The Fed moved again today on rates, as the market expected. This is the eighth quarter point hike in this post-QE normalization on rates. And this now puts the Fed Funds rate at the range of 2%-2.25%.

Now, the markets will pick apart the statement and endlessly parse the Fed Chair’s words in the press conference. But let’s step back and take a look at the impact of these Fed hikes thus far.

We know the economy is running at the best pace since before the financial crisis. We know that the jobless rate is near record lows. We know that consumer credit worthiness is at record levels. This has all happened, despite the Fed’s rate hikes.

What about debt service coverage? As rates are moving higher, are consumers showing signs of getting squeezed?

If we look back at the height of the credit bubble in 2008 (just prior to its burst), 13.22% of household income was going to service debt–within that number, 7.2% of household income was going to service mortgage debt. What about now? Debt service is now 10.2% of household income. And the mortgage piece is down to just 4.4%. This is the result of six years of zero interest rates, a massive QE program (which included the Fed’s purchase of mortgage bonds), and a government program that subsidized banks to refi high interest rate mortgages.

So the big question is, how has the Fed’s exit of QE effected the consumers ability to service debt? Are higher rates hurting?

Well, they started hiking rates in the fourth quarter of 2015. Total debt service at that time was 10.1%. That’s virtually unchanged from today. And the mortgage piece was 4.5%. That’s actually a touch higher than today.

Bottom line: The Fed’s normalization on rates has not damaged the consumer, nor has it killed the housing market.

But that’s only because the yield curve has been flattening. That is, longer term market interest rates have been steady. That means the benchmark rate from which consumer and mortgage rates have been set, has been steady. And those longer term rates have been steady, in large part, because Europe and Japan have remained in QE mode (buying global assets, which includes our Treasurys).

With that, while most have been watching the Fed closely for how it’s delicately handling the exit of QE, the more important spot to watch will be how Europe and Japan manage their exits. Hopefully, the U.S. economy is hot enough, at that point, to withstand the move in longer term U.S. rates that will come with the end of global QE.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Yesterday Trump made good on his promise by announcing another $200 billion in tariffs on China.

To the surprise of many, stocks went up. Why?

Perhaps it’s because reforming the way the world deals with China is a good thing. Remember, China’s currency manipulation over the past two decades led to the credit bubble, which ultimately led to the financial crisis. And as long as the rest of the world continues to allow China to maintain a trade advantage (dictated by their currency manipulation): 1) they will manufacture hot economic growth through exports, 2) the global cycle of booms and bust will continue, and 3) the wealth transfer from the rest of the world to China will continue.

With this in mind, as I’ve said, the trade dispute is all about China – everything else Trump has taken on (Canada, Mexico, Europe) has been to gain leverage on getting movement in China.

With Trump now making it very clear that he won’t back down until major structural change takes place in China, it’s no surprise that one of the biggest winners of the day (following the further economic sanctions on China) was Japan!

The Nikkei was up big today. And it was Japanese stocks that set the tone for global markets on the day. As a signal that China’s days of cornering the world’s export markets may be coming to an end, Japan is in position to be a big winner.

Remember, while much of the world has returned to new record highs following the global financial crisis, Japan remains 40% away from the record highs set nearly 30 years ago.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Those that look for reasons to pick apart the bull case for the economy and markets were disappointed by the ECB this morning.

As we discussed earlier in the week, the improvements in the U.S. economy and the trajectory of U.S. rates has cleared the path for Europe to finally exit QE. And the ECB confirmed this morning that they remain on that path — to end QE into the year end.

The idea that Europe can exit QE is a huge positive for both the European economy and the global economy – a confidence signal.

With that, German stocks are a big buy here. As you can see in the chart below, while the S&P 500 is on record highs, the DAX has been well underwater on the year (down more than 6%).

The index also trades well under the 200 day moving average (the purple line). To close the performance gap in this chart, German stocks could be in the early stages of a 13%-15% run.

And stocks in Europe should be supported by a strengthening euro.

Remember, as the global economy improves, the dollar should get weaker. The growth and rate gap (between the U.S. and the rest of the world) will be narrowing from here, which will promote foreign capital to flow into currencies like the euro. But most importantly, the exit of QE means Europe has escaped the dangerous crisis era, which means money will flow “back home“ out of/from the world’s safe-haven asset (dollar-denominated U.S. Treasury market).

I suspect the euro will trade closer to 1.30 by this time next year, as the ECB will begin raising rates in 2019, and likely follow the U.S. lead on fiscal stimulus to drive growth.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

I hope everyone had a great Fourth of July yesterday. Today, the markets continue to be thinly traded as we head into the jobs report tomorrow.

We did get minutes from the recent Fed meeting today. This is a closer look into the views of the Fed from their June meeting. Of course, we already had a lot of information from that June meeting: the Fed hiked rates for the second time this year, they telegraphed an additional hike for the year in their projections, plus the June meeting was also accompanied by a press conference from Fed chair Jay Powell. And his explicit “main takeaway” was … “the economy is doing very well.”

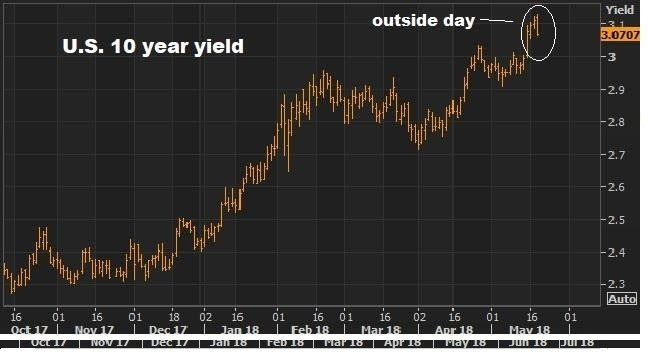

With this in mind, as we head into tomorrow’s jobs numbers, the 10-year yield is probably the most important chart to watch. While inflation isn’t near reflecting an economy that’s running hot, the interest rate market is even more disconnected.

Remember, back on May 18, in my ProPerspectives note, we discussed this chart …

As the world was becoming concerned with the speed and level of market interest rates, we had this big technical reversal signal hit for the key 10-year government bond yield.

We focused on this in my May 18th piece, where I said “this technical phenomenon, when closing near the lows, is a very good predictor of tops and bottoms in markets, especially with long sustained trends.” And I said, “I suspect we may have seen some global central bank buyers of our Treasuries today (which puts downward pressure on yields) to take a bite out of the momentum.”

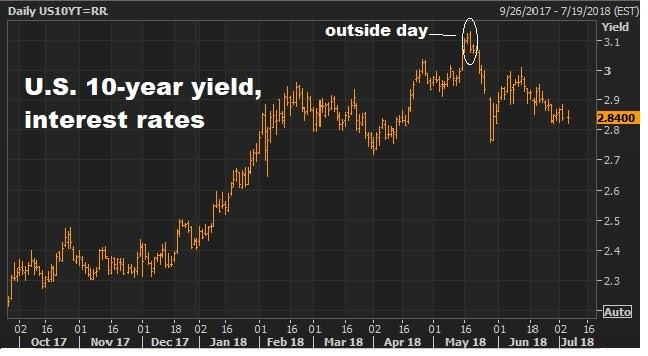

Today the chart looks like this …

So, that outside day did indeed predict a reversal. And we head into tomorrow’s job report with the benchmark 10-year yield at just 2.84%. That’s in a world where the economy is running at 3% growth and unemployment is under 4%.

But this disconnect may be changing tomorrow. The key data point tomorrow will be wages (Average Earning), not jobs. A hot number there will likely turn this around, and bring higher rates back into the picture.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Tech stocks and small caps continue to behave like an economy that is about to take off.

The Nasdaq is now up 14% on the year. The Russell 2000 is up 10%. The S&P 500 (with more global exposure) is lagging it all, up just 4%.

Is it telling us that the investments in the U.S. are gaining more favor, relative to the rest of the world? Maybe. Is it telling us that capital is flowing toward the U.S. to align with Trump policies and away from those that may be harmed by being on the wrong side of Trump. Maybe.

With that said, we know Europe has been slowing. We know the “Italy-risk” presents another drag on that outlook. As such, the ECB followed the Fed’s hike yesterday with a rather dovish outlook this morning. Draghi laid out a timeline for following the Fed’s lead on normalization that was a little slower/ little later than expectations. That sent the dollar soaring, the euro plunging, and rates in Europe lower.

Tonight, we hear from the Bank of Japan. Remember, this is the lynchpin in keeping a lid on global interest rates. As long as they have the QE spigot wide-open, our yields (and therefore our consumer rates) will be well contained.

Japan’s policy on pegging its 10-year yield at zero has been the anchor on global interest rates. Forcing their benchmark government bond yield back to zero, in a world where there has been upward pressure on interest rates, has meant that they can, and will, buy unlimited amounts of JGBs to get the job done. That equates to unlimited QE. When they finally signal a change to that policy, that’s when rates will finally move.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Watching the media and expert community digest the Fed decision is always interesting.

They are all programmed to home in on the worst-case scenario. It’s very similar to the way they parse politics.

In this case, the Fed projected an extra rate hike this year. They were projecting three hikes for 2018. Now they are projecting four hikes for the year (two of which are now in the rear-view mirror). Why an extra hike? Is it because they want to disrupt the recovery and undo all of their efforts of the past decade to manufacture that recovery? No. It’s because they think the economy is good! In fact, Powell (the Fed Chair) said “the main takeaway is that the economy is doing very well.”

And when asked about the impact of tax cuts, he said, we’ve yet to see the benefits. But, it should “provide significant support to demand over the next three years … encourage greater investment … and drive productivity.” This is exactly what we stepped through last week in my Pro Perspective notes (here). We laid out the components of GDP (consumption, investment, government spending and net exports) and we talked about the setup for positive surprises feeding into an economy that’s already running at near 3% growth — because pro-growth policies are just beginning to show up in the data!

With that, it should be no surprise that the Fed feels more comfortable telegraphing another hike, from what is still very low levels of interest rates.

Now, what is the negative scenario the pundits have been harping on? The yield curve. With the Fed gradually walking up short term rates (rates they set), the benchmark market interest rates (namely the 10-year government bond yield) has been soft. That creates yield curve flattening, which gets the bears excited that a yield curve inversion could be coming (a good historical predictor of recession).

Why is the 10 year yield soft? As we’ve discussed, the two major central banks that are still in the QE game have been anchoring longer term interest rates through their outright purchases of global government bonds (including lots of U.S. Treasuries, which keeps a cap on yields).

On that note, we have the ECB tomorrow. And the Bank of Japan will meet on monetary policy tomorrow night. The trajectory of global monetary policy is UP. And the more the Fed does, the more it forces that timeline elsewhere in the world to follow the Fed’s path on normalizing rates. The ECB will be following the Fed normalization path soon. And the Bank of Japan will be last. And when we get hints that it’s coming sooner rather than later, the yield curve will start steeping, and the bears will have a very hard time justifying their “sky is falling” view.

We have a lot of geopolitical noise surrounding markets.

Let’s step through them:

1) Yesterday, we discussed the Trump trade threats with China:

How is it playing out?

We have an economy that is leading the global economic recovery. China wants and needs to be part of it. Trump’s bark, with the credibility to bite, is creating movement. It’s creating compliance. That’s becoming a very positive catalyst for global economy and for geopolitical stability (the exact opposite of what the experts have predicted these tactics would produce).

2) We’ve talked about the shock-risk developing in Europe. A coalition government forming in Italy, with an “Italy first” approach to the social and economic agenda, has created some flight of Italian bond market capital toward safety. This has people skittish about another blowup threat of the euro zone.

How is it playing out?

The last time Italy was on default/blow up watch, the 10 year yields were 7% (unsustainable levels). At those levels, the ECB had to intervene.

This recent move in the Italian bond markets leaves yields at just 2.4% …

This looks like Grexit, Brexit and the Trump election. It creates leverage for the third largest economy in the European Union (excluding Britain). In this case, we may see it result in a loosening of fiscal constraints in the European Union – and an EU wide fiscal stimulus plan to follow the lead of the U.S.

3) The North Korean nuclear threat …

How is it playing out?

Eight months ago, North Korea launched a missile over Japan. Markets barely budged, and the world continued to turn. Now, we’ve quickly gone from an imminent threat to potential denuclearization. And now a meeting has been cancelled. With that, on the continuum of this relationship, I’d say it’s closer to its best point, rather than its worst.

Bottom line, these risks should do little to stop the momentum of the economy and the stock market.

Last week, rising market interest rates in the U.S. were becoming a concern. But as we discussed on Friday, we ended the week with a big bearish reversal signal in the 10-year yield. This week, the market focus seems to be shifting toward a lower dollar and higher commodities.

Friday’s bearish signal in rates seems to have foreshadowed the news coming into today’s session, that Italy is putting forward an agreement for a coalition government that would break compliance from EU rules (an “Italy first” approach to an economic and social agenda).

That has created some flight to safety in the bond market. You can see in this chart below, money moving out of Italian bonds (yields go up) and into German bonds (yields go down).

And that means money goes into U.S. Treasuries too. So you can see U.S. yields (the purple line in the chart below) backing off of the highs of last week, and with room to move back toward 3% (or below) if this dynamic in Italy continues to elevate the risk environment.

Now, with the rate picture softening, the dollar may be on the path of softening too. That would be a welcome site for emerging market currencies. We discussed last week how the push higher in U.S. yields was putting pressure on emerging market currencies. And the combination of weaker currencies and higher dollar-denominated oil prices was a recipe for economic strain.

Today, Larry Kudlow, the Chief Economic Advisor to the White House, carefully crafted a response on the dollar, as to not say they favored it “stronger.” That’s probably enough, given the rising risks in emerging markets, to get the dollar moving lower (to alleviate some of the pain of buying dollar-denominated oil for some of the EM countries).

And it may be the signal for commodities to start moving again. Because most commodities are priced in dollar, commodities prices tend to be inversely correlated to the dollar.

Today we had a fresh three-year high in the benchmark commodities index (the CRB Index).

Here’s an excerpt from one of my Forbes Billionaire’s Portfolio notes back in June, on the building momentum for commodities: “The technology sector minted billionaires over the past decade. It’s in commodities that I think we’ll see the new billionaires minted over the next decade. The only two times commodities have been this cheap relative to stocks was at the depths of the Great Depression in the early 30s and at the end of the Bretton Woods currency system in the early 70s. Commodities went on a tear both times.”

We’ve talked this week about the pressure that rising U.S. market interest rates are putting on emerging markets.

The fear surrounding the big 3% marker for U.S. 10-year yields is that 3% may quickly become 4%. And a 4% yield, much less a quick adjustment in this key benchmark interest rate, would cause some problems.

Not only does it create capital flight out of areas of the world where rates are low, and monetary policy is heading the opposite direction of the Fed, but a quick move to a 4% yield on the 10-year would certainly cloud the U.S. economic growth picture, as higher mortgage and consumer borrowing rates would start chipping away at economic activity.

With that said, we may have a reprieve with the action today in the bond market.

As we head into the weekend, today we get a softening in the rates market. And that came with a big technical reversal pattern (an outside day).

You can see in the chart above, the engulfing range of the day. This technical phenomenon, when closing near the lows, is a very good predictor of tops and bottoms in markets, especially with long sustained trends.

I suspect we may have seen some global central bank buyers of our Treasurys today (which puts downward pressure on yields) to take a bite out of the momentum. We will see if this quiets the rate market next week, for a drift back down to 3%. That would calm some of the nerves in global currencies, and global markets in general.

We talked yesterday about the building pressure in emerging markets, driven by weakening currencies and rising dollar-denominated oil prices.

With that bubbling up as a potential shock risk, gold hasn’t exactly been telling the story of elevated risks.

You can see in this chart above, since the tax cuts were passed in late 2017, rates have been rising (the purple line). This is a hotter economy, pick-up in inflation story. And, as it should, gold stepped higher with rates all along–until the last few weeks. You can see the divergence in the chart above.

I suspect we’ll see gold snap back to reflect some increasing market risks, and especially to reflect a world where central banks are beginning to finally see inflation pressures build. The gold bugs loved gold when inflation was dead. And now that it’s building, they are surprisingly very quiet.