the their 10 year at zero provides an anchor to our interest rates, as the BOJ is in unlimited QE mode. Some of that freshly produced liquidity, and the money displaced by their bond buying, undoubtedly finds a happier home in U.S. Treasuries (with a rising dollar, and a 2.4% yield). That caps yields.

But in large part, the quiet drag on U.S. yields has also come from the rising risks in Europe. The election cycle in Europe continues to threaten a populist Trump-like movement, which is very negative for the European Union and for the survival of the single currency (the euro). That creates capital flight, which has been contributing to dollar strength and flows into the parking place of U.S. Treasuries (which pressures yields, which is keeping mortgage and other consumer rates in check).

These flows are also showing up clearly in the safest bond market in Europe: the German bunds. The 2-year German bund hit an all-time record LOW, today of -91 basis points. Yes, while the U.S. mindset is adjusting for the idea of a 3%-4% growth era, German yields are reflecting crisis and money is plowing into the safest parking place in Europe. The spread between German and French bonds are reflecting the mid-2012 levels when Italy and Spain where on the brink of insolvency — only to be saved by a bold threat/backstop from the European Central Bank.

We talked last week about the prospects for higher gold and lower yields as questions arise about the execution of (or speed of execution) Trump’s growth policies, some of the inflation optimism that has been priced in, may begin to soften. That would also lead to a breather for the stock market. I suspect we will begin to see the coming elections in Europe also contribute to some de-risking for the next couple of months. We already have a good earnings season and some solid economic data and optimism about the policy path priced in. May be time for a dip. But as I’ve said, it would create opportunities– to buy any dip in stocks, and sell any rally in bonds.

To peek inside the portfolio of Trump’s key advisor, join me in our Billionaire’s Portfolio. When you do, I’ll send you my special report with all of the details on Icahn, and where he’s investing his multibillion-dollar fortune to take advantage of Trump policies. Click here to join now.

Stocks continue to print new record highs. Let’s talk about why.

First, as we know, the most powerful underlying force for stocks right now is prospects of a massive corporate tax cut, deregulation, a huge infrastructure spend and trillions of dollars of corporate repatriation coming. But quietly, among all of the Trump attention, earnings are also driving stocks. More than 70% of S&P 500 companies have reported. About 2/3rds of the companies have beat Wall Street estimates. And most importantly, earnings in Q4 have grown at 3.1% year-over-year. That’s the first consecutive positive growth reading since Q4 2014/ Q1 2015.

Meanwhile, yields have remained quiet. And oil prices have remained quiet. That’s positive for stocks. Take a look at the graphic below …

You can see, stocks and most commodities continue to rise on the growth outlook. Yields and energy should be rising too. But the 10 year yield has barely budged all year — same for oil. Of course, higher rates, too fast, are a countervailing force to the pro-growth policies. Same can be said for higher oil too fast. With that, both are adding more “fuel” to stocks.

On the rate front, we’ll hear from Janet Yellen this week, as she gives prepared remarks on the economy to Congress, and takes questions.

She’s been a communications disaster for the Fed. Most recently, following the Fed’s December rate hike, she backtracked on her comments made a few months prior, when she said the Fed would let the economy run hot. She denied that in December. Still, the 10-year yield is about 10 basis points lower than where it closed following that December press conference. I wouldn’t be surprised to see a more dovish tone from Yellen this time around, in effort to walk market rates a little lower, to take the pressure off of the Fed and to continue stimulating optimism about the economy.

On Friday we looked at four important charts for markets as we head into this week: the dollar/yen exchange rate, the Nikkei (Japanese stocks), the DAX (German Stocks), and the Shanghai Composite (Chinese stocks).

With U.S. stocks printing new record highs by the day, these three stock markets are ready to make a big catch-up run. It’s just a matter of when. And I argued that a positive tone coming from the meeting of U.S. and Japanese leadership, under the scrutiny of trade tensions, could be the greenlight to get these markets going. That includes a stronger dollar vs. the yen. All are moving in the right direction today.

On the China front, we looked at this chart on Friday.

As I said, “Copper has made a run (up 10% ytd). That typically correlates well with expectations of global growth. Global growth is typically good for China. Of course, they are in the crosshairs of Trump’s fair trade movement, but if you think there’s a chance that more fair trade terms can be a win for the U.S. and a win for China, then Chinese stocks are a bargain here.”

Copper is surged again today on a supply disruption and has technically broken out.

This should continue to spark a move in the Chinese stock market.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

I talked yesterday about the Fed. As I said, I think we’ll find that the Fed will shift gears again to stay behind the curve on inflation, to let the economy run a little hot. They met today and it was a non-event. They said nothing to build momentum on their rate hike from December.

The news of the day has been Apple (NASDAQ:AAPL) earnings. People over the past couple of years have been calling for the decline in Apple. They’ve said it’s topped. They can’t innovate in the post-Steve Jobs era. The iPhone was magic. But reproducing magic isn’t easy. Once you put a computer in everyone’s pocket, there’s not much more they can do to it with it. These are all of the quips about Apple’s peak. They may be right. But Apple’s peak, at least as a stock, is greatly exaggerated.

They reported a huge positive surprise on earnings yesterday after the close. The stock was up 6% on the day. But even before that, I suspect it has become a much loved stock in the past two months in the “smart money” investor community.

We should see in the coming weeks, as big investors disclose their positioning for the end of Q4, Apple will have returned to a lot of portfolios again. Warren Buffett, an investor that has made his fortune buying when others are selling, built a big stake at the lows of the year last year. And it’s a perfect Buffett stock.

It’s incredibly cheap compared to the market.

The stock still trades at 15x earnings. Much cheaper than the market. Apple trades at 13x next year’s projected earnings. The S&P 500 trades at 16.5x. What about Apple’s monster cash position? Apple has even more cash now — a record $246 billion. If we excluded the cash from the valuation, Apple market cap goes down from $675 billion to $429 billion. That would equate to Apple trading at closer to 9x earnings. Though not an “apples to apples” that valuation would group Apple with the likes of these S&P 500 components that trade around 9 times earnings, like: Dow Chemical, Prudential Financial, Bed Bath & Beyond, a Norwegian chemical company (LBY), and Hewlett Packard Enterprise. It’s safe to say no one is debating whether or not Hewlett Packard is at the pinnacle of its business. Yet, if we strip out the cash in Apple, AAPL shares are trading closer to an HPE valuation.

Add to that, Apple now has a fresh catalyst coming in, Trump policies. The new President Trump is incentivizing Apple (and others) to bring offshore cash hoards back home with a flat 10% tax. And Apple makes money – a lot of it. A cut in the corporate tax rate will be a boon for earnings. Two years ago, Carl Icahn argued that Apple should use (a lot more of) their cash to buyback shares – and, with that, valued the stock at double its current levels.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The Trump agenda continues to dominate the market focus as we entered the second week of Trumponomics.

To this point the market focus has been on the pro-growth agenda. With that, stocks have been higher, yields have been higher, the dollar has been higher, and global commodities have been broadly rising. Meanwhile, gold (the fear trade) has been falling and the VIX has been falling, toward ultra-low levels. The VIX, like gold, is a good market indicator of uncertainty and/or fear.

Let’s talk about the VIX…

The VIX measures the implied volatility of options on the S&P 500. This is a key component in the price investors pay for downside protection on their portfolios.

So what is implied volatility? Implied volatility measures both actual volatility and the options market maker community’s expectations (or perception of certainty) about future volatility. When market makers feel confident about the stability in markets, implied vol is lower, which makes the price of options cheaper. When they aren’t confident in stability, implied vol goes up, which makes the price of an option go up. To compensate those that are taking the other side of your trade, for the lack of predictability, you pay a premium.

With that in mind, on Friday, the VIX traded to the lowest levels since the days before the failure of Lehman Brothers. That indicates that the market had (or has) become a believer that pro-growth policies, combined with ultra-easy central bank policies have created a buffer against the downside in stocks. But that perception of downside risk is changing today, with the more vocal uprising against Trump social policies. You can see the spike (in the far right of the chart) today…

So as big money managers were closing the week last Friday, looking at Dow 20,000+ and a VIX sliding toward levels not too far from pre-crisis levels, buying downside protection was dirt cheap. This morning, they’re paying quite a bit more for that protection.

With that said, this pop in the VIX and the Dow trading off by more than 100 points today gets a lot of attention. But is there justification to think that market turbulence will begin to reflect the turbulence and division in public opinion toward Trump policies? Just gauging the extent of the market reaction from the VIX today, it’s unlikely. The chart below is the longer term view of the VIX.

My observations: The VIX has had a small bounce from very, very low levels. On an absolute basis, vol is still very cheap. When there is real fear in the air, real uncertainty about the future, you can see from the spikes in the longer term chart above, the premium for the unknown gets priced in quickly and aggressively. Given that there has been virtually no risk premium priced into the market for any falter in the Trump Presidency, or the execution of Trump policies, the moves today have been very modest. And gold (as I write) is barely changed on the day.

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We’re finishing the first full week under Trumponomics. And it’s been an active one.

It’s clear now that President Trump intends to follow through on his campaign promises. While that’s making waves with the media and with Washington types, it’s creating more certainty about the outlook for growth for the real economy and, therefore, for financial markets.

We close the week with the Dow above 20,000, on new record highs. And as we discussed yesterday, stock markets around the world are rallying too on the prospects of a stronger U.S. economy translating into a stronger global economy. We looked at the charts of Mexican and Canadian stocks yesterday–both of which are sitting on record highs. U.K. stocks are near record highs and German stocks are quickly closing in.

We already know that small business optimism in the U.S. has hit 12-year highs, jumping by the most in since 1980–on Trump’s pro-growth agenda. Today the consumer sentiment report showed sentiment is on the rise too–at 13-year highs.

Let’s talk about the data that we’re leaving behind. Fourth quarter GDP was reported today at just 1.9%. This, more than seven years removed from the failure of Lehman Brothers, an $800 billion stimulus package, seven years of zero interest rates and three rounds of quantitative easing, and the economy is running at about 60% of its normal pace. And even after taking the Fed’s balance sheet from $800 billion to $4.5 trillion, we have inflation running at less than 50% of its normal pace. This malaise is consistent throughout the world. And this is precisely why big, bold fiscal stimulus and structural change is desperately needed, and is being embraced by those that understand the dangers of the stall-speed global economy that has been kept alive by global central bank intervention. As I’ve said, at Dow 20,000, it’s just getting started.

Have a great weekend!

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Remember, this (animal spirits) is the element that economists and analysts can’t predict, and can’t quantify. It’s not in the forecasts. This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mistrust of the system. All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindsethas been underway since the night of the election. And that gives way to a return of animal spirits.

Higher stock prices tend to beget higher stock prices. Trust me, individual investors that haven’t been believers will be calling their financial advisors and logging in to their online brokerage accounts over the coming days. Institutional investors that haven’t been believers, that have been underweight stocks, will be beefing up exposure if they want to compete with their peers (and keep their jobs).

And not only do higher stock prices lead to higher stock prices, but higher stock prices tend to make people feel more confident about the economy, which begets a better economy.

Add to this, the psychological value of Dow 20,000 could finally be a turning point in the divergence of sentiment toward the Trump Presidency. It may serve as a validation marker for those that have been on the fence. And for those in opposition, as I’ve said before, growth solves a lot of problems! When the college grad that’s been relegated to a 10-year career as a barista begins to see signs of opportunity for a better career and a better future, in a stronger economy, the sands of Trump sentiment can shift quickly.

Cleary, Trump entered with a game plan that can pop economic growth. And he’s going 100 miles an hour at executing on that plan. For markets, what he’s doing is creating a sense of certainty for investors. They know what he’s promised, and now they know that he appears to intend on delivering on those promises. And the coordination of growth policies, along with ultra-easy monetary policy (even with tightening in view) serves as risk mitigators for markets. It should limit downside risk, which is what investors care most about. How?

Remember, even at Dow 20,000, stocks are still extremely cheap.

Here’s a review on why …

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 48% by the middle of this year. We’re still making up for the lost growth of the past decade. And there’s a lot of ground to make up.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year. That’s an S&P 500 earnings estimate of $133.64 times a P/E of 20 equals 2,672 on the S&P 500.

Reason #3: The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 37% higher.

With this in mind, we are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The new President Trump has wasted no time on carrying out his plan on trade. He met with 12 major U.S. company leaders today and told them that they would pay to build outside of the U.S., but (importantly) they would save to build here. And he wrote an executive order to withdraw from the Trans-Pacific Partnership, and one to renegotiate NAFTA.

There are plenty of people that have focused on the risks and the dangers with the Trump trade policies. Meanwhile, those most directly affected aren’t quite as draconian on the outlook — quite the opposite. The executives that have walked out of Trump Tower, and now the White House have largely been optimistic. The same is said for trade partners. Whether they mean it or not, they understand the value of doing business with the U.S. consumer.

As I’ve said, there are clear opportunities for win-wins – especially in a world that must rebalance trade to avoid more cycles of the booms and busts, like the boom-bust we experienced over the past two decades. The administration has the leverage of power (with a Republican Congress), but they also have the leverage of rewards. Despite what the media tells us, behind closed doors the new administration seems to negotiate by carrot rather than stick. Trump comes to meetings bearing gifts, and that creates buy-in.

When you bring American CEOs in and tell them that you’re going to give them a 20 percentage point tax cut, you’re going to slash the regulation burden (by “75%” as he said today), you’re going to give them a 30+ percentage point tax cut on repatriating offshore money, and your going to launch a trillion dollar infrastructure spend, all in an effort to juice the economy to a 4%+ growth rate, they’re going to be very excited — even if you tell them they can no longer access the cheapest production in the world.

In the end, they’d rather have a hot economy to sell into, than a stagnant economy, even if it comes with a higher cost of production. And we may find that, in the end, the after-tax profit margins of these big U.S. corporates may be better given all of these incentives, even if they make things here. Better revenues, and maybe better margins to go with it.

Remember, the optimism of U.S. small business owners made the biggest jump since 1980 on the prospects of growth-friendly Trump policies. GDP equals Consumption + Investment + Government Spending + Net Exports. Ultra easy monetary policies have made borrowing cheap, saving expensive and created the economic stability necessary to get hiring over the past several years. That has all kept consumption going.

The “build it here” policies are a recipe for capital investment to finally ramp up. Add to that, a big government infrastructure spend, and we’re getting the pieces of the puzzle in place to see much better economic growth. A hotter U.S. economy will mean a hotter global economy. With that, I suspect net exports will ultimately pick up as well, with a healthier, more sustainable global economy.

On that note, if we look at the USD/Mexican Peso exchange rate as a gauge of trade partner health, we’ve seen the peso hit hard through the campaigning period under the protectionist fears of a Trump administration. Interestingly, since the inauguration, the peso has been strengthening, even as President Trump signed an executive order today to renegotiate NAFTA. The message behind that usually means: the U.S. does better, Mexico does better.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

dell, whirlpool, ford, johnson and johnson, lockheed, arconic, u.s. steel, tesla, under armour, international paper, corning, trump, white house

With a Fed decision queued up for tomorrow, let’s take a look at how the rates picture has evolved this year.

With a Fed decision queued up for tomorrow, let’s take a look at how the rates picture has evolved this year.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

Stocks continue to print new record highs. Let’s talk about why.

Stocks continue to print new record highs. Let’s talk about why.