The Fed decided to hike interest rates by another quarter point yesterday. That was fully telegraphed and anticipated by markets. That’s the third rate hike this year, and the fifth in the post-crisis rate hiking cycle.

Still, the yield on the 10-year Treasury note (the benchmark market determined interest rate), moved lower today, not higher — and sits unchanged for the year.

We talked earlier in the week about the biggest central bank event of the month. It wasn’t the Fed, but it will be in Japan next week. Japan’s policy on pegging their 10-year yield at zero has been the anchor on global interest rates.

When they signal a change to that policy, that’s when rates will finally move.

With this divergence between what the Fed is doing (setting rates) and what market rates are doing (market-determined), people have become convinced that the interest rate market is foretelling a recession coming — i.e. short term rates have been rising, while longer term rates have been quiet, if not falling. For example, when the Fed made it’s first rate hike in December of 2015, the 30-year government bond yield was 3%. Today, after five rate hikes on the overnight Fed determined interest rate, the 30-year is just 2.72% (lower, not higher than when the Fed started).

This dynamic has created a flattening yield curve. That gets people’s attention, because historically, when the yield curve has inverted (short term rates rise above long term rates), recession has followed every time since 1950, with one exception in the late 60s.

And it turns out, this “flattening of the yield curve” indicator, historically (and ultimate inversion, when it happens), is typically driven by monetary policy (i.e. rate hikes — check). In these cases, the market anticipates the Fed killing growth and eventually leading rate cuts! They find more certainty and stability in owning longer term bonds (leaving short term bonds pushing those rates up and moving into long term bonds, pushing those rates down — inverting the curve).

The question, is that the case this time? Or is this time different. It’s rarely a good idea in markets to think this time is different than the past. But in this case, following trillions of dollars of central bank intervention and a near implosion in the global economy, it’s probably safe to say that this time is certainly different than past recessions. Though the Fed is in a hiking cycle, rates remain well below long term averages. And, as we know, we have unconventional monetary policies at work in other key areas of the world — stoking liquidity, growth and skewing demand for U.S. Treasuries (which suppresses those long term interest rates).

So the flattening yield curve fears are probably misplaced, especially given big fiscal stimulus is coming. And when Japan moves off of its “zero yield policy,” the U.S. yield curve may steepen more quickly than people think is possible.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

This morning we got a report that smallbusiness optimism hit the second highest level in the 44-year history of the index.

Here’s a look at that history …

optimism

Remember, last year, following the election, this index that measures the outlook from the small business community had the biggest jump since 1980 (as you can see in the chart).

Why were they so excited? For most of them, they had dealt with a decade long crisis in their business, where they had credit lines pulled, demand for their products and services were crushed, healthcare costs were up and their workforce had been slashed. If they survived that storm and were still around, any sign that there could be a radical change coming in the environment was a good sign.

A year ago, with a new administration coming in, half of the smallbusiness owners surveyed, expected the economy to improve. That was the largest agreement of that view in 15 years.

They’ve been right.

Now with an economy that will do close to 3% growth this year, still, about half of small business owners expect the economy to improve further from here.

No surprise, they are more than pleased with the tax cuts coming down the pike. They’ve seen regulatory relief over the past year. And, according the chief economist for the National Federation of Independent Businesses, small business owners see the incoming Fed Chair (Powell) as more favorable toward business (and market determined decisions) than Yellen. And he says, “as long as Congress and the President follow through on tax reform, 2018 is shaping up to be a great year for small business, workers, and the economy.”

This reflects the theme we’ve talked about all year: the importance of fiscal stimulus to bridge the gap between the weak economic recovery that the Fed has manufactured, and a robust sustainable economic recovery necessary to escape the crisis era. This small business survey tends to correlate highly with consumer confidence. Consumer confidence drives consumption. And consumption contributes about two-thirds of GDP. So, by restoring confidence, the stimulative policy actions (and the anticipation of them) has been self-reinforcing.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We had a jobs report this past Friday. The unemployment rate is at 4.1%. We’re adding about 172k jobs a month on average, over the past twelve months. These are great looking numbers (and have been for quite some time). Yet employees, broadly speaking, still haven’t been able to command higher wages. Wage growth continues to be on the soft side.

With little leverage in the job market, consumers tend not to chase prices in goods and services higher — and they tend not to take much risk. This tells you something about the health of the job market (beneath the headline numbers) and about the robustness of the economy. And this lack of wage growth plays into the weak inflation surprise that has perplexed the Fed. And the weak growth that has perplexed all policy makers (post-crisis). That’s why fiscal stimulus is needed!

And this could all change with the impending corporate tax cut. The biggest winners in a corporate tax cut are workers. The Tax Foundation thinks a cut in the corporate tax rate would double the current annual change in wages.

As I’ve said, I think we’re in the cusp of an economic boom period — one that we’ve desperately needed, following a decade of global deleveraging. And today is the first time I’ve heard the talking heads in the financial media discuss this possibility — that we may be entering an economic boom.

Now, we’ve talked quite a bit about the run in the big tech giants through the post-crisis era — driven by a formula of favor from the Obama administration, which included regulatory advantages and outright government funding (in the case of Tesla). And we’ve talked about the risk that this run could be coming to an end, courtesy of tighter regulation.

Uber has already run into bans in key markets. We’ve had the repeal of “net neutrality” which may ultimate lead big platforms like Google, Twitter, Facebook and Uber, to transparency of their practices and accountability for the actions of its users (that would be a game changer). And we now know that Trump is considering that Amazon might be a monopoly and harmful to the economy.

With this in mind, and with fiscal stimulus in store for next year, 2018 may be the year of the bounce back in the industries that have been crushed by the “winner takes all” platform that these internet giants have benefited from over the past decade.

That’s probably not great for the FAANG stocks, but very good for beaten down survivors in retail, energy, media (to name a few).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

With all that’s going on in the world, the biggest news of the day has been Bitcoin.

People love to watch bubbles build. And then the emotion of “fear of missing out” kicks in. And this appears to be one.

Bitcoin traded above $16,000 this morning. In one “market” it traded above $18,000 (which simply means some poor soul was shown a price 11% above the real market and paid it).

As we’ve discussed, there is no way to value bitcoin. There is no intrinsic value. To this point, it has been bought by people purely on the expectation that someone will pay them more for it, at some point. So it’s speculation on human psychology.

Let’s take a look at what some of the most sophisticated and successful investors of our time think about it…

Billionaire Carl Icahn, the legendary activist investor that has the longest and best track record in the world (yes, better than Warren Buffett): “I don’t understand it… If you read history books about all of these bubbles…this is what this is.”

Billionaire Warren Buffett, the best value investor of all-time: “Stay away from it. It’s a mirage… the idea that it has some huge intrinsic value is a joke. It’s a way of transmitting money.”

Billionaire Jamie Dimon, head of one of the biggest global money center banks in the world: “It’s not a real thing. It’s a fraud.”

Billionaire Ray Dalio, founder of one of the biggest hedge funds in the world: “Bitcoin is a bubble… It’s speculative people, thinking they can sell it at a higher price…and so, it’s a bubble.”

Billionaire investor Leon Cooperman: “I have no money in bitcoin. There’s euphoria in bitcoin.”

Billionaire distressed debt and special situations investor, Marc Lasry: “I should have bought bitcoin when it was $300. I don’t understand it. It might make sense to try to participate in it, but I can’t give you any analysis as to why it makes sense or not. I think it’s real, as it coming into the mainstream.”

Billionaire hedge funder Ken Griffin: “It’s not the future of currency. I wouldn’t call it a fraud either. Bitcoin has many of the elements of the Tulip bulb mania.”

Now, these are all Wall Streeters. And they haven’t participated. But this all started as another disruptive technology venture. So what do billionaire tech investors think about it…

Billionaire Jerry Yang, founder of Yahoo: “Bitcoin as a digital currency is not quite there yet. I personally am a believer that digital currency can play a role in our society, but for now it seems to be driven by the hype of investing and getting a return, as opposed to transactions.”

Mark Cuban: He first called it a “bubble.” He now is invested in a cryptocurrency hedge fund but calls it a “Hail Mary.”

Michael Novagratz, former Wall Streeter and hedge fund manager. He once was a billionaire and may be again at this point, thanks to bitcoin: “The whole market cap of all of the cryptocurrencies is $300 billion. That’s nothing. This is global. I have a sense this can go a lot further.” He equates it to an alternative to, or replacement for, the value of holding gold – which is an $8 trillion market… “over the medium term, this thing is going to go a lot higher.” But he acknowledges it shouldn’t be more than 1% to 3% of an average persons net worth.

Now with all of this in mind, billionaire Thomas Peterffy, one of the richest men in the country and founder of the largest electronic broker in the U.S., Interactive Brokers, has warned against creating exchange traded contracts on bitcoin. He says a large move in the price could destabilize the clearing organizations (the big futures exchanges) which could destabilize the real economy.

With that, futures launch on Bitcoin on Sunday at the Chicago Mercantile Exchange. This is about to get very interesting.

It’s hard to predict the catalyst that might prick a market bubble. And there always tends to be an interconnectedness across the economy to bubbles, that aren’t clear before it’s pricked (i.e. some sort of domino effect).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

With the potential government shutdown looming, let’s look at some perspective on government debt.

As we discussed early in the week, the policy execution pendulum for the Trump administration has swung over the past four months, from winless to potentially two big wins by the year end.

As I’ve said, with a massive corporate tax cut coming and big incentives for companies to build, invest and bring money back home (from overseas), we should be entering an economic boom period — one we have desperately needed, post-recession, but haven’t gotten.

Still, there are people that hate the tax cut idea. They think the economy is fine shape. And that debt is the problem. The Joint Committee on Taxation is the go to study for those that oppose the tax cuts. The study shows not a lot of growth, and disputes the case that the tax cuts will pay for themselves through growth.

What the headlines that cite this study don’t say, is that the study has huge assumptions that drive their conclusions. Among them, that creating incentives to repatriate $3 trillion in offshore corporate money will only contribute about a fifth of the taxable value of that amount of money. And they assume that the Fed will hike rates at a pace to precisely nullify any gains in economic activity (which wouldn’t be smart, unless they want to go revisit another decade of QE).

Now, with this study in mind, people are fearing the debt implications, on what is already a large debt load. And they fear that global investors might start dumping our Treasuries, as a result.

This has been a misguided fear throughout much of the post-financial crisis environment. Conversely, international investors have flocked into our Treasuries (lending us money), as the safest parking place for their capital. Why?

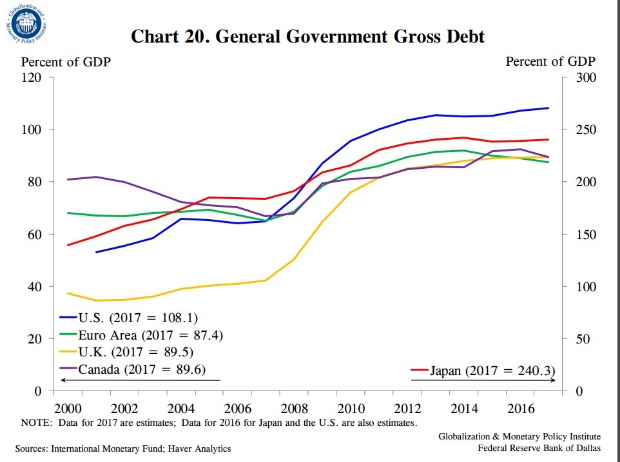

For perspective on the debt load and the fiscal stimulus decision, as we discussed earlier this week: “The national debt is a big number. But so is the size of our economy – about $19 trillion. Sovereign debt isn’t about the absolute number. It’s about the size of debt relative to the size of the economy. With that, it’s about our ability to service that debt at sustainable interest rates. The choice of austerity in this environment, where the economy is fragile and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession (as it did in Europe). And the outlook for re-emerging would be grim. That would make our debt/gdp far inferior to current levels — and our ability to service the debt, far inferior.”

Add to this, the increase in sovereign debt relative to GDP, has been a global phenomenon, following the financial crisis. Much of it has to do with the contraction in growth and the subsequent sluggish growth throughout the recovery (i.e. the GDP side of the ratio hasn’t been carrying it’s weight).

You can see in the chart above, the increasing debt situation isn’t specific to the U.S.

The euro zone tried the path of austerity back in 2011, and quickly found themselves back in recession, only re-emerging by promising to backstop the failing countries in the monetary union, and launching a massive QE program.

What about the government shutdown threats? Would it derail stocks? Stocks went up about 2% the last time the government shutdown in 2013. Before that was 1995-96 (stocks were flat) – and 1990 (stocks were flat).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

It looks like we’ll get tax cuts approved before year end! And that will give us two of the four pillars of Trumponomics underway in the first year of the new administration.

What a difference four months makes.

Remember, we entered the year with prospects of a big corporate tax cut, a huge infrastructure spend, deregulation and incentives to bring trillions of U.S. corporate money home.

By this summer, the ability to execute on these policies, given the political gridlock and mudslinging, was beginning to look questionable.

The game changer was the hurricanes.

In my note on August 29th, I said: “I think it’s fair to say the optimism toward the President, the administration and Washington policy making has been waning with the lack of policy execution. And from the optics of it all, sentiment couldn’t go much lower. But in markets, turning points (bottoms and tops) in the prevailing trend are often triggered by a catalyst (big trend changes, by some sort of intervention).

With that, the hurricane will likely have little negative impact on overall growth, but it may do something positive for policy making (maybe a turning point).

Given the mess of the political landscape, and an economy that remains vulnerable and in need of fiscal stimulus and structural reform, the crisis in Texas might serve as a needed catalyst: 1) to offer an opportunity for Trump to show leadership in a time of crisis, an opportunity to earn support and approval, and 2) to engage support for rebuilding, not just in Texas but throughout the U.S. (i.e. the much needed economic catalyst of infrastructure spend)…

National crises tend to be unifying. And in the face of national crisis, the barriers to get government spending going get broken down.

So, as we discussed last week, it may be the hurricanes that become the excuse for lawmakers to stamp more spending projects which can ultimately become that big infrastructure spend. And the easing of social tensions and political gridlock on policy making would all be highly positive for the global economic outlook.”

Of course that was followed by the big hurricane in Florida, and then in Puerto Rico. All told, the damages are north of $250 billion.

Congress has approved, to this point, about $60 billion in aid for hurricanes and wildfires (as far as I can track). And that number will likely go much higher — well into nine figure territory (probably more like a quarter of a trillion dollars). For Katrina, the ultimate federal aid disbursed was $120 billion.

On that momentum the first tranche of aid passed back in September, Trump went right to tax cuts. Three months later, and tax cuts are coming.

So, quickly, the policy execution pendulum has swung. This should pop growth nicely next year (and in Q4), which we desperately need to break out of the post-crisis rut of weak demand, slow growth and low inflation.

What about the $20 trillion debt load the media loves to talk about? It’s a big number. So is the size of our economy – about $19 trillion. Sovereign debt isn’t about the absolute number. It’s about the size of debt relative to the size of the economy. With that, it’s about our ability to service that debt at sustainable interest rates. The choice of austerity in this environment, where the economy is fragile and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession (as it did in Europe). And the outlook for re-emerging would be grim. That would make our debt/gdp far inferior to current levels — and our ability to service the debt, far inferior.

On the other hand, with fiscal stimulus underway, don’t underestimate the value of confidence in the outlook (“animal spirits) to drive economic growth higher than the number crunchers in Washington can imagine (the same one’s that couldn’t project the credit bubble, and didn’t project the sluggish 10 years that have followed).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn

Stocks fell sharply this morning, but recovered nearly all the losses from the lows of the day.

Today we got a reminder of the impact that algorithmic trading can have on markets. When the headline hit today about Flynn, here’s what stocks did…

Big institutions have been trading stocks through computer programs for a long time, but the speed at which these algorithms can access markets and information have changed dramatically over the past decade – so has the massive amount of assets deployed through high frequency trading programs. They can remove liquidity very quickly. Combine that with the reduced liquidity in markets that has resulted from the global financial crisis (i.e. the shrinkage of the marketing making community and of hedge fund speculators, and the banning of bank prop trading) and you get markets that can go down very fast. And you get markets that can go up very fast too.

The proliferation of ETFs exacerbates this dynamic. ETFs give average investors access to immediate execution, which turns investors into reactive traders. Selling begets selling. And buying begets buying.

Now, with the Flynn news, Wall Street and the financial media spend a lot of time trying to predict when the market will correct and what will cause it. But as the great billionaire investor, Howard Marks, has said: “It’s the surprises no one can anticipate that move markets. But most people can’t imagine them, and most of the time they don’t happen. That’s why they’re called surprises.”

Still, if you’re not a leveraged hedge fund, this tail-chasing game of trying to pick tops and reduce exposure at the perfect time shouldn’t apply.

More important is the observation that stocks remain cheap at current levels, when we consider valuations in historically low interest rate periods. And we continue to have very low interest rates. So the question is: Is it more likely that corporate earnings will get worse from here, or better from here?

There’s plenty of evidence to suggest the momentum and the fundamental backdrop supports “getting better” from here. And we add to that, the fuel of tax cuts, and earnings should continue to make stocks very attractive relative to a 2.3% ten-year yield.

The Dow is now up 23% on the year. The index that measures the broader market, the S&P 500, is up 18%. This is more than double the performance of the long run compounded average growth rate for the stock market.

People continue to be surprised that policy execution is improving, and that tax cuts are actually coming. And they speculate on whether or not the stock market already has it all priced in. I think the steady rise in stocks is telling them it’s not.

As I’ve said, we remain in an ultra-low interest rate world, where incentives continue to push money into stocks (as the best alternative). And in ultra-low rate environments, historically, the multiple on stocks (the P/E) runs north of 20. It’s 18 right now, on the consensus estimate on next year’s earnings. So on a valuation basis, there’s room. This doesn’t take into account a corporate tax cut that will take the rate from 35% to 20%. That goes right to the bottom line for companies (earnings go UP). When earnings go up, the multiple stocks trade for goes down (stocks get cheaper).

Citibank thinks each 1% cut in corporate taxes will add roughly $2 in S&P 500 earnings. And Citibank says the effective tax rate across the S&P 500 is more like 27%. So a cut to 20% would mean a seven percentage point reduction. This would put next year’s S&P 500 earnings in the mid-$150s, which would put the multiple at 16 to 17 times next year’s earnings.

And don’t forget, we’re getting fiscal stimulus for a reason: to pop economic growth, which has been in a rut (post-crisis), running well south of the 3% long run average growth rate for the economy. The prospects for better growth, means prospects for better earnings. The outlook for better earnings, on a better economy, should also put downward pressure on valuations, making stocks more attractively valued.

In my January 2 note, I said: “there will be profound differences in the world this year, with the inauguration of a new, pro-growth U.S. president, at a time where the world desperately needs growth.” I think it’s safe to say that is playing out—albeit maybe slower and messier than expected.

I also said: “The element that economists and analysts can’t predict, and can’t quantify, is the return of ‘animal spirits.’ This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mistrust of the system. All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset appears to finally be underway. And that gives way to a return of animal spirits, which haven’t been calibrated in all of the forecasts for 2017 and beyond.”

The adoration for Bitcoin has been growing by the day, though no one understands how to value it.

CNBC went on “watch” the other day for Bitcoin $10,000. Today it traded above $11,000 and then fell as much as 21% from the highs.

Here’s a look at the chart.

I heard someone today say, everyone should have a small portion of their net worth in Bitcoin. That sounds an awful lot like the mantra for gold. Gold has been sold all along as an inflation hedge. But unless you have Weimar Republic-like hyperinflation, you’re unlikely to get the inflation-hedge value out owning it.

Remember, gold went on a tear from sub-$700 to above $1,900 following the onset of global QE (led by the Fed). Gold ran up as high as 182%. That was pricing in 41% annualized inflation at one point (as a dollar for dollar hedge). Of course, inflation didn’t comply. Still, nine years after the Fed’s first round of QE and massive global responses, we’ve been able to muster just a little better than 1% annualized inflation. So gold is a speculative trade. It’s a fear trade. And it’s volatile.

If you bought gold at the top in 2011, the value of your “investment” was cut in half just four years later. That’s a lot of risk to take for the prospect of “hedging” against the loss of purchasing power in the paper money in your wallet.

Now, Bitcoin is becoming a pretty polarizing “asset class.” The gold bugs get very emotional if you argue against the value of owning gold. Those that own Bitcoin seem to have a similar reaction. But Bitcoin, like gold, is a tough one to value. You buy it because you hope someone is going to buy it from you at a higher price.

So is Bitcoin (cryptocurrencies) an investment? Sophisticated investors that are involved, likely see it as similar investment to a startup. It has traction. It has a lot of risks. It could go to zero. Or it could pay them multiples of what they pay for it. But they thrive on diversification. When they have a large portfolio of these types of bets, when a few payoff, they put up nice returns. Bitcoin may be one of the few, or it may not.

Stocks continue to rise today, up another 1% on the Dow. So year-to-date, the Dow is up 20% now, the S&P 500 is up 17% and the Russell 2000 is up 13%. Remember, most of Wall Street was expecting 3%-4% returns for stocks this year.

What did they miss? Mostly the rise in optimism surrounding the incoming pro-growth government.

With consumer and corporate balance sheets as good as we’ve seen in a long time, unemployment at 4.1% and corporate earnings growing at a 10% clip through the first three quarters, and tax cuts coming, we should expect almost everything to go up.

As for tax cuts, that got a step closer today, as it was approved by the Senate budget committee. Now it goes to a vote on the floor of the Senate.

All of this, and market interest rates are going nowhere. The 10-year yield, at 2.33%, is just about where we started the year. That’s, in part, being weighed down by some comments by incoming Fed Chair Jerome Powell.

Today, Powell gave prepared remarks and took questions for his confirmation hearing with the Senate today. The general view has been that Powell is a like-thinker to Yellen, but with partisan alignment for the president.

But under Yellen’s leadership at the Fed, the overly optimistic forecasts about inflation and the rate path affected consumer behaviors and nearly stalled the recovery last year. They had to reverse course on their projections and game plan early in 2016. And then we had the election, and the prospects of fiscal stimulus, and the Fed (under Yellen) went back to the script of telegraphing a more restrictive rate environment.

Now, with that in mind, I thought early on that Trump would show Yellen the door. And I expected him to appoint a new Fed Chair that was a clear dove–someone that would leave rates alone (given the weak inflation) and let fiscal stimulus feed into the recovering economy, to finally fuel some animal spirits. Do no harm to the economy. Even Bernanke suggested the Fed should let the economy run hot, warning not to kill the recovery by setting expectations for tighter credit coming down the pike.

From Powell’s comments today, it sounds like we may be getting less Yellen than people have believed. In his short prepared remarks, he made an effort to say he strives to support the economy’s progress toward full recovery. He implied the job market needs more improvement, and that he favors easing the regulatory burden on banks. This doesn’t sound like a guy that thinks the economy can withstand mechanically stepping rates higher in the face of weak inflation and sub-trend growth.