We talked yesterday about the important inflation data. That was in line this morning. And with that, the big 3% level on the benchmark 10-year government bond yield remains well preserved.

But stocks soured anyway on the day, and it was led by the Nasdaq.

Let’s take a closer look at the Nasdaq.

This is where the big tech giants, Apple, Microsoft and Amazon have led the charge back in the index back to new record highs over the past couple of days. Those three stocks represent about a third of the index (and contribute heavily to the S&P 500 too).

But as the three tech giants led the way up, they cracked today, and we now have some very compelling signals that another down leg for stocks may be here.

First, as the broader financial markets are still licking the wounds of the sharp correction, and still jittery, Apple hit a record high valuation of $925 billion this week (sniffing near the trillion dollar valuation mark). And then it did this today…

As you can see in this chart above, Apple put in a huge bearish reversal signal (an outside day).

So did Microsoft (a huge bearish reversal signal).

So did Amazon, after breaching record levels of $1600 over the past two days …

And, not surprisingly, same is said for the Nasdaq – a big reversal signal…

The S&P 500 had the same reversal pattern.

For perspective, if we avoided the distraction of the big cap weighted indices, the Dow chart tells us the downtrend in stocks from the late January highs remains well intact.

As we discussed yesterday, stocks have fully recovered the decline that people were attributing to Trump’s trade barrier announcement last week.

With that, the tariff hysteria seems to have subsided a bit, as they struggle for evidence to support their hyperbole. Perhaps people may start acknowledging that we are now in a higher volatility environment, and that we will be slowly working out of this recent price correction until corporate earnings and economic growth data start confirming the benefits of tax cuts.

Interestingly, they seem to hate the trade threat, far more than the love the tax incentives and the pro-growth initiatives. And while trade is a complicated issue, everyone seems to suddenly have an expert opinion on it. And everyone is an expert on the Smoot-Hawley Act (which, by the way was a tariff on over 20,000 goods) and depression-era economics.

If they indeed were reflective about the economy, I think they would agree that we (and the world) desperately need growth initiatives to save us from terminal central bank life support (which wouldn’t be so terminal given they have fired all of their bullets to keep us afloat as long as they did). And they would know that we are in for a perpetual cycle of booms and busts (repeat of the credit bubble and burst) if the trade imbalances (mainly between China overproducing and the U.S. overconsuming) ultimately are not corrected.

Now, as more of the conversation on trade turns more toward China, I want to revisit an excerpt from my note in December of 2016 (when Trump was President-elect):

MONDAY, DECEMBER 19, 2016 — “While many think Trump will provoke a military conflict, that’s far from a certainty. With the credibility to act, however, Trump’s tough talk on China creates leverage. And from that leverage, there may be a path to a mutually beneficial agreement, where the U.S. can win in trade with China, and China can win. But it may get uglier before it gets better. In the end, growth solves a lot of problems. A hotter growing U.S. economy (driven by reform and fiscal stimulus), will ultimately drive much better growth in the global economy. And China has a lot to gain from both. Though in a fair-trade environment, they won’t get as much of the pie as they’ve gotten over the past two decades. But it has the chance of leading to a more balanced and sustainable economy in China, which would also be a win for everyone.”

Now, why not just focus on China now? Because they will continue to abuse other countries. And those open trade channels will still allow that product to enter the U.S. As we discussed yesterday, the global economy has been damaged by China’s currency/trade policy, yet the rest of the world has been relying on the U.S. to lead the fight. They need to join the fight to create the leverage to make it ultimately work – so that the global economy can find a sustainable path of recovery and robust growth.

Stocks continue to swing around, and in wider ranges than we’ve seen in a while. We should expect this type of action following a sharp technical correction–a correction that shook many of the players out of the market, that were contributors to suppressing volatility in recent years (the short vol ETFs among them).

Now, as I’ve said in the past, people always search for a story to fit the price. Despite the fact that stocks have been swinging around, with little or no story for them to attribute, they were quick to pounce on Trump’s announcement about steel tariffs, and have since blamed every down tick in the stock market for it. And they’ve run wild with trade war scenarios. For those trying to capitalize on that fear scenario, it shows how uninformed, naive or intellectually dishonest they are (most the latter). They like to evaluate it as if there is no context or history.

Where have they all been the past 20-plus years?

China has been manipulating the global markets through their cheap currency policy for the better part of the past 25 years. In pinning down their currency, they cornered the world’s export market. And in the process, they emerged as the second largest economy in the world. They also accumulated the world’s largest reserve of foreign currencies, which they plowed into global credit markets (mainly our Treasurys) to fuel cheap credit, which ultimately led to the global credit bubble and bust (the global financial crisis). We buy their cheap stuff. They take our dollars and buy Treasurys, supplying more credit to us to buy more of their cheap stuff. And so the cycle goes.

Currencies are the natural balancing mechanism to prevent this bubble/global imbalance from forming. When freely traded in an open economy, the market demand for yuan, given the aggressive growth in the economy, would have driven the value of China’s currency higher, making its exports less attractive, and therefore slowing their breakneck growth and wealth accumulation in China, and its ability to fuel global credit. But of course, the government determines the value of the yuan, and keeping the currency cheap is part of the economic model in China (still).

For those that fear retaliation (a historic response to protectionism), this is retaliation… for 20 years of wealth transfer.

The tariff threats address metals, but the currency is a key tool that makes it all happen. For those that like to play it as a political football, Trump is not the architect of the plan. A staunch democratic Senator from New York, Charles Schumer, led the push in Congress for a bill in 2005 to impose a 35% tariff on China. That’s what ultimately led to the agreement by the Chinese to allow their currency to weaken (somewhat). With that, I want to revisit my note from late September 2016 (prior to the elections) for a little more backstory on Why Trump Is Right About China (read more here).

If you are hunting for the right stocks to buy on this dip, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

Yesterday we talked about the commodities bull market and the move underway in natural gas.

That all continued today, thanks in part to a comment by the U.S. Treasury Secretary, saying “obviously a weaker dollar is good for us.” When the dollar goes down, commodities prices tend to go up, since they are largely priced in dollars. As such, commodities were the top performers of the day – beginning to gain more momentum at multi-year highs.

But as we’ve seen from this chart, this recovery in commodities, which has dramatically lagged in the reflation trade, has a long way to go.

While the markets reacted as if Mnuchin, the Treasury Secretary, was talking down the dollar, the dollar is already in a long-term bear market cycle.

Remember, we looked at this chart (below) of the long-term dollar cycles back in June…

And I said, “if we mark the top of the most recent cycle in early January, this bull cycle has matched the longest cycle in duration (at 8.8 years) and comes in just shy of the long-term average performance of the five complete cycles. The most recent bull cycle added 47%. The average change over a long-term cycle has been 56%. This all argues that the dollar bull cycle is over. And a weaker dollar is ahead. That should go over very well with the Trump administration.”

The dollar is down about 8% since then and is breaking down technically now.

The dollar index is now down 14% in this new bear cycle. And these are the early innings. Based on the dollar cycle, it has a long way to go, and should last for another 5 to 7 years.

So, this dollar outlook is further support for the case for a big run in commodities we’ve been discussing. And as we observed yesterday, in the case of Chesapeake Energy (CHK), the second largest producer of natural gas in the country, the commodities stocks are still extremely underpriced if this scenario for commodities plays out.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

With a government shutdown over the weekend, today I want to revisit my note from last month (the last time we were facing a potential government shutdown) on the significance of the government debt load.

The debt load is an easy tool for politicians to use. And it’s never discussed in context. So the absolute number of $19 trillion is a guarantee to conjure up fear in people – fear that foreigners may dump our bonds, fear that we may have runaway inflation, fear that the economy is a house of cards. So that fear is used to gain negotiating leverage by whatever party is in a position of weakness. For the better part of the past decade, it was used by the Republican party to block policies. And now it’s being used by the Democratic party to try to block policies.

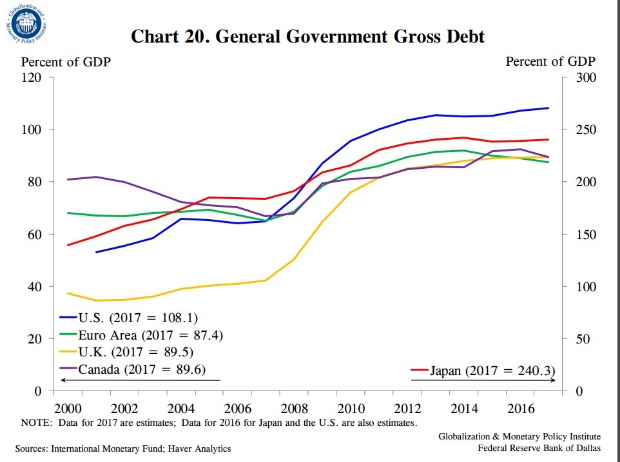

Now, the federal debt is a big number. But so is the size of our economy – both about $19 trillion. And while our debt/GDP has grown over the past decade, the increase in sovereign debtrelativetoGDP, has been a global phenomenon, following the financial crisis. Much of it has to do with the contraction in growth and the subsequent sluggish growth throughout the recovery (i.e. the GDP side of the ratio hasn’t been carrying its weight).

You can see in the chart below, the increasing debt situation isn’t specific to the U.S.

Now, we could choose to cut spending, suck it up, and pay down the debt. That’s called austerity. The choice of austerity in this environment, where the economy is fragile, and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession. Just ask Europe. After the depths of the financial crisis, they went the path of tax hikes and spending cuts, and by 2012 found themselves back in recession and a near deflationary spiral – they crushed the weak recovery that the European Central Banks (and global central banks) had spent, backstopped and/or guaranteed trillions of dollars to create.

The problem, in this post-financial crisis environment: if the major economies in the world sunk back into recession (especially the U.S.), it would certainly draw emerging markets (and the global economy, in general) back into recession. And following a long period of unprecedented emergency monetary policies, the global central banks would have limited-to-no ammunition to fight a deflationary spiral this time around.

Now, all of this is precisely why the outlook for the U.S. and global economy changed on election night in 2016. We now have an administration that is focused on growth, and an aligned Congress to overwhelm the political blocking. That means we truly have the opportunity to improve our relative debt-load through growth.

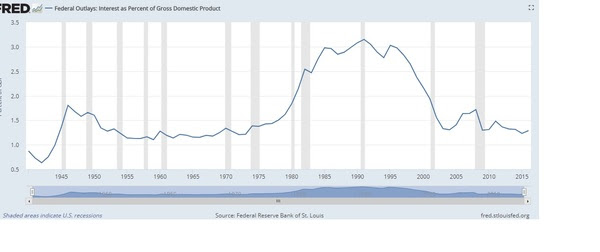

In the meantime, despite all of the talk, our ability to service the debt load is as strong as it’s been in forty years (as you can see in the chart below). And our ability to refinance debt is as strong as it’s been in sixty years.

For help building a high potential portfolio, follow me in our Forbes Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

government shutdown, washington, wall street, economy

Last week we talked about the big adjustment we should expect to come in the inflation picture. With oil above $60 and looking like much higher prices are coming, and with corporate tax cuts set to fuel the first material growth in wages we’ve seen in a long time (if not three decades), this chart (inflation expectations) should start moving higher…

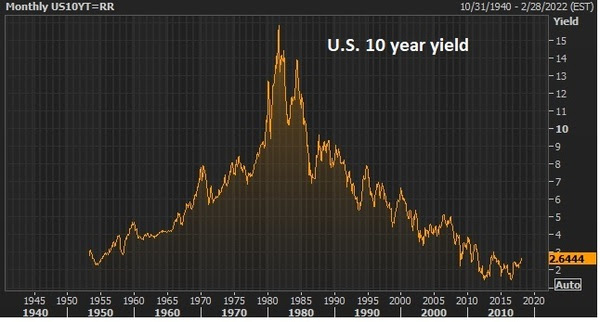

And with that, market interest rates should finally make a move. As we discussed last week, we will likely have a 10-year yield with a “3” in front of it before long.

Yields have already popped nearly a quarter point since the beginning of the year. But that’s just (finally) reflecting the December Fed rate hike. What hasn’t been reflected in rates, as it has in stocks, is the different growth and wage pressure outlook this year, thanks to the tax cut. Last year, people could argue it wasn’t going to happen. This year, it’s in motion. And the impact is already showing up. We should expect it to show in the inflation data, sooner rather than later.

With that, today we’re knocking on the door of a big breakout in rates (as you can see in the chart below) — which comes in at 2.65%…

As we’ve discussed, the anchor for the benchmark U.S. 10-year yield (and for global rates), even in the face of a more optimistic global economic growth outlook, has been Japan’s unlimited QE (driven by its policy to peg its 10-year at a yield of zero). On that note, last week, the former head of the central bank in India, Raghuram Rajan (a highly respected former central banker), said he thinks both Europe and Japan will exit emergency policies sooner than people think. That’s a positive statement on the global economy and a warning that global rates should finally start moving.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

Yesterday’s slide in stocks was all recovered today, despite the continued threat of a government shutdown. As we discussed yesterday, holding the government budget hostage to make gains on partisan demands hasn’t been enough to move the needle on the stock market the past three times we’ve seen it happen (2013, 1995-1996 and 1990).

Still, incredulously, the chatter about a “top” in stocks was heavy, yesterday afternoon and throughout this morning – given the 300 point move off of the top in the Dow (and accompanied by a sharp slide in bitcoin this morning).

The media and Wall Street experts must need to be reminded daily that we have a huge tax cut hitting this year, into extremely favorable economic conditions (low rates, cheap gas, record low unemployment, record high household net worth, record high consumer credit worthiness), with continued pro-business policies being executed, a major infrastructure spend pursued, and global growth expected to run as hot as we’ve seen since before the financial crisis.

With this in mind, Apple told us today that they plan to repatriate all of their offshore cash (about a quarter of a trillion dollars worth — thanks to a new, massive repatriation tax break), hire 20k people over the next five years and spend $30 billion in capex, to contribute $350 billion to the U.S. economy overall.

So, this is a direct result of incentives. And creating these incentives are the motivations behind the fiscal stimulus policies – all in an effort to achieve the behavior we’re seeing from Apple. Ultimately, it’s all about escaping the dangerously slow economic growth that was manufactured by central banks – so that the 10-year global economic slog doesn’t give way to a full-blown depression. So these incentives are working. Fiscal stimulus is working. And, as we’ve discussed, this should promote the big bounce back in growth that is typical of post-recession recoveries, but has been lacking in this post-financial crisis environment.

Still, people with the most influential voices continue to underestimate the outlook. The Fed is looking for just 2.5% U.S. GDP growth for the year (that’s likely less than what we’ll see for full year 2017). And Wall Street is looking for just 6% growth in stocks (according to this WSJ piece). The S&P 500 is already up 5%.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

Stocks reversed after a hot opening today. With a quiet data week ahead, the focus is on the prospects of a government shutdown.

If this sounds familiar to you, it should. Government debt is the, often played, go-to political football.

It was only last month that we were facing a similar threat. But with some policy-making tailwinds on one side of the aisle, the fight was politically less palatable in December. With that, Congress passed a temporary funding bill to kick the can to this month.

And just three months prior to that, in September, we had the same showdown, same result. The “government shutdown” card was being played aggressively until the hurricanes rolled through. From that point, politicians had major political risk in trying to fight hurricane aid. They kicked the can to December to approve that funding.

Now, the Democrats feel like they have some leverage, and their using the threat of a government shutdown to make gains on their policy agenda. So, how concerned should we be about a government shutdown (which could come on Friday)? Would it derail stocks?

If you recall, there was a lot of fuss and draconian warnings about an impending government shutdown back in 2013. The government was shutdown for 16 days. Stocks went up about 2%. Before that was 1995-1996 (stocks were flat), and 1990 (stocks were flat).

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

We kicked off the New Year continuing to discuss the theme of a hot stock market ahead (again) and a hotter than average economy (finally). Stocks continue to comply, with a big start – led by Japanese stocks today, up 2% on the day and up 4% on the year already.

It’s important to realize, the economic crisis was global. The central bank response was globally coordinated, led by the Fed. And, as we discussed early last year, everyone should hope Trumponomics works, because the global economy will benefit in coordination. And that’s what we’ve been seeing over the past year.

Of course, now we’re getting policy execution on that front, and we’re seeing the rising tide of the U.S. economy lifting all boats.

How high will that tide rise? As I said yesterday, if we add pro-growth policies that are being executed out of Washington, to an economy with near record low unemployment, cheap gas, near record low mortgage rates, record high consumer credit worthiness, record high household net worth, a record high stock market and near record low inflation, it’s hard to imagine the economy can’t do better than the long term average (3% growth) this year.

Let’s take a closer look at that economic growth picture.

Remember, in typical recessions, we should expect to get a big pop in growth to follow, due to policymaker responses to the slowdown and the natural upturn in the business cycle. In the Great Recession, we haven’t gotten it — after TEN years.

For the more than 50 years of history prior to the global financial crisis, U.S. economic growth averaged 3.5% (rolling four quarters). We’ve since averaged just 1.5% (over the past ten years). With that underperformance, the U.S. economy has foregone about $3 trillion dollars in real GDP growth, from being knocked off path by the global economic crisis. We’re due for a period to make up that ground.

On Tuesday we talked about the prospects of a return of “animal spirits” this year, for the first time in a long time. This is what can drive a period of economic growth that does better than the long term average. This animal spirits kicker may be the real theme of 2018.

But what is it?

Economics is about incentives. Economists think you’ll make rational decisions, with the incentive to best serve your interests. But emotions come into play. These emotions might cause you to be more risk-aversein times where policies incentivize you to take more risks, and vice versa.

This “emotion override” has been the problem over the past decade. The Fed gave us all abundant incentives to go out and borrow and spend, to stimulate the economy. But the scars of the housing crash, joblessness and overindebtedness were too great. People saved. They paid down debt. That didn’t trust the outlook. The Fed wanted us to take risk and they got risk aversion.

It has taken a regime change and an ultra-aggressive fiscal stimulus and structural reform response to finally break that mindset. The execution on tax cuts looks like the catalyst that has gotten more people off the fence, and believing in a rosier outlook. But I don’t think anyone would argue that confidence is broadly running hot (animal spirits) – much less, in a state of euphoria (which would justify concern of a top in markets and the recovery).

Robert Shiller (Yale economist) describes animal spirits like this: There are good times when people have substantial trust… They make decisions spontaneously. They believe instinctively that they will be successful.”

We’re not there yet, but we may begin seeing it/feeling it this year. And with that, we may see some hot growth over the coming years.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. And 25% of our portfolio is in commodities stocks. You can join me here and get positioned for a big 2018.

We are off to what will be a very exciting year for markets and the economy.

Over the past two years I’ve written this daily piece, discussing the bigslow-moving themes that drive markets, the catalysts for change, and the probable outcomes. When we step back from all of the day to day noise that has distracted many throughout the time period, the big themes have been clear, and the case for higher stocks has been very clear. That continues to be the case as we head into the New Year.

As I’ve said, I think we’re in the early stages of an economic boom. And I suspect this year, we will feel it — Main Street will feel it, for the first time in a long time.

And I suspect we’ll see a return of “animal spirits.” This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mis-trust of the system. All along the way, throughout the recovery period, and throughout a quadrupling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset has been tough. But with the likelihood of material wage growth coming this year (through a hotter economy and tax cuts), we may finally get it. And that gives way to a return of animal spirits, which haven’t been calibrated in all of the economic and stock market forecasts.

With this in mind, we should expect hotter demand and some hotter inflation this year (to finally indicate that the global economy has a pulse, that demand is hot enough to create some price pressures). With that formula, it’s not surprising that commodities have been on the move, into the year-end and continuing today (as the New Year opens). Oil is above $60. The CRB (broad commodities index) is up 8% over the past two weeks – and a big technical breakout is nearing.

This is where the big opportunities lie in stocks for the New Year. Remember, despite a very hot performance by the stock market last year, the energy sector finished DOWN on the year (-6%). Commodity stocks remain deeply discounted, even before we add the influence of higher commodities prices and hotter global demand. With that, it’s not surprising that the best billionaire investors have been spending time building positions in those areas.

This year is set up to handsomely reward the best stock pickers.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. And 25% of our portfolio is in commodities stocks. You can join me here and get positioned for a big 2018.