We’ve past yet another hurdle of concern for markets this past week. Last Friday this time, we had a potential catastrophic category 5 hurricane projected to decimate Florida.

Though there was plenty of destruction in Irma’s path, the weakening of the storm through the weekend ended in a positive surprise relative what could have been.

So we end with stocks on highs. And remember, we’ve talked over past month about the quiet move in copper (and other base metals) as a signal that the global economy (and especially China) might be stronger than people think. Reuters has a piece today where they overlay a chart of economist Ed Yardeni’s “boom-bust barometer” over the S&P 500. It looks like the same chart.

What does that mean? The boom-bust barometer measures the strength of industrial commodities relative to jobless claims. Higher commodities prices and lower unemployment claims equals a rising index as you might suspect (i.e. suggesting economic boom conditions, not bust). And that represents the solid fundamental back drop that is supporting stocks.

With that in mind, consider this: In the recent earnings quarter, earnings and revenue growth came in as good as we’ve seen in a long time for S&P 500 companies. We have 4.4% unemployment. The rise in equities and real estate have driven household net worth to $94 trillion – new record highs and well passed the pre-crisis peaks (chart below).

Now, people love to worry about debt levels. It’s always an eye-catching headline.

But what happens to be the key long-term driver of economic growth over time? Credit creation (debt). The good news: The appetite for borrowing is back. And you can see how closely GDP (the purple line, economic output) tracks credit growth.

Meanwhile, and importantly, consumers have never been so credit worthy. FICO scores in the U.S. have reached all-time highs. So despite what the media and some of Wall Street are telling us, things look pretty darn good. Low interests have produced recovery, without a ramp up in inflation.

But as I’ve said, it has proven to have its limits. We need fiscal stimulus to get us over the hump – on track for a sustainable recovery. And we now have, over the past two weeks, improving prospects that we will see fiscal stimulus materialize — i.e. policy execution in Washington.

To sum up: People continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

Yesterday we looked at the charts on oil and the U.S. 10 year yield. Both were looking poised to breakout of a technical downtrend. And both did so today.

Here’s an updated look at oil today.

And here’s a look at yields.

We talked yesterday about the improving prospects that we will get some policy execution on the Trumponomics front (i.e. fiscal stimulus), which would lift the economy and start driving some wage pressure and ultimately inflation (something unlimited global QE has been unable to do).

No surprise, the two most disconnected markets in recent months (oil and interest rates) have been the early movers in recent days, making up ground on the divergence that has developed with other asset classes.

Now, oil will be the big one to watch. Yields have a lot to do, right now, with where oil goes.

Though the central banks like to say they look at inflation excluding food and energy, they’re behavior doesn’t support it. Oil does indeed play a big role in the inflation outlook – because it plays a huge role in financial stability, the credit markets and the health of the banking system. Remember, in the oil price bust last year the Fed had to reverse course on its tightening plan and other major central banks coordinated to come to the rescue with easing measures to fend off the threat of cheap oil (which was quickly creating risk of another financial crisis as an entire shale industry was lining up for defaults, as were oil producing countries with heavy oil dependencies).

So, if oil can sustain above the $50 level, watch for the inflation chatter to begin picking up. And the rate hike chatter to begin picking up (not just with the Fed, but with the BOE and ECB). Higher oil prices will only increase this divergence in the chart below, making the interest rate market a strong candidate for a big move.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Yesterday we talked about the Draghi remarks (head of the European Central Bank) that were intended to set expectations that the ECB might be moving toward the exit doors on QE and zero interest rate policy. That bottomed out global rates — which popped U.S. rates further today. The Bank of England piled on today, talking about rate normalization soon.

We’ve gone from 2.12% in the U.S. ten year yield to 2.25% in about 24 hours. These are big swings in the interest rate market – a big bounce and, as I’ve said, the bottom appears to be in for rates.

As importantly, this prepared speech by Draghi could very well cement the top in the dollar. It begins to tighten a very wide interest rate spread between the U.S. and global rates. We entered the year with the Fed going one way (tightening) while the rest of the world was going the other way (easing). That’s a recipe for capital to storm into U.S. assets — into the dollar. And now that may be over.

I’ve been researching long-term cycles in the dollar for a very long time and throughout the global financial crisis period, it these cycles in the world’s reserve currency have been my guidepost for drawing a lot of conclusions on markets and the outlook for capital flows over the past several years.

Despite the choppiness in the dollar for much of the crisis, if we look back at the cycles following the failure of the Bretton Woods system, we were able, very early on, to determine the dollar was in a bull cycle.

This view came in the face of all of the negative global sentiment toward the dollar in 2010. Foreign leaders were taking shots at the Fed, accusing the Fed of trying to destroy the dollar. People were calling for the end of the dollar as the world’s reserve currency. All the while, the dollar held firm and ultimately made an aggressive climb.

Take a look below at my chart on the long term dollar cycles…

I’ve watched this chart for quite some time, defining the five complete dollar cycles over the past nearly 40 years, and the most recent bull cycle.

If we mark the top of the most recent cycle in early January, this bull cycle has matched the longest cycle in duration (at 8.8 years) and comes in just shy of the long-term average performance of the five complete cycles. The most recent bull cycle added 47%. The average change over a long term cycle has been 56%. This all argues that the dollar bull cycle is over. And a weaker dollar is ahead. That should go over very well with the Trump administration.

Join the Billionaire’s Portfolioto hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

Today I want to take a look back at my March 7th Pro Perspectives piece. And then I want to talk about why a power shift in the economy may be underway (again).

Big Picture .. Market Perspectives March 7, 2017

“A big component to the rise of Internet 2.0 was the election of Barack Obama. With a change in administration as a catalyst, the question is: Is this chapter of the boom in Silicon Valley over? And is Snap the first sign?

Without question, the Obama administration was very friendly to the new emerging technology industry. One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007, before Obama announced his run for president, and just as Facebook was taking off after moving to and raising money in Silicon Valley (with ten million users). Facebook was an app for college students and had just been opened up to high school students in the months prior to Obama’s run and the hiring of the former Facebook cofounder. There was already a more successful version of Facebook at the time called MySpace. But clearly the election catapulted Facebook over MySpace with a very influential Facebook insider at work. And Facebook continued to get heavy endorsements throughout the administration’s eight years.

In 2008, the DNC convention in Denver gave birth to Airbnb. There was nothing new about advertising rentals online. But four years later, after the 2008 Obama win, Airbnb was a company with a $1 billion private market valuation, through funding from Silicon Valley venture capitalists. CNN called it the billion dollar startup born out of the DNC.

Where did the money come from that flowed so heavily into Silicon Valley? By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S.

When institutional investors see that kind of money flowing somewhere, they chase it. And valuations start exploding from there as there becomes insatiable demand for these new ‘could be’ unicorns (i.e. billion dollar startups).

Who would throw money at a startup business that was intended to take down the deeply entrenched, highly regulated and defended taxi business? You only invest when you know you have an administration behind it. That’s the only way you put cars on the street in NYC to compete with the cab mafia and expect to win when the fight breaks out. And they did. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation. Uber is valued at $60 billion. That’s more thanthree times the size of Avis, Hertz and Enterprise combined.

Will money keep chasing these companies without the wind any longer at their backs?”

Now, this was back in March. And that was the question — will it keep going under Trump? Can they continue to thrive/ if not survive without policy favors. Most importantly for the billion dollar startup world, will the private equity capital dry up. This is what it’s really all about. Will the money that chased the subsidies from D.C. to Silicon Valley for eight years (i.e. the trillion dollar pension funds) stop flowing? And will it begin chasing the new favored industries and policies under the Trump administration?

It seems to be the latter. And it seems to be happening in the form of a return to the public markets — specifically, the stock market.

And it may be amplified because of the huge disparity in what is being favored. In Silicon Valley, innovation is favored. Profitability? Remember, the 90s tech bubble. The measure of success for those companies was “eyeballs.” How much traffic were they getting to their websites? Today, when you hear a startup founder talk about the success benchmarks, it rarely has anything to do with with revenue or profit. It’s all about headcount (how many people they’ve hired) and money raised (which enables them to hire people). They are validated by convincing investors to fund them (mostly with our pension money).

Now, the other side of this coin: Trumponomics. Remember, among the Trump policies (corporate tax cuts, repatriation, deregulation, infrastructure spend), the most common sense play in the stock market has been flooding money into companies that make a lot of money. Those that make a lot of money have the most to gain from a slash in the corporate tax rate — it falls right to the bottom line. Leading the way on that front, is Apple. They make a lot of money. And they will make a lot more when a tax cut comes, making the stock even cheaper. That’s why it’s up 25% year-to-date. That’s 2.5 times the performance of the broader market.

Meanwhile, let’s take a look back at the Snapchat. Snapchat doesn’t make money. And even after a 1/3 haircut on the valuation, trades about 35 times revenue. And now, as a public company, probably doesn’t get the protection from the venture capital/private equity community that may have significant investments in its competitors. So the competitors (like Facebook) are circling like sharks to copy their business.

What about Uber? The Uber armor may be beginning to crack as well, with the leadership shakeup in recent weeks. Maybe a good signal for how Uber may be doing? Hertz! Hertz has bounced about 20% from the bottom this week.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

The last data point for everyone to obsess about going into next week’s Fed meeting will be this Friday’s jobs report.

But as I’ve said for quite a while, the jobs data has been good enough in the Fed’s eyes for quite some time. Nonetheless, they’ve had many, many balks along the path of normalizing rates over the past couple of years. Here’s a look at a chart of the benchmark payrolls data we’ll be seeing Friday.

You can see in this chart, the twelve-month moving average is 195k. The three-month moving average is 182k. The six-month moving average is 182k. This is all fairly consistent with historical/pre-crisis levels.

So the numbers have been solid for quite some time, even meeting and exceeding the Fed’s targets, especially when it comes to the unemployment rate (4.7% last). However, when the Fed’s targets have been met, the Fed has moved the goal posts. When those goal posts were then exceeded, the Fed found new excuses to justify their decisions to avoid the path of aggressive hikes/normalization of rates that they had guided.

Among those excuses: When jobs were trending at 200k and unemployment breached 5%, the Fed started to acknowledge underemployment. Then the lack of wage growth became the focus. Then it was macro issues. To name a few: It’s been soft Chinese economic data, a Chinese currency move, Russian geopolitical tensions, collapsing oil prices, Brexit and weak productivity.

And just prior to the election last year, the Fed became, confusingly, less optimistic about the U.S. economic outlook, which was the justification to ratchet down the aggressive projected path for rates.

I suspected last year, when they did this that they were making a strategic pivot, to set expectations for a much easier path for rates, in hopes to keep people spending, borrowing and investing — instead of promoting a tighter path, which proved for the better part of two years (prior to the election) to create the opposite effect.

Remember, Bernanke (the former Fed Chair) even wrote a public piece on this last August, criticizing the Fed for being too optimistic in its projections for the path of interest rates. By showing the market/the world an expectation that rates will be dramatically higher in the coming months, quarters and years, Bernanke argued in his post that this “guidance” has had the opposite of the desired effect – it’s softened the economy.

A month later, in September, in Yellen’s post-FOMC press conference, she said this in response to why they didn’t raise rates: “the decision not to raise rates today and to wait for some further evidence that we’re continuing on this course is largely based on the judgment that we’re not seeing evidence that the economy is overheating.” Safe to argue, the economy isn’t overheating, still.

Again, as I said on Friday, the only difference between now and then, is the prospects of major fiscal stimulus, which is precisely what the Fed claims to be ignoring/leaving out of their forecasts – a believe it when I see it approach, allegedly.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

The big event of the week will be President Trump’s speech to Congress tomorrow. We know the pro-growth agenda of the Trump administration. We know the framework is in place to make it happen (with a Republican controlled Congress). That alone has led to a “clear shift in the environment” as Ray Dalio has called it (head of the biggest hedge fund in the world) – I agree.

But we’re at a point now, with European elections approaching and political risk rising there, and with the reality setting in that execution on fiscal stimulus from Trumponomics won’t be coming quickly, markets are calming down a bit. As we discussed last week, yields are falling back, following the lead of record level lows set in the German 2-year bund yield (in deeply negative territory). That dislocation in the German government bond market, as other key market barometers have been pricing in bliss, has come as a warning signal.

Another event of interest: Warren Buffett’s annual letter was released over the weekend, and he was on CNBC for a long interview this morning.

First, I want to revisit his letter from last year: Last year, in the face of an oil price crash, and a stock market that had opened the year with the worse decline on record, Buffett addressed the fears and uncertainty in markets. He said the growth trajectory for America has been and will continue to be UP. “America’s economic magic remains alive and well.”

And the growth trajectory has to do with two key factors: Improvements in productivity and innovation.

On productivity, he said:“America’s population is growing about .8% per year (.5% from births minus deaths and .3% from net migration). Thus 2% of overall growth produces about 1.2% of per capita growth. That may not sound impressive. But in a single generation of, say, 25 years, that rate of growth leads to a gain of 34.4% in real GDP per capita. (Compounding effects produce the excess over the percentage that would result by simply multiplying 25 x 1.2%.) In turn, that 34.4% gain will produce a staggering $19,000 increase in real GDP per capita for the next generation. Were that to be distributed equally, the gain would be $76,000 annually for a family of four. Today’s politicians need not shed tears for tomorrow’s children. All families in my upper middle–class neighborhood regularly enjoy a living standard better than that achieved by John D. Rockefeller Sr. at the time of my birth. Transportation, entertainment, communication or medical services.”

On innovation, he said:“A long–employed worker faces a different equation. When innovation and the market system interact to produce efficiencies, many workers may be rendered unnecessary, their talents obsolete. Some can find decent employment elsewhere; for others, that is not an option. When low–cost competition drove shoe production to Asia, our once–prosperous Dexter operation folded, putting 1,600 employees in a small Maine town out of work. Many were past the point in life at which they could learn another trade. We lost our entire investment, which we could afford, but many workers lost a livelihood they could not replace. The same scenario unfolded in slow–motion at our original New England textile operation, which struggled for 20 years before expiring. Many older workers at our New Bedford plant, as a poignant example, spoke Portuguese and knew little, if any, English. They had no Plan B. The answer in such disruptions is not the restraining or outlawing of actions that increase productivity. Americans would not be living nearly as well as we do if we had mandated that 11 million people should forever be employed in farming. The solution, rather, is a variety of safety nets aimed at providing a decent life for those who are willing to work but find their specific talents judged of small value because of market forces. (I personally favor a reformed and expanded Earned Income Tax Credit that would try to make sure America works for those willing to work.) The price of achieving ever–increasing prosperity for the great majority of Americans should not be penury for the unfortunate.”

And, finally on stocks, he said (my paraphrase): Overtime, with the above growth dynamic in mind, stocks go up.“In America, gains from winning investments have always far more than offset the losses from clunkers. (During the 20th Century, the Dow Jones Industrial Average — an index fund of sorts — soared from 66 to 11,497, with its component companies all the while paying ever–increasing dividends.”

What a difference a year makes. This time, he releases his letter into a stock market that’s UP 6% on the year already. And there’s new leadership and policy change underway.

So all of this in the above was written a year ago, what does he think now? In his letter released over the weekend, Buffett AGAIN addresses the fears and uncertainties in markets.

We discussed on Friday the stages of a bull market which slowly moves from the state of broad pessimism, to skepticism to optimism and finally to euphoria, which tends to end the bull market. But as Paul Tudor Jones says (one of the great macro investors), the “last third of a great bull market is typically a blow-off, whereas the mania runs wild and prices go parabolic” (i.e. euphoria can last for a while).

The fact that Buffett is still addressing concerns about valuations and the future of the American economy, is more evidence that we’re far from euphoria (bubble-like territory that some like to often talk about) and were probably more like the area between skepticism to optimism.

About Valuation: As we’ve discussed many times here my daily Pro Perspectives piece, when rates are low, historically, valuations run higher than normal (a P/E of 20 or better). At a ten year yielding at 2.4% and fed funds at 75 basis points (well below the long run average) the forward P/E on the S&P is just 17.8x. That’s still cheap, relative to the alternative of owning bonds. That incentivizes money to continue to flow into stocks. And if we apply a 20 P/E earnings estimates for the next twelve months, we get about 12% higher on the S&P 500.

Now, let’s hear from the legend himself on the topic: Buffett said this morning, “We’re not in bubble territory, if interest rates were 7% or 8% then these prices would look exceptionally high, but you measure everything against interest rates, measured against interest rates, stocks are on the cheap side compared to historic valuations.”

By the way, on that “valuation note” for stocks, as you may recall I made the case early this month for why Apple (the largest component of the S&P 500) was cheap (Is Apple A Double From Here?). What does Buffett think? Buffett disclosed that he’s doubled his position in Apple since the beginning of the year. It’s now his second largest position at $17 billion. He thinks Apple will be the first trillion dollar company. Full disclosure: We own Apple in our Billionaire’s Portfolio along with Buffett and his fellow billionaire investor David Einhorn. We’re up 30% since adding it in March of last year.

Follow The Lead Of Great Investors Like Warren Buffett In Our Forbes Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

Yesterday we looked at the slide in yields (U.S. market interest rates — the 10-year Treasury yield). That continued today, in a relatively quiet market.

Let’s take a look at what may be driving it.

If you take a look at the chart below, you can see the moves in yields and gold have been tightly correlated since election night: gold down, yields up.

As markets began pricing in a wave of U.S. growth policies, in a world where negative interest rates were beginning to emerge, the benchmark market-interest-rate in the U.S. shot up and global interest rates followed. The German 10-year yield swung from negative territory back into positive territory. Even Japan, the leader of global negative interest rate policy early last year, had a big reversal back into positive territory.

And as growth prospects returned, people dumped gold. And as you can see in the chart above of the “inverted price of gold,” the rising line represents falling gold prices.

Interestingly, gold has been bouncing pretty aggressively since mid December. Why? To an extent, it’s pricing in some uncertainty surrounding Trump policies. And that would also explain the slow down and (somewhat) slide in U.S. yields. In fact, based on that chart above and the gold relationship, it looks like we could see yields back below 2.10%. That would mean a break of the technical support (the yellow line) in this next chart …

Another reason for higher gold, lower yields (i.e. higher bond prices), might be the capital flight in China. Where do you move money if you’re able to get it out in China? The dollar, U.S. Treasuries, U.S. stocks, Gold.

The data overnight showed the lowest levels reached in the countries $3 trillion currency reserve stash in 6 years. That, in large part, comes from the Chinese central banks use of reserves to slow the decline of their currency, the yuan. Of course a weakening yuan only inflames U.S. trade rhetoric.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

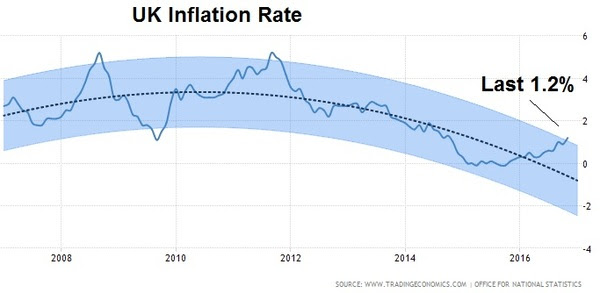

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

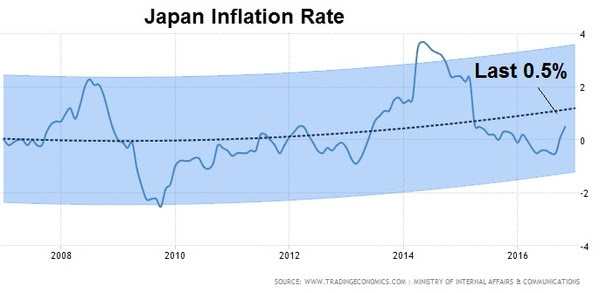

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We talked yesterday about the bad start for global markets in 2016. It was led by China. Today, it was a move in the Chinese currency that slowed the momentum in markets. Yields have fallen back. The dollar slid. And stocks took a breather.

China’s currency is a big deal to everyone. It’s the centerpiece of the tariff threats that have been levied from the U.S. President-elect. I’ve talked quite a bit about that posturing (you can see it again here: Why Trump’s Tough Talk On China May Work).

As we know, China, itself, sets the value of its currency every day. It’s called a managed float. They determine the value. And for the past two years, they’ve been walking it lower — weakening the yuan against the dollar. That’s an about face to the trend of the prior nine years. In 2005, in agreement with their major trading partners (primarily the U.S.), they began slowly appreciating their currency, in an effort to allay trade tensions, and threats of trade sanctions (tariffs).

So what happened today? The Chinese revalued its currency — pegged ithigher by a little more than a percent against the dollar. That doesn’t sound like a lot, but as you can see in the chart, it’s a big move, relative to the average daily volatility. That became big news and stoked a little bit of concern in markets, mostly because China was the sore spot at the open of last year, and the PBOC made a similar move around this time, when global marketswere spiraling.

Why did they do it? This time around, the Chinese have complained about the threat of capital flowing out of the country – it’s a huge threat to their economy in its current form. That’s where they’ve laid the blame, on the two year slide in the value of the yuan. With that, they’ve allegedly been fighting to keep the yuan stable and have been stepping up restrictions on money leaving the country. Today’s move, which included a spike in the overnight yuan borrowing rate, was a way to crush speculators that have been betting against the currency, putting further downward pressure on the currency. But it also likely Trump related – the beginning of a crawl higher in the currency as we head toward the inauguration of the new President Trump. It’s very typical for those under the gun for currency manipulation to make concessions before they meet with trade partners.

So, should we be concerned about the move today in China? No. It’s not another January 2016 moment. But the move did drive profit taking in twobig trends of the past two months: the dollar and U.S. Treasuries. With that, the first jobs report of the year comes tomorrow. It should provide more evidence that the Fed will hike a few times this year. And that should restore the climb in the dollar and in rates.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We’ve past yet another hurdle of concern for markets this past week. Last Friday this time, we had a potential catastrophic category 5 hurricane projected to decimate Florida.

We’ve past yet another hurdle of concern for markets this past week. Last Friday this time, we had a potential catastrophic category 5 hurricane projected to decimate Florida.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.