For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

Brexit. Russia. Trump’s protectionist threats. Trump’s inability to get policies legislated. The French election.

The bears, those looking for a recession around the corner and big slide in stocks, are losing ammunition for the story.

With the threat of instability from the French election now passed, these are two of the more intriguing catch-up trades.

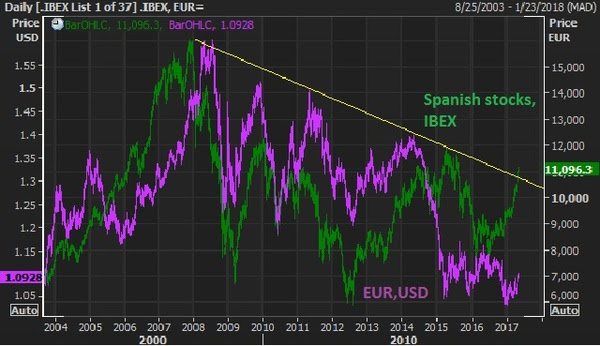

In the chart above, the green line is Spanish stocks (the IBEX). U.S., German and UK stocks have not only recovered the 2007 pre-crisis highs but blown past them — sitting on or near (in the case of UK stocks) record highs. Not only does the French vote punctuate the break of this nine year downtrend, but it has about 45% left in it to revisit the 2007 highs. And the euro, in purple, could have a dramatic recovery with the cloud of French elections lifted, which was an imminent threat to the future of the single currency.Next … Japanese stocks. While the attention over the past five months has been diverted toward U.S. politics and policies, the Bank of Japan has continued with unlimited QE. As U.S. rates crawl higher, it pulls Japanese government bond yields with it, moving the Japanese market interest rate above and away from the zero line. Remember, that’s where the BOJ has pegged the target for it’s 10 year yield – zero. That means they buy unlimited bonds to push the yield back down. That means they print more and more yen, which buys more and more Japanese stocks.

The Nikkei has been one of the biggest movers over the past couple of weeks (up almost 10%) since it was evident that the high probability outcome in the French election was a Macron win.Again, German, U.S., and UK stocks are at or near record highs. The Nikkei has been trailing behind and looks to make another run now, with 25,000 in sight.If you need more convincing that stocks can go much higher, Warren Buffett reiterated over the weekend that this low interest rate environment and outlook makes stocks “dirt cheap.” Last year he made the point that when interest rates were 15% [in the early 1980s], there was enormous pull on all assets, not just stocks. Investors have a lot of choices at 15% rates. It’s very different when rates are zero (or still near zero). He said, in a world where investors knew interest rates would be zero “forever,” stocks would sell at 100 or 200 times earnings because there would be nowhere else to earn a return.

Buffett essentially said at zero interest rates into perpetuity, the upside on the stock market (and any alternative asset class with return) is essentially infinite, as people are forced to find return by taking risk. Why you would buy a treasury bond that has no growth, and little-to-no yield and the same or worse balance sheet than high quality dividend stock.

This “forcing of the hand” (pushing investors into return producing assets) is an explicit objective by the interest rate policies of the Fed and the other major central banks of the world. They need us to buy stocks. They need us to spend money. They need economic growth.

If you have an brokerage account, and can read a weekly note from me, you can position yourself with the smartest investors in the world. Join us in The Billionaire’s Portfolio.

Over the past week, I’ve talked about the potential for disruption in what has been very smooth sailing for financial markets (led by stocks). While the picture has grown increasingly murkier, markets had been pricing in the exact opposite – which makes things even more vulnerable to a shakeout of the weak hands.

With that, it looked like we are indeed working on a correction in stocks. But it’s not just because stocks are down. It’s because we have some very important technical developments across key markets. The Trump trend has been broken.

Let’s take a look at the charts …

The above chart is the S&P 500. We looked at a break in the futures market last week. Today we get a big break in the cash market. This trendline represents the nice 45 degree climb in stocks since election night on November 8th. We have a clean break today.

Stocks ran up on the prospects that Trumponomics can end the decade long malaise in, not just the U.S. economy, but the global economy too. With that, the money that has been parked in U.S. Treasuries begins to leave. Moreover, any speculators that were betting the U.S. would follow the world into negative rate territory run for the exit doors. That sends Treasury bond prices lower and yields higher (as you can see in the chart above). So today, we also get a break of this “Trump trend” in rates as well (the yellow line). Remember, this is after the Fed’s rate hike last week — rates are moving lower, not higher.

Next up, gold …

I talked about gold yesterday — as being the clearest trade (higher) in an increasingly murkier picture for global financial markets. You can see in the chart above, gold is now knocking on the door of a break in this post-election Trump trend.

Remember, we’ve talked about the buy-the-rumor sell-the-fact phenomenon in markets. The beginning of the Trump trend in stocks started on election night (buying “the rumor” in anticipation of pro-growth policies). The top in stocks came the day following the President’s speech to the joint sessions of Congress (selling “the fact”, entering the “show me” phase).

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recent addition to the portfolio – a stock that one of the best activist investors in the world thinks will double.

One of the best investors on the planet, David Tepper, was on CNBC this morning. Let’s talk about how he sees the world and how he is positioned.

What I appreciate about Tepper: He’s a common sense guy.

And his common sense view of the world happens to be in alignment with the view and themes we discuss here every day. So he agrees with me – another thing I appreciate about him.

As you know, Wall Street and the media are always good at overcomplicating the investment environment with their day-to-day hyper analysis. Because of that, they tend to forge a path that moves further and further away from the simple realities of the big picture. That’s actually good. Because it creates opportunity for those that can avoid those distractions.

Right now, as we’ve discussed, the big picture is straight forward. We have a President that wants deregulation, tax cuts and a big infrastructure spend. And we have a Congress in place that can approve it. And this all comes at a time when the world has been in a decade long economic slog following the global financial crisis – in desperate need of growth. With that, we have a Fed that still has rates at very, very low levels. And the ECB and BOJ are still priming the pump with QE.

This is precisely Tepper’s view. He says the bowl is still full, i.e. the stimulus from the monetary policy side is still full, and now we get stimulus coming in from the fiscal side. What more could you ask for (my words) to pump up growth and asset prices, which will likely spill over into a pop in global growth. Still, people are underestimating it. And as he says, the Fed is underestimating it.

Are there risks? Yes. But the probability of growth, with the above in mind, well outweighs the probable downside scenarios. What about execution risk? Even if tax reform and infrastructure are slow to come, Tepper says deregulation is a done deal. It drives earnings and “animal spirits.”

He likes stocks. He likes European stocks. And I think he really likes Japanese stocks, but he stopped short of talking about it (my deduction).

Among the risks: Inflation picking up too fast, which would require the Fed to move faster, which could choke off growth (undo or neutralize fiscal stimulus).

This is why, among other reasons, Tepper’s favorite trade is short bonds. – i.e. higher interest rates. If he’s right and economic growth has a big pop, he wins. If the risk of hotter inflation materializes and rates move faster, he wins.

For context, this is the guy that literally changed global investing sentiment in late 2010 when he sat in front of a camera on CNBC, in a rare high profile TV interview (maybe first), when investing sentiment was all but destroyed by the global financial crisis and the various landmines that kept popping up. Tepper said in a very confident voice that the Fed, by telegraphing a second round of QE, had just given us all a free put on stocks (i.e. the Fed is protected the downside, it’s a greenlight to buy stocks). For all of the market jockeys that were constantly focusing on the many problems in the world, that commentary from Tepper, for some reason, woke them up.

For perspective on Tepper: Here’s a guy that is probably the best investor in the modern era. He’s returned between 35%-40% annualized (before fees) for more than 20 years. He made $7.5 billion in 2009 betting on financial stocks that most people thought were going bankrupt. And he was telling everyone that what the Fed is doing will make ‘everything’ go up. It sparked, in 2010, what is known as the “Tepper rally” in stocks.

When Tepper speaks it’s often smart to listen. And he likes the Trump effect!

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

The last data point for everyone to obsess about going into next week’s Fed meeting will be this Friday’s jobs report.

But as I’ve said for quite a while, the jobs data has been good enough in the Fed’s eyes for quite some time. Nonetheless, they’ve had many, many balks along the path of normalizing rates over the past couple of years. Here’s a look at a chart of the benchmark payrolls data we’ll be seeing Friday.

You can see in this chart, the twelve-month moving average is 195k. The three-month moving average is 182k. The six-month moving average is 182k. This is all fairly consistent with historical/pre-crisis levels.

So the numbers have been solid for quite some time, even meeting and exceeding the Fed’s targets, especially when it comes to the unemployment rate (4.7% last). However, when the Fed’s targets have been met, the Fed has moved the goal posts. When those goal posts were then exceeded, the Fed found new excuses to justify their decisions to avoid the path of aggressive hikes/normalization of rates that they had guided.

Among those excuses: When jobs were trending at 200k and unemployment breached 5%, the Fed started to acknowledge underemployment. Then the lack of wage growth became the focus. Then it was macro issues. To name a few: It’s been soft Chinese economic data, a Chinese currency move, Russian geopolitical tensions, collapsing oil prices, Brexit and weak productivity.

And just prior to the election last year, the Fed became, confusingly, less optimistic about the U.S. economic outlook, which was the justification to ratchet down the aggressive projected path for rates.

I suspected last year, when they did this that they were making a strategic pivot, to set expectations for a much easier path for rates, in hopes to keep people spending, borrowing and investing — instead of promoting a tighter path, which proved for the better part of two years (prior to the election) to create the opposite effect.

Remember, Bernanke (the former Fed Chair) even wrote a public piece on this last August, criticizing the Fed for being too optimistic in its projections for the path of interest rates. By showing the market/the world an expectation that rates will be dramatically higher in the coming months, quarters and years, Bernanke argued in his post that this “guidance” has had the opposite of the desired effect – it’s softened the economy.

A month later, in September, in Yellen’s post-FOMC press conference, she said this in response to why they didn’t raise rates: “the decision not to raise rates today and to wait for some further evidence that we’re continuing on this course is largely based on the judgment that we’re not seeing evidence that the economy is overheating.” Safe to argue, the economy isn’t overheating, still.

Again, as I said on Friday, the only difference between now and then, is the prospects of major fiscal stimulus, which is precisely what the Fed claims to be ignoring/leaving out of their forecasts – a believe it when I see it approach, allegedly.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

As we discussed last week, the Presidential address to the joint sessions of Congress last night was a big market event. And as I discussed yesterday, growth and fiscal stimulus needed to be moved to the front burner of the daily narrative. The President delivered last night.

After he began speaking, one of the early headlines on my Reuters feed last night: TRUMP SAYS HE WILL BE ASKING CONGRESS TO APPROVE LEGISLATION THAT PRODUCES $1 TRILLION INVESTING IN INFRASTRUCTURE FINANCED THROUGH BOTH PUBLIC AND PRIVATE CAPITAL.

Bingo! There’s a lot of talk about the inspiration of the speech, but growth is king in this environment, after 10 years of malaise and no improvement in sight. And the focus has shifted to growth. Stocks have had a huge day. Meanwhile, yields have been up but relatively tame. Gold has been down, but relatively tame. And the dollar has been up, but relatively tame.

German 2 year yields, which have been the sour spot, as they’ve slipped toward -1% in the past week, were up bouncing nicely today.

It’s not uncommon to see big global market participants ignore all else in key market moments, and just focus on one spot. That has been the case. And that spot is the stock market. The U.S. stock market is where the impact of a trillion dollar infrastructure spend, a massive tax cut, and broad deregulation can be most directly influenced and, as importantly, stocks are capable to absorbing large, large amounts of capital.

Now, it’s time to revisit some great catch up trades I’ve discussed for a while: German and Japanese stocks. A better U.S. is better for everyone, make no mistake. Hotter growth here, will mean hotter global growth, and it gives Europe and Japan a shot at recovery, especially with their central banks priming the pump with big QE, still.

On that note, let’s take a look at the charts …

So you can see the same period here for U.S., German and Japanese stocks, dating back to 2012, when the European Central Bank stepped in with intervention in the European sovereign bond market (at least promised to do so), that turned global economic sentiment and then then Japan came in months later with promises of a huge stimulus program. All stocks went up.

But you can see, stocks in Europe and Japan have yet to regain highs of 2015, after the oil price crash induced correction.

These stock markets look like a big catch up trade is coming, and it may be quick, following the catalyst of last nights U.S. Presidential address.

Follow The Lead Of Great Investors Like Warren Buffett In Our Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

Markets are quiet as we head into President Trump’s address to Congress tonight. As we’ve discussed over the past week or so, the markets seem to have run the course on the outlook of fiscal stimulus and regulatory reform within an environment of a gradual rise in interest rates.

That “expectation” backdrop seems to be pretty well priced in. Now, it’s a matter of detail and timing, and that puts the new President squarely in focus for tonight.

We’ve already heard from his Treasury Secretary last week that tax reform wouldn’t be coming until August-ish. And he said we shouldn’t expect that big growth bump from Trumponomics until 2018. That’s been the first real downward management of the expectations that have been set over the past three months.

What hasn’t been discussed much is the big infrastructure spend, which is really at the core of the pro-growth policies of the Trump administration. For years, the Fed has been begging Congress for help in stabilizing the economy and stimulating growth in it — from the FISCAL side.

Given the wounds of the debt crisis, it was politically unpalatable for Congress. They ignored the calls. And as a result, just six months ago we (and the rest of the world) were dangerously close to slipping back into crisis. Only this time, the central banks would not have had the ammunition to fight it.

So now we have Congress with the will and position to act. It’s a matter of detailing a plan and getting it moving. Of the many positive things that could come from tonight’s speech by President Trump, details and timeline on fiscal stimulus would be the biggest and most meaningful.

The bickering about deficits and debt will continue, but a big stimulus package will happen — it has to happen. A government spending led growth pop is, at this stage, the only chance we have of returning to a sustainable path of growth and ultimately reducing the debt load down the line, which now is about 100% of GDP. A move back to 80% of GDP would make the U.S. debt load, relative to the rest of the world, a non-issue.

Follow The Lead Of Great Investors Like Warren Buffett In Our Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

We had new record highs again in the Dow today. But remember, yesterday we talked about this dynamic where stocks, commodities and the dollar were strong. But a missing piece in the growing optimism about growth has been yields.

Clearly the 10 year at 2.40ish is far different than the pre-election levels of 1.75%-1.80%. But the extension was quick and has since been a non-participant in the full-on optimism vote given across other key markets.

Why? While stocks can get ahead of better growth, yields can’t in this environment. Higher stocks can actually feed higher growth. Higher yields, on the other hand, can kill it.

But there’s something else at work here. As we know Japan’s policy to target the their 10 year at zero provides an anchor to our interest rates, as the BOJ is in unlimited QE mode. Some of that freshly produced liquidity, and the money displaced by their bond buying, undoubtedly finds a happier home in U.S. Treasuries (with a rising dollar, and a 2.4% yield). That caps yields.

But in large part, the quiet drag on U.S. yields has also come from the rising risks in Europe. The election cycle in Europe continues to threaten a populist Trump-like movement, which is very negative for the European Union and for the survival of the single currency (the euro). That creates capital flight, which has been contributing to dollar strength and flows into the parking place of U.S. Treasuries (which pressures yields, which is keeping mortgage and other consumer rates in check).

These flows are also showing up clearly in the safest bond market in Europe: the German bunds. The 2-year German bund hit an all-time record LOW, today of -91 basis points. Yes, while the U.S. mindset is adjusting for the idea of a 3%-4% growth era, German yields are reflecting crisis and money is plowing into the safest parking place in Europe. The spread between German and French bonds are reflecting the mid-2012 levels when Italy and Spain where on the brink of insolvency — only to be saved by a bold threat/backstop from the European Central Bank.

We talked last week about the prospects for higher gold and lower yields as questions arise about the execution of (or speed of execution) Trump’s growth policies, some of the inflation optimism that has been priced in, may begin to soften. That would also lead to a breather for the stock market. I suspect we will begin to see the coming elections in Europe also contribute to some de-risking for the next couple of months. We already have a good earnings season and some solid economic data and optimism about the policy path priced in. May be time for a dip. But as I’ve said, it would create opportunities– to buy any dip in stocks, and sell any rally in bonds.

To peek inside the portfolio of Trump’s key advisor, join me in our Billionaire’s Portfolio. When you do, I’ll send you my special report with all of the details on Icahn, and where he’s investing his multibillion-dollar fortune to take advantage of Trump policies. Click here to join now.

There’s little in the way of economic data next week to move the needle on markets and the economic outlook. With that said, the catalyst will continue to be Trumponomics, and the President said yesterday that we should expect to hear “big things” coming in the next week or two.

As we head into the weekend, let’s take a look at some charts of interest.

The S&P 500 is now up 10% since election day (November 8). For some perspective, since the 2009 bottom, when the global central banks stepped in to pull the world back from the edge of collapse, you can see the trend has been a 45 degree angle UP. And despite all of the fear and pessimism along the way, the sharp corrections along the way were quickly reversed, most of which were completely recovered inside of ONE MONTH.

With central bank policy around the world still promoting higher global asset prices, and with pro-growth policies underway in the U.S., any dip in stocks will be a gift to buy.

We looked at this next chart last week. It’s the inverse price of gold versus the U.S. 10 year yield. You can see they have tracked nicely since the election.

With Yellen’s session on Capitol Hill this week, the yield has whipped around from 2.40 back to 2.50 and back to 2.41 today.

Meanwhile, with the continued hostility surrounding the Trump administration, and accusations about Russian conflicts, gold has been stepping higher. This all looks like higher gold and lower yields coming. As questions arise about the execution of (or speed of execution) growth policies, some of the inflation optimism that has been priced in may begin to soften. That would also lead to a breather for the stock market. In both cases, it would create opportunities — to buy any dip in stocks, and sell any rally in bonds.

Stocks finished the week on record highs. We talked earlier in the week about Trump’s meeting with Japan’s Prime Minister and his economic and finance advisors.

I suspect that Trump will come away, after a weekend in Palm Beach with Abe, learning that Abenomics is good for the U.S., and good global growth and stability (in the current global economic environment).

And one of the keys to success in Abenomics is a weaker yen, which translates to a stronger dollar. As I’ve said, the weak yen has been pulled into the fray with Trump’s tough talk on trade imbalances, but his beef on currency advantage is really directed toward China – not Japan, not Mexico, not even Europe.

With that, and with the assumption that the yen may be pardoned for a while, the dollar bouncing against the yen as we head into the weekend. And it looks like we may see a technical breakout and an even higher dollar, lower yen in our future.

And Japanese stocks look set to break out too, to catch up to the strength of U.S. stocks. The Nikkei is 8% off of the 2015 highs, while U.S. stocks are on record highs, and 8% ABOVE its 2015 highs.

Another catch up trade: German stocks. Despite the growing attention given to the French nationalist candidate, Le Pen, who has been anti-euro and anti-European Union, right or wrong the bond market isn’t showing any new interest in disaster insurance in Europe, nor is the euro.

With that, German stocks look very good, still about 8% from the 2015 highs, and the technical correction clearly ended last summer.

Lastly, let’s take a look at another big sleeper stock market, China…

You can see how Copper is on a big run (up 10% ytd). That typically correlates well with expectations of global growth. Global growth is typically good for China. Of course, China is in the crosshairs of Trump’s fair trade movement, but if you think there’s a chance that more fair trade terms can be a win for the U.S. and a win for China, then Chinese stocks are a bargain here.

Have a great weekend!

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We ended last week with a very strong jobs report, yet the measure of wage pressure was soft. That, for the near term, reduces expectations on how aggressive the Fed might be (but not a lot).

Still, the 10-year yield has drifted lower to start the week. It was 2.50% Friday afternoon. Today it’s closer to 2.40%. When the 10-year yield drifts lower, mortgage rates drift a little lower, back very close to 4% today. This all helps two of the most important tools the Fed has been focused on for the past eight years to drive economic recovery: stocks and housing.

The Trump administration, like the Fed, will need both stocks and housing to continue higher to maintain confidence in the economy, and in the agenda.

Now, on Friday I said Trump was hosting Japan’s Prime Minister Abe in Florida over the weekend for a round of golf at Mar-a-Lago. It looks like it’s this coming weekend, instead.

Interestingly, this comes as the Trump administration made a conscious effort on Friday to refocus the messaging from a protectionist narrative to an economic growth narrative.

Abe will be entering this meeting with President Trump under some peripheral scrutiny about trade imbalances. Japan runs about a $60 billion surplus with the United States. That’s about on par with Mexico, which has become a target for Trump in recent weeks. Still, as I said last week, it’s peanuts compared to China, and that’s where the Trump administration’s real attention lies.

Nonetheless, Abe is expected to come in with a plan to balance trade with the U.S., which includes working together on a big U.S. infrastructure program. And there is still considerable sensitivity surrounding the value of the yen (the Japanese currency).

As we know, under Abenomics, the yen has devalued by about 40% against the dollar. But as China has done often over the past decade, as they have headed into big meetings with global leaders, Japan seems to be walking its currency up in the days heading into the Abe/Trump meeting.

You can see in the chart above, the dollar has been in decline against the yen this year (the orange line falling represents a weaker dollar, stronger yen). The top in the USD/JPY exchange rate this year came when Trump’s chief trade negotiator was named on January 3rd. Robert Lighthizer worked in the Reagan administration and happened to be behind stiff tariffs imposed on Japan during that era on electronics.

Trump’s tough talk on trade, and the market’s continued focus on upcoming elections in Europe (that threaten to continue the trend of nationalism and protectionism) have stocks in Japan and Europe diverging from the strength we’re seeing in U.S. stocks. The Dow is above 20k. Meanwhile, Japanese stocks are still 10% off of the 2015 highs. German stocks are 7% off of 2015 highs.

But as I’ve said, growth solves a lot of problems. In addition to the underlying current of a better performing U.S. economy (with the pro-growth agenda in the pipeline), the data is already improving in both Germany and Japan. I suspect that Europe and Japan will soon be cleared from the fray of the trade protectionist rhetoric, and we’ll start seeing major European stock markets and the Japanese stock market climbing, and ultimately putting up a big number in 2017.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

{kind=link}