Stocks are sliding more aggressively today. Wall Street and the media always have a need to assign a reason when stocks move lower. There have been plenty of negatives and uncertainties over the past seven months — none of which put a dent in a very strong opening half for stocks.

But markets don’t go straight up. Trends have retracements. Bull markets have corrections. And despite what many people think, you don’t need a specific event to turn markets. Price can many times be the catalyst.

If we look across markets, it’s safe to say it doesn’t look like a market that is pricing in nuclear war. Gold is higher, but still under the highs of a month ago. The 10 year yield is 2.21%. Two weeks ago, it was 2.22%. That doesn’t look like global capital is fleeing all parts of the world to find the safest parking place.

Now, on the topic of North Korea, the media has found a new topic to obsess about– and to obsessively denounce the administration’s approach. With that, let’s take a look at the Trump geopolitical strategy of calling a spade a spade.

As we know, Mexico was the target heading into the election. Trump’s tough talk against illegal immigration and drug trafficking drew plenty of scrutiny. People feared the protectionist threats, especially the potential of alienating the U.S. from its third biggest trading partner. We’re still trading with Mexico. And the U.S. is doing better. So is Mexico. Mexican stocks are up 11% this year. The Mexican currency is up 13% this year.

China has been a target for Trump. He’s been tough on China’s currency manipulation and, hence, the lopsided trade that contributed heavily to the credit crisis. Despite all of the predictions, a trade war hasn’t erupted. In fact, China has appreciated its currency by 5% this year. That’s a huge signal of compliance. That’s among the fastest pace of currency appreciation since they abandoned the peg against the dollar more than 12 years ago (which was China’s concession to threats of a 30% trade tariff that was threatened by two senators, Schumer and Graham, back in 2005). And even in the face of a stronger currency (which drags on exports, a key driver of the economy), stocks are up 5% in China through the first seven months of the year.

Bottom line: It’s fair to say, the tough talk has been working. There has been compromise and compliance. So now Trump has stepped up the pressure on North Korea, and he has been pressuring China, to take the side of the rest of the world, and help with the North Korea situation – and through China is how the North Korea threat will likely get resolved.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

As we know, inflation has been soft. Yet the Fed has been moving on rates, assuming that they have room to move away from zero without counteracting the same data that is supposed to be driving their decision to increase rates.

Thus far, after four (quarter point) increases to the Fed funds rate, the moves haven’t resulted in a noticeable tightening of financial conditions. That’s mainly because the interest rate market that most key consumer rates are tied to have remained low. Because inflation has remained low.

A key contributor to low inflation has been low oil prices (though the Fed doesn’t like to admit it) and commodity prices in general that have yet to sustain a recovery from deeply depressed levels (see the chart below).

But that may be changing.

Commodities have been lagging the rest of the “reflation” trade after the value of the index was cut in half from the 2011 highs. Remember, we looked at this divergence between the stocks and commodities last month. Commodities are up 6% since.

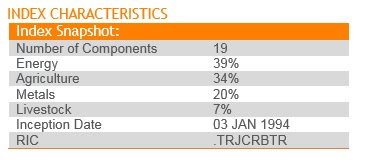

Things are picking up. Here’s the makeup of the broadly followed commodities index.

You can see, energy has a heavy weighting. And oil, with another strong day today, looks like a break out back to the $50 level is coming.With today’s inventory data, we’ve now had 12 out of the past 14 weeks that oil has been in a draw (drawing down on supply = bullish for prices). And with that backdrop, the CRB index, after being down as much as 13% this year, bottomed following the optimistic central bank commentary last month, and is looking like it may be in the early stages of a big catch-up trade. And higher oil (and commodity prices in general) will likely translate into higher inflation expectations.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

Healthcare was the story of the day today. With the Senate having had its go at the house healthcare bill, it goes back to the house, then back through Senate before it gets to the President’s desk.

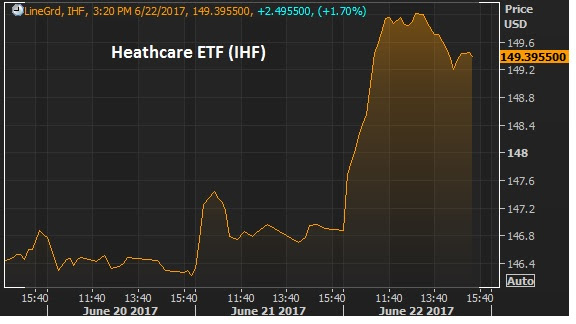

Still, policy progression is very positive in this environment. Healthcare stocks were up big today — the IHF healthcare ETF was up over 2%. This is the ETF that tracks insurers, diagnotic and specialized treatment companies.

And despite all of the debate around healthcare, it has been the hottest sector to invest in since the election.Since election day, the IHF is up 35% since the lows of November 9th, the day after the election. Here’s a look at S&P sector performance over the past sixmonths.

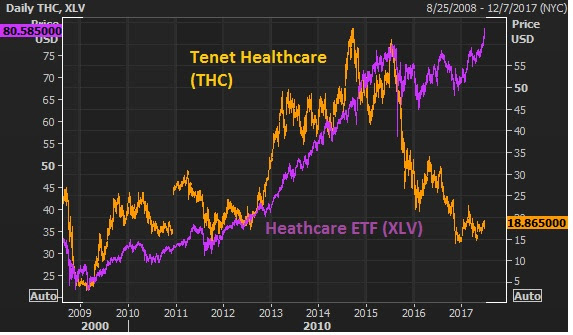

Most interesting, the healthcare sector has been beaten up badly since the cracks in Obamacare became clear back in 2014. But as of the past week, the healthcare sector trackers have finally broken back above those 2014 Obamacare–optimism–driven highs. With that, the divergence in this next chart of one of the biggest hospital companies in the country becomes quite an intriguing trade.

Join the Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

Today I want to take a look back at my March 7th Pro Perspectives piece. And then I want to talk about why a power shift in the economy may be underway (again).

Big Picture .. Market Perspectives March 7, 2017

“A big component to the rise of Internet 2.0 was the election of Barack Obama. With a change in administration as a catalyst, the question is: Is this chapter of the boom in Silicon Valley over? And is Snap the first sign?

Without question, the Obama administration was very friendly to the new emerging technology industry. One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007, before Obama announced his run for president, and just as Facebook was taking off after moving to and raising money in Silicon Valley (with ten million users). Facebook was an app for college students and had just been opened up to high school students in the months prior to Obama’s run and the hiring of the former Facebook cofounder. There was already a more successful version of Facebook at the time called MySpace. But clearly the election catapulted Facebook over MySpace with a very influential Facebook insider at work. And Facebook continued to get heavy endorsements throughout the administration’s eight years.

In 2008, the DNC convention in Denver gave birth to Airbnb. There was nothing new about advertising rentals online. But four years later, after the 2008 Obama win, Airbnb was a company with a $1 billion private market valuation, through funding from Silicon Valley venture capitalists. CNN called it the billion dollar startup born out of the DNC.

Where did the money come from that flowed so heavily into Silicon Valley? By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S.

When institutional investors see that kind of money flowing somewhere, they chase it. And valuations start exploding from there as there becomes insatiable demand for these new ‘could be’ unicorns (i.e. billion dollar startups).

Who would throw money at a startup business that was intended to take down the deeply entrenched, highly regulated and defended taxi business? You only invest when you know you have an administration behind it. That’s the only way you put cars on the street in NYC to compete with the cab mafia and expect to win when the fight breaks out. And they did. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation. Uber is valued at $60 billion. That’s more thanthree times the size of Avis, Hertz and Enterprise combined.

Will money keep chasing these companies without the wind any longer at their backs?”

Now, this was back in March. And that was the question — will it keep going under Trump? Can they continue to thrive/ if not survive without policy favors. Most importantly for the billion dollar startup world, will the private equity capital dry up. This is what it’s really all about. Will the money that chased the subsidies from D.C. to Silicon Valley for eight years (i.e. the trillion dollar pension funds) stop flowing? And will it begin chasing the new favored industries and policies under the Trump administration?

It seems to be the latter. And it seems to be happening in the form of a return to the public markets — specifically, the stock market.

And it may be amplified because of the huge disparity in what is being favored. In Silicon Valley, innovation is favored. Profitability? Remember, the 90s tech bubble. The measure of success for those companies was “eyeballs.” How much traffic were they getting to their websites? Today, when you hear a startup founder talk about the success benchmarks, it rarely has anything to do with with revenue or profit. It’s all about headcount (how many people they’ve hired) and money raised (which enables them to hire people). They are validated by convincing investors to fund them (mostly with our pension money).

Now, the other side of this coin: Trumponomics. Remember, among the Trump policies (corporate tax cuts, repatriation, deregulation, infrastructure spend), the most common sense play in the stock market has been flooding money into companies that make a lot of money. Those that make a lot of money have the most to gain from a slash in the corporate tax rate — it falls right to the bottom line. Leading the way on that front, is Apple. They make a lot of money. And they will make a lot more when a tax cut comes, making the stock even cheaper. That’s why it’s up 25% year-to-date. That’s 2.5 times the performance of the broader market.

Meanwhile, let’s take a look back at the Snapchat. Snapchat doesn’t make money. And even after a 1/3 haircut on the valuation, trades about 35 times revenue. And now, as a public company, probably doesn’t get the protection from the venture capital/private equity community that may have significant investments in its competitors. So the competitors (like Facebook) are circling like sharks to copy their business.

What about Uber? The Uber armor may be beginning to crack as well, with the leadership shakeup in recent weeks. Maybe a good signal for how Uber may be doing? Hertz! Hertz has bounced about 20% from the bottom this week.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

Yesterday, following the slide in stocks, we looked at some charts on stocks, gold and the dollar. We talked about the media and Wall Street’s need to fit price action to a story. And we asked if the story did indeed warrant fitting it to the price action. Was a crisis beginning or just a correction for stocks?The answer: It still looks like a market that values fiscal stimulus and structural change over political mudslinging and scandal. For stocks, the news may have been the catalyst to start a healthy technical correction.

Today, the market behavior appears to support that view.

Now, with the idea that a technical correction is (I think) underway for stocks, and maybe for months, until we get a better handle on policy action, remember this: a correction in stocks is a buying opportunity.

Major asset classes, over time, will rise (stocks, bonds, real estate). The value of these core assets will grow faster than the value of cash.

That comes with one simple assumption. The world, over time, will improve, will grow and will be a better and more efficient place to live than it was before. If that assumption turned out to be wrong, we have a lot more to worry about than the value of our stock portfolio.

With that said, as an average investor that is not leveraged, dips in stocks, particularly U.S. stocks—the largest economy in the world, with the deepest financial markets—should be bought, because in the simplest terms, over time, the broad stock market has an upward sloping trajectory. Instead, dips in stocks tend to create fear, and fear creates selling, at precisely the time we should be buying.

With this in mind, we’ve had a brief dip of about 4% in stocks within the “Trump trend” (the post–election rise in stocks). A typical correction is around 10%. But strong bull markets tend to have shallow retracements. A 6%–10% correction in stocks would take us back to the 200–day moving average (minimum), and maybe as low as 2,200 in the S&P 500.

Invitation to my daily readers: Join my premium service members at Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse portfolio of the most high potential stocks.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

For perspective: As of the close yesterday, the Nasdaq was up 18% year to date (just five months in). Gold was in the middle of a three year range. Market interest rates (the U.S. 10-year government bond yield) was just above the middle of the range of the past four years. The dollar was not far off its strongest levels in 15 years.

Today the media has explicitly printed the headline of impeachment for Trump (actually, they’ve run those headlines a various times over the past several months). Nonetheless, stocks (the S&P 500) today are off by 1.6%.

This gets the bears very excited. I saw the story about consumer debt, surpassing 2008 levels, floating all over the internet today. People tried to make the bubble connection — implying another debt crisis was coming.

The real story: Total household indebtedness finally surpassed the previous peak from 2008. That’s precisely what the Fed was attempting to do with zero interest rates. Make existing debt cheaper to manage, and at some point, break the psychology of the debt burden and get people borrowing (at ultra-cheap rates), investing and spending again. Otherwise, our economy and the world economy would have gone into a deflationary spiral.

That said, as I’ve found in my 20 years in this business, people tend to find a story to fit the price. The story hadn’t been fitting the price for much of the past six months. Today, it seems pretty easy. See the chart below of stocks ….

We had the first breakdown of the Trump trend in March, but all it could muster was about a 3% correction. This looks much more like a technical correction (a double top, and trend break today) – than a Trump impeachment trade. I suspect with the earnings catalyst behind us, this is the start of a deeper technical correction, which is healthy in a bull market. And it may take significant progress made in tax reform to see new highs in the broad stock indicies. We shall see.This next chart is the dollar index. This too had a significant trend break today. This translates into a higher euro, which would spell out a story where Europe is improving and the ECB is able in start discussing exit from QE.

What about the Trump/Comey saga? Aren’t people dumping dollars because of that? Not likely. If that were potentially destabilizing to the U.S., it would be destabilizing to the global economy, and people would buy dollars not sell them.

With that in mind, here’s gold. Gold sits on the brink of a big trend break (higher). When looking at gold and the dollar, it’s important to remember this: back in the heat of the crisis, gold and the dollar moved together, higher! That’s opposite of the traditional correlation. They moved higher together because people bought gold and they bought dollars (and dollar denominated assets, like Treasuries) as they viewed it the safest alternative in the world to park money – with the chance of getting it back.

With a break higher in gold looking imminent, and the dollar looking lower, it looks like a more traditional relationship. It’s not communicating crisis.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

Why is the messaging so different? Remember, the financial media and Wall Street are easily distractible. Not only do they have short attention spans, but they’ve been trained throughout their careers to find new stories to obsess about. They need to interpret, pontificate, strategize to feel valued. Approaching their jobs with the idea that a slow moving dominant theme is at work is just too boring.

This is the disconnect between markets and the narrative. We have major central banks around the world that continue to print money. These central banks buy assets with that freshly printed money. That means, stocks, bonds, commodities go higher. And now we have everyone’s fate (the global economy) tied to the outcome of new policies from the leading economy in the world – efforts to restore sustainable growth through structural reform and fiscal stimulus. That hopeful outlook does nothing but underpin the rise in asset prices (stocks, bonds, commodities, real estate).

Yesterday we got a look under the hood of the portfolios of the biggest money managers in the world, via their 13F filings (required quarterly portfolio disclosures to the SEC). It’s been clear that the biggest and best, embrace this big theme, and have been aggressively positioning to take advantage of the very bullish proposed policy tailwinds for stocks, which are: 1) a corporate tax rate cut, which will go right to the bottom line for profitable companies. Not surprisingly, which stocks have been leading the way in the climb in the indicies? The one’s that make a lot of money (Apple, Microsoft, Google). 2) a repatriation tax holiday that will bring back trillions of dollars onshore, to be paid back to shareholders and put to work in the economy through investment and projects. 3) a trillion dollar infrastructure spend that, regardless of how difficult it may be to legislate, should happen in one form or another.

Among the reports on portfolio holdings yesterday, we heard from the Swiss National Bank. As I said above, don’t forget there are still central banks deeply entrenched in QE and, beyond local government bonds, are buying foreign assets (in large amounts). Switzerland’s central bank has more freshly printed money to put to work every quarter, and has been increasing their allocation to equities dramatically – $80 billion of which is now (as of the end of Q1) in U.S. stocks! That’s a 29% bigger stake than they had at the end of 2016. The SNB is the world’s eighth biggest public investor.

So keep this big theme in mind: Central banks remain involved, but the baton has been passed, from a central bank-driven recovery to a fiscal stimulus-driven recovery. And everyone needs it to work.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

As for oil: From the depths of the oil price crash last year, remember, we discussed the prospects for a huge bounce. Oil prices at $26 were threatening to undo the trillions of dollars of work central banks and governments had done to stabilize the global economy. Central banks couldn’t let it happen. After a series of coordinated responses (from the BOJ, China, ECB and the Fed), oil bottomed and quickly doubled.

Also at that time, two of the best oil traders in the world were calling the bottom and calling for $70-$80 oil by this year (Pierre Andurand and Andy Hall). Another commodities king that called the bottom: Leigh Goehring.

Goehring, one of the best commodities investors on the planet, has also laid out the case for $100 oil by next year. He says he’s “wildly bullish” oil in his recent quarterly investor letter at his new fund, Goehring & Rozencwajg.

Goehring argues that the IEA inventory numbers are flawed. He thinks oil the market is already over-supplied and is in a draw, as of May of last year. With that, he thinks the OPEC cuts will ultimately exacerbate the deficit and send prices aggressively higher. He says “we remain ‘wildly’ bullish and believe that there is a very high probability of oil prices reaching triple digits in the first half of 2018.”

Follow This Billionaire To A 172% WinnerIn our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

Those that oppose it warn that it will lead to another financial crisis. On that note, I want to revisit my take from earlier this year on the cause of the crisis that almost destroyed the global economy.

“With all of the complexities of the housing bubble and the subsequent global financial crisis, it can seem like a web of deceit. But it all boils down to one simple actor. It wasn’t Wall Street. It wasn’t hedge funds. It wasn’t mortgage brokers. These entities were operating, in large part, from the natural force of economics: incentives.

It wasn’t even the government’s initiative to promote home ownership that led to the proliferation of mortgages being given to those that couldn’t afford them.

So who was the culprit?

It was the ratingsagencies.

Housing prices were driven sky high by the availability of mortgages. Mortgages were made easily available because the demand to invest in mortgages, to fund those mortgages, was sky high.

But what drove that demand to such high levels?

When the mortgages were combined together in a package (securitized as a mix of good mortgages, and a lot of bad/higher yielding mortgages), they were bought, hand over fist, by the massive multi-trillion dollar pension industry, banks and insurance companies. Yes, the guys that are managing your pension funds, deposit accounts and insurance policies were gobbling up these mortgage securities as fast as they could, but ONLY because the ratings agencies were stamping them all with a top AAA rating. Who would encourage such a thing? Congress. In 1984 they passed a law making it okay for banks, pension funds and insurance companies to buy/treat high rated secondary mortgages like they would U.S. Treasuries.

So as investment managers, in the business of building the best performing risk-adjusted portfolio possible, and in direct competition with their peers, they couldn’t afford NOT to buy these securities. They came with the safest ratings, and with juicy returns. If you don’t buy these, you’re fired.

To put it all very simply, if these securities were not AAA rated, the pension funds would not have touched them (certainly not to the extent). With that, if the there’s no appetite to fund the mortgages (no money chasing it), then the ultra-easy lending practices never happen, and housing prices never skyrocket on unwarranted and unsustainable demand. The housing bubble doesn’t build, doesn’t bust, and the financial crisis doesn’t happen.

That begs the question: Why did the ratings agencies give a top rating to a security that should have received a lower rating, if not much lower?

First, it’s important to understand that the ratings agencies get paid on the products they rate BY the institutions that create them. That’s right. That’s their revenue model. And only a group of these agencies are endorsed by the government, so that, in many cases, regulatory compliance on a financial product requires a rating from one of these endorsed agencies.”

Keep this in mind as the fear mongering over the talk of repeal of rework of Dodd Frank heats up.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Over the past few days, some of the most influential investors in the world have publicly shared views on some of their best ideas.First, over the weekend, it was Buffett at his annual shareholders meeting. The take away, as I said yesterday, “stocks are dirt cheap” if you think rates will stay low for longer (i.e. below long term averages). His assumption in that statement is that the Fed’s benchmark rate goes to 3ish% and done – well below the long run average neutral rate of 5%.

In addition, he was quite vocal on Apple, a stake he picked up as others were selling in fear in the first half of last year (i.e. being greedy when others are fearful). And he doubled his stake earlier this year, now holding north of $20 billion worth of the stock. The analyst community thinks Apple is a juggling act, with balls that will drop if they don’t come up with another revolutionary product every quarter. Buffett thinks Apple is cheap even if they don’t have another single new invention in the future. Why? Because they’ve developed a services business around their hardware that has quickly become one of the biggest and fastest growing businesses in the world.

Remember, back on February 1, I made the case for why Apple could double. You can see that here. It’s gone from a $560 billion company to an $800 billion company since we added it in our Billionaire’s Portfolio early last year. Even at $154 a share (today’s levels) if we strip out the quarter of a trillion dollars in cash, we get the existing business for 12 times earnings.

Now, let’s talk about one of the big ideas presented yesterday at the annual Sohn Conference in New York, where many of top billionaire investors and hedge fund managers give their outlook on the stock market, the economy and talk about their favorite long and/or short picks.

Billionaire investor Jeff Gundlach, who oversees the world’s largest bond fund likes selling the S&P 500 against emerging market stocks. He thinks value is distorted relative to global GDP. But it’s more a view on undervaluation of EM, rather than overvaluation of U.S. stocks. He took to Twitter to defend that view…

Assuming a stable to improving world economy, emerging market stocks have lagged and offer a great opportunity to catch up with the strength in the U.S. stock market. It also requires that emerging market currencies are a good bet against the dollar, if policy makers around the world are able to follow the lead of the Fed, where rising interest rate cycles follow. This is a very similar view to the one we discussed yesterday, where Spanish stocks (supported by a stronger euro) present a big catch up trade opportunity (to the tune of about 40% to revisit the 2007 highs), with the destabilization risk of the French elections in the rear-view mirror.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Yesterday, following the slide in stocks, we looked at some charts on stocks, gold and the dollar. We talked about the media and Wall Street’s need to fit price action to a story. And we asked if the story did indeed warrant fitting it to the price action. Was a crisis beginning or just a correction for stocks?The answer: It still looks like a market that values fiscal stimulus and structural change over political mudslinging and scandal. For stocks, the news may have been the catalyst to start a healthy technical correction.

Yesterday, following the slide in stocks, we looked at some charts on stocks, gold and the dollar. We talked about the media and Wall Street’s need to fit price action to a story. And we asked if the story did indeed warrant fitting it to the price action. Was a crisis beginning or just a correction for stocks?The answer: It still looks like a market that values fiscal stimulus and structural change over political mudslinging and scandal. For stocks, the news may have been the catalyst to start a healthy technical correction.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

Over the past few days, some of the most influential investors in the world have publicly shared views on some of their best ideas.First, over the weekend, it was Buffett at his annual shareholders meeting. The take away, as I said yesterday, “stocks are dirt cheap” if you think rates will stay low for longer (i.e. below long term averages). His assumption in that statement is that the Fed’s benchmark rate goes to 3ish% and done – well below the long run average neutral rate of 5%.

Over the past few days, some of the most influential investors in the world have publicly shared views on some of their best ideas.First, over the weekend, it was Buffett at his annual shareholders meeting. The take away, as I said yesterday, “stocks are dirt cheap” if you think rates will stay low for longer (i.e. below long term averages). His assumption in that statement is that the Fed’s benchmark rate goes to 3ish% and done – well below the long run average neutral rate of 5%.