Jobs, jobs everywhere there’s jobs. The President-elect yesterday said he will be the “greatest job creator God ever created.”

Since December, when the President-elect announced that Carrier, an air conditioner manufacturer in Michigan, would keep 1,000 jobs in the U.S. instead of moving them to Mexico, other companies have been lining up to announce big, bold hiring plans.

It was immediately clear that Carrier won priceless exposure and good-will. From that point, the Japanese billionaire Masayoshi Son took a visit to Trump Tower and followed with an announcement that his Softbank technology holdings company would invest $50 billion in U.S. businesses and create 50,000 new jobs. Softbank owns more than 80% of Sprint, and Sprint has followed with an announcement of 5,000 jobs to come.

Alibaba’s founder Jack Ma visited Trump Tower yesterday and left saying he would create 1 million jobs in the U.S.

Amazon, who’s CEO Jeff Bezos had a visit to Trump Tower last month, said today they plan to add 100k jobs.

Not to be outdone, Taco Bell (part of YUM Brands), said today it would add 1.6 million jobs in the U.S. Does this mean Taco Bell is about to go on a massive expansion increasing their store count by 5x — putting a Taco Bell on every corner in America?

Or, is this all just a public relations ploy? Are they all hoping to gain favor with the administration? Yes and yes. But it’s also all self-reinforcing. A better outlook for jobs is driving confidence. Confidence can drive a better outlook for jobs. More employed, more confident consumers can drive economic growth. And better growth drives more jobs.

Now, all of this said, the headline unemployment number is already down to 4.7% (near what is considered “normal”). The number that measures underemployed and those that have stopped looking is down to 9.2%. It’s much higher than the headline rate, but relative to history, it’s returning close to normal levels too. With the prospects of hotter growth coming, and new job creation, we could be headed for a very tight labor market. What does that mean? Higher wages are coming, to finally begin making up for two decades of wage stagnation.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

For two full months the Trump rally has consisted of higher stocks, higher yields, a higher dollar and higher commodity prices — all on the prospects of hotter growth and a sustainable period of prosperity ahead.

Since the night of November 8th, it’s been “buy it now, prove it to me later” market. But people are expecting there will be a period of time where the markets begin trading in “prove it to me” mode.

Often we see a “buy the rumor, sell the fact” phenomenon in markets — it’s a reflection of investors pricing new information in anticipation of an event, and then selling into the event on the notion that the market has already valued the new information. With that, the period surrounding the January 20th inauguration could be the “sell the rumor” moment (in fact, we may be working on it now).

Many are hoping it could be the second chance given to those that have been left behind in the great Trump reflation rally. The question is, how deep or shallow that correction might be, and how long or short-lived it might me.

I would argue, it’s going to short-lived and shallow (maybe very shallow), for all of the reasons I’ve discussed in this daily note, not the least of which, is a world starving for a return to meaningful and sustainable growth, and the perception that this is the best chance we’ve had and might have, to get the global economy back on track. Trump’s tone today, in his press conference, indeed, indicated that he would waste no time executing on his plan. That favors a short-and-shallow correction scenario for the Trump rally. And shallow corrections are typical of strong trending markets.

With that said, since the election, here’s a view of key markets (taking the last price before the election night whipsaw):

The yield on the 10-year has gone from 1.85% to over 2.64% on the Trump effect. But despite a surprisingly hawkish Fed on December 14th, and even more hawkish fundamental data since, the high in yields, thus far, was marked the day after the Fed meeting last month. And today yields traded just below 2.33%, the lowest since November 30th! For technicians, the 38.2% (Fibonacci) retracement of the entire move is 2.34%. That would be considered a shallow retracement.

The dollar (index) has gone from 97.68 to 103.82, and today trades at 101.28 which is the lowest level since December 14. Commodities (the broad commodity index) have gone from 183 to 193, and today trades at 191. Both have room for another 1% or so lower. The dollar looks very strong.

What about stocks? The S&P 500 has gone from 2,138 to 2,278, and now trades at 2,262. A shallow retracement for stocks of the Trump rally would be about 2,225 (which is about 2% lower from here). Given the policy outlook, those wishing for something deeper may not get the chance – a couple of percentage points from here may be the gift.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

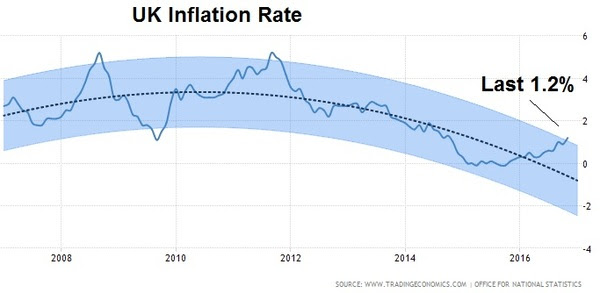

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

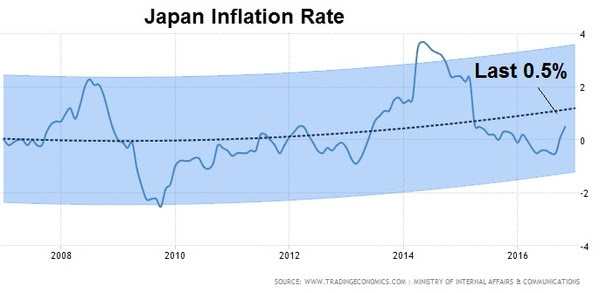

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We talked yesterday about the bad start for global markets in 2016. It was led by China. Today, it was a move in the Chinese currency that slowed the momentum in markets. Yields have fallen back. The dollar slid. And stocks took a breather.

China’s currency is a big deal to everyone. It’s the centerpiece of the tariff threats that have been levied from the U.S. President-elect. I’ve talked quite a bit about that posturing (you can see it again here: Why Trump’s Tough Talk On China May Work).

As we know, China, itself, sets the value of its currency every day. It’s called a managed float. They determine the value. And for the past two years, they’ve been walking it lower — weakening the yuan against the dollar. That’s an about face to the trend of the prior nine years. In 2005, in agreement with their major trading partners (primarily the U.S.), they began slowly appreciating their currency, in an effort to allay trade tensions, and threats of trade sanctions (tariffs).

So what happened today? The Chinese revalued its currency — pegged ithigher by a little more than a percent against the dollar. That doesn’t sound like a lot, but as you can see in the chart, it’s a big move, relative to the average daily volatility. That became big news and stoked a little bit of concern in markets, mostly because China was the sore spot at the open of last year, and the PBOC made a similar move around this time, when global marketswere spiraling.

Why did they do it? This time around, the Chinese have complained about the threat of capital flowing out of the country – it’s a huge threat to their economy in its current form. That’s where they’ve laid the blame, on the two year slide in the value of the yuan. With that, they’ve allegedly been fighting to keep the yuan stable and have been stepping up restrictions on money leaving the country. Today’s move, which included a spike in the overnight yuan borrowing rate, was a way to crush speculators that have been betting against the currency, putting further downward pressure on the currency. But it also likely Trump related – the beginning of a crawl higher in the currency as we head toward the inauguration of the new President Trump. It’s very typical for those under the gun for currency manipulation to make concessions before they meet with trade partners.

So, should we be concerned about the move today in China? No. It’s not another January 2016 moment. But the move did drive profit taking in twobig trends of the past two months: the dollar and U.S. Treasuries. With that, the first jobs report of the year comes tomorrow. It should provide more evidence that the Fed will hike a few times this year. And that should restore the climb in the dollar and in rates.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Remember this time last year? The markets opened with a nosedive in Chinese stocks. By the time New York came in for trading, China was already down 7% and trading had been halted. That started, what turned out to be, the worst opening stretch of a New Year in the history of the U.S. stock market.

The sirens were sounding and people were gripping for what they thought was going to be a disastrous year. And then, later that month, oil slid from the mid $30s to the mid $20s and finally people began to realize it wasn’t China they should be worried about, it was oil. The oil price crash was a ticking time bomb, about to unleash mass bankruptcies on the energy industry and threaten a “round two” of global financial crisis.

What happened? Central banks stepped in. On February 11th, the Bank of Japan intervened in the currency markets, buying dollars/selling yen. What did they do with those dollars? They must have bought oil, in one form or another. Oil bottomed that day. China soon followed with a move to boost bank lending, relieving some fears of a global liquidity crunch. The ECB upped its QE program and cut rates. And then the Fed followed up by taking two of their projected four rate hikes off of the table (of which they ended up moving just once on the year).

What a difference a year makes.

There’s a clear shift in the environment, away from a world on liquidity-driven life support/ and toward structural, growth-oriented change.

With that, there’s a growing sense of optimism in the air that we haven’t seenin ten years. Even many of the pros that have constantly been waiting for the next “shoe to drop” (for years) have gone quiet.

Global markets have started the year behaving very well. And despite the near tripling from the 2009 bottom in the stock market, money is just in the early stages of moving out of bonds and cash, and back into stocks. Following the election in November, we are coming into the year with TWO consecutive record monthly inflows into the U.S. stock market based on ETF flows from November and December.

The tone has been set by U.S. markets, and we should see the rest of the world start to play catch up (including emerging markets). But this development was already underway before the election.

Remember, I talked about European stocks quite a bit back in October. While U.S. stocks have soared to new record highs, German stocks have lagged dramatically and have offered one of the more compelling opportunities.

Here’s the chart we looked at back in October, where I said “after being down more than 20% earlier this year, German stocks are within 1.5% of turning green on the year, and technically breaking to the upside“…

And here’s the latest chart…

You can see, as you look to the far right of the chart, it’s been on a tear. Adding fuel to that fire, the eurozone economic data is beginning to show signs that a big bounce may be coming. A pop in U.S. growth would only bolster that.

And a big bounce back in euro zone growth this year would be a very valuabledefense against another populist backlash against the establishment (first Grexit, then Brexit, then Trump). Nationalist movements in Germany and France are huge threats to the EU and euro (the common currency). Another round of potential break-up of the euro would be destabilizing for the global economy.

With that, as we enter the year with the ammunition to end the decade long economy rut, there are still hurdles to overcome. Along with Trump/China frictions, the French and German elections are the other clear and present dangers ahead that could dull the efficacy of Trumponomics.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Happy New Year! We’re off to what will be a very exciting year for markets and the economy. And make no mistake, there will be profound differences in the world this year, with the inauguration of a new, pro-growth U.S. President, at a time where the world desperately needs growth.

I’ve talked a lot about the “Trump effect.” Clearly, when you come in slashing the corporate tax rate, creating incentives for trillions of dollars of capital to come home, and eliminating overhead and hurdles associated with regulation, you’ll get hiring, you’ll get spending, you’ll get investment and you’ll get growth.

But there’s more to it. Ray Dalio, one of the richest, best and brightest investors in the world has said, there is a clear shift in the environment, “from one that makes profit makers villains with limited power, to one that makes them heroes with significant power.”

The latter has been diminished over the past 10 years.

Clearly, we entered the past decade in an economic and structural mess. But while monetary policy makers were doing everything in their power (and then some) to avert the apocalypse and, later, fuel a recovery, it was being undone by law makers and a lack of fiscal support, swinging the pendulum too far in the direction of punishment and scapegoating.

With that, despite the continued wealth creation of the 1% over the past decade, and the widening of the inequality gap, the power of the wealth creators has been diminished in the crisis period – certainly, the public’s favor toward the rich has diminished. And most importantly, the incentives for creating value and creating wealth have been diminished.

With all of the nuances of change that are coming, and the many opinions on what it all means, that statement by billionaire Ray Dalio might be the most simple and clear point made.

Another good point that has been made by Dalio, as he’s reflected on the “Trump effect.” It’s the element that economists and analysts can’t predict, and can’t quantify. The prospects of the return of “animal spirits.” This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mis-trust of the system.

All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset appears to finally be underway. And that gives way to a return of animal spirits, which haven’t been calibrated in all of the forecasts for 2017 and beyond.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Last week we talked about how a visit to Trump Tower was becoming a good predictor of a success for your stock.

Goldman continues to build representation in the Trump administration with the latest addition, Gary Cohn (current COO and President of Goldman Sachs) as the National Economic Council Director. And hedge funder Anthony Scaramucci, a Goldman Sachs alum and current member of the Trump transition team, is rumored to be in the running for a role in the administration. Goldman’s stock continues to rise, as the best performer in the Dow Jones Industrial average since Election Day (up 31%).

And remember, we talked about the visit last week of Masayoshi Son, the Japanese billionaire and majority stake holder in Sprint. Sprint is up 32% since election day.

So now we have the latest, and one of the most important cabinet appointments, Rex Tillerson, who will be Secretary of State. He’s the Chairman and CEO of Exxon Mobil, the biggest energy company in the country and one of the largest publicly traded companies. Exxon was up 2% today, and is up 9% since the election — better than the broader market, but not quite as good as the stocks of some other Trump Tower visitors.

This is a very interesting pick. Given that the President-elect has openly talked about using oil as an economic weapon (on Iraq… “we should have taken the oil”). We now have one of the world’s most respected experts in oil, and in negotiating around oil, charged with stabilizing the middle east and relations with Russia (to name a few). And given that the hot spot of global instability surrounds countries (or regimes) that are highly dependendent on oil revenue (funded by oil revenue), we have a guy that could credibly utilize leverage emerging U.S. supply, and global demand of the developed world, as a bargaining chip. His appointment/presence may also end up yielding a stable oil price environment going forward (tempering the manipulation of price extremes by OPEC).

Follow me and look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up more than 27% this year. You can join me here and get positioned for a big 2017.

On Friday, we looked at five key charts that showed the technical breakout in stocks, interest rates, the dollar and crude oil.

All of these longer term charts argue for much higher levels to come. Remember, the big event remaining for the year is the December 14th Fed meeting. A rate hike won’t move the needle. It’s well expected at this stage. But the projections on the path of interest rates that they will release, following the meeting, will be important. As I said Friday, “as long as Yellen and company don’t panic, overestimate the inflation outlook and telegraph a more aggressive rate path next year, the year should end on a very positive note.”

On that note, today we had a number of Fed members out chattering about rates and where things are headed. Did they start building expectations for a more aggressive rate path in 2017, because of the Trump effect? Or, did they stick to the new strategy of promoting a view that underestimates the outlook for the economy and, therefore, the rate path (a strategy that was suggested by former Fed Chair Bernanke)?

The former is what Bernanke criticized the Fed as doing late last year, which he argued was an impediment to growth, as people took the cue and started positioning for a rate environment that would choke off the recovery. The latter is what he suggested they should move to (and have moved to), sending an ultra accommodative signal, and a willingness to be behind the curve on inflation — letting the economy run hot for a while (i.e. they won’t impede the progress of recovery by tightening money).

So how did the Fed speakers today weigh in, relative to this positioning?

First, it should be said that Bernanke also recently criticized the Fed for the cacophony of chatter from Fed members between meetings. He said it was confusing and disruptive to the overall Fed communications.

So we had three speakers today. New York Fed President William Dudley spoke in New York, St. Louis Fed President James Bullard spoke in Phoenix, and Chicago Fed President Charles Evans speaks in Chicago. Did they have a game plan today to promote a more consistent message, or was it a more of the disruptive noise we’ve heard in the past?

Fortunately, they were on message. Only Dudley and Bullard are voting members. Both had comments today that spanned from cautious to outright dovish. Dudley, the Vice Chair, wasn’t taking a proactive view on the impact of fiscal stimulus — he promoted a wait and see view, while keeping the tone cautionary. Bullard, a Fed member that is often swaying with the wind, said he envisioned ONE rate hike through 2019. That would mean, one in December, and done until 2019. That’s an amazing statement, and one that completely (and purposely) ignores any influence of what may come from the new pro-growth policies.

This is all good news for stocks and the momentum in markets. The Fed seems to be disciplined in its strategy to stay out of the way of the positive momentum that has developed. And that only helps their cause. With that, if today’s chatter is a guide, we should see a very modest view in the economic projections that will come on December 14th. That should keep the stock market on track for a strong close into the end of the year.

We may be entering an incredible era for investing. An opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade, or more. For help, follow me in my Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up 24% year to date. That’s more than three times the performance of the broader stock market. Join me here.

We talked last week about the Trump effect on stocks. With a new President promising aggressive growth polices and a supportive Congress in place to make it happen, the Trump plan is now being coined as Trumponomics.

As we discussed last week, the markets are reflecting this hand-off, from a Fed driven economy to a pro-growth government driven economy, positively — pricing in a period of hot growth. And it couldn’t come at a better time — in fact, it may come at the perfect time.

The Fed has been able to manufacture stability but not demand and inflation. Fiscal stimulus is designed to fill that void — to boost aggregate demand and inflation. That’s why the bond market has shifted gears so dramatically, now reflecting a world with a trillion dollar infrastructure spend on the table, tax cuts, deregulation and incentives to get $2.5 trillion of U.S. corporate capital repatriated. Prior to last week, despite all of the best efforts from global central banks, and a Fed that was telegraphing a removal of emergency policies, the bond market was reflecting a world that was in depression, with the 10-year yield well below 2% in the U.S. and negative rates throughout much of the world. Today the U.S. 10 year traded above 2.25%, returning to levels we saw last December, when the Fed made its first post-crisis rate hike.

As we’ve discussed, growth has a way of solving a lot of problems, including our debt problem. Politicians and economists love to scare people by emphasizing the enormity of our debt (close to $20 trillion). But our debt size is all relative — relative to the size of our economy, and relative to what’s going on in the rest of the world.

You can see, in a major economic downturn, debt tends to rise. And it has for everyone. The downturn has been global. And the rise in debt has been global.

The fears that a big debt load will lead to a dumping of the dollar, hyper-inflation and runaway interest rates don’t fit in this picture of a broadly weak recovery from a paralyzing global debt bust. Coming out of the worst global recession since World War II, inflation hasn’t been the problem. It’s been deflation. Inflation will be a concern when the structural issues are on the mend, employment is robust, confidence is high and the real economy is working. That hasn’t happened. But an aggressive and targeted government spending plan can finally start changing that dynamic.

And the markets are telling us, an inflationary environment is welcomed – it comes with signs of life.

Gold is the widely-loved inflation hedge. And gold isn’t rising out of concerns of overindebtedness. It’s falling hard in the past week, in favor of growth.

With this in mind, we may very well be entering an incredible era for investing – after a long slog. And an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade, or more. For help, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up 16% this year. That’s 2.5 times the performance of the broader stock market. Join me here.