Yesterday we looked at this chart of the S&P 500 …

In discussing this chart, I made an error. The blue line, of course, represents what the S&P 500 would have looked like had it continued its long-run annualized growth rate of 8% from the 2007 (pre-crisis) peak. That gives us perspective on where we stand in this stock market recovery. Even though we’re up more than four-fold from the 2009 bottom, and people continue to talk about how long this bull market has run, we still have not recovered the lost growth of the past decade.

That is clearly displayed in the gap between the orange line (the actual S&P 500) and the blue line (where stocks would be had we continued along the 8% annualized path).

What can we attribute this gap to? Post-recession recoveries are typically driven by an aggressive bounce-back in growth. We didn’t get it. Instead, the post-recession growth environment of the past decade was dangerously shallow and slow.

Why? The Fed and other major central banks were the only game in town for the global economy over the past decade. They saved the world from a total collapse, staved off further shocks along the way, and they manufactured a recovery. But the “easy money” solution doesn’t work the same in the depths and aftermath of a global debt bust, as it does in normal recessions. The central banks could only muster stall-speed growth.

That’s why the election was so important. It has resulted in the great hand-off, from a global economy that was just surviving on the life-support of central banks, to a global economy that has the chance to thrive on the catalyst of fiscal stimulus, and become sustainable from structural reform.

With that, we should expect the gap in the chart above to close. That argues for much higher stock prices, and a continuation of this bull market.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

With the S&P 500 finally returning to new record highs today, fully recovering the price correction this year, let’s take a look back at the correction, and where stocks can go from here.

As I said in my January 30 note “experience tells us that markets don’t go in a straight line. And with that, we should expect to have dips along the way for this bull market. Since 1946, the S&P 500 has had a 10% decline about once a year on average. A correction here would be healthy and would set the table for hotter earnings and hotter economic growth (coming down the pike) to ultimately drive the remainder of stock returns for the year.”

Fast forward eight months, and we’ve now had a 12% correction. And we’ve since had back-to-back quarters of 20%+ earnings growth, with an economy that is finally growing at better than 3% four-quarter average annualized growth.

Meanwhile, stocks remain cheap. The 10-year yield is still under 3%. And historically, when rates are low (sub 3% is still VERY low), stocks tend to trade north of 20 times earnings. The forward P/E on stocks at the moment is just 17. If we apply a 20x multiple to $170 in forward S&O 500 earnings, we get 3,400 in the S&P. That’s 19% higher.

With that in mind, let’s also revisit my chart on the long term growth rate of the S&P 500.

In the orange line, you can see what the S&P 500 looks like growing at 8% annualized (the long-run average growth rate) from the pre-crisis peak in 2007. This is where stocks should have gone, absent the near global economic apocalypse. And you can see the actual path for stocks in the blue line.

Bottom line: Despite the nice run we’ve had in stocks, off the bottom in 2009, we still have a big gap to make up (the difference between the blue line and the orange line). This is the lost decade for stocks.

This argues for another 28% higher in stocks to fill that gap.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

As we discussed on Friday, with China coming back to the negotiating table on trade, we have a signal that the trade dispute smoke will not end in fire.

That is unlocking this rotation we’ve been talking about for the past month or so, where the money that has been plowed into the stocks of the very hot tech giants, starts moving out and into the lagging blue chips.

With that, as we sit eight months into the year, with the winds of fiscal stimulus in our sails, the S&P 500 is just now close to recovering the losses from the January highs.

And the Dow remains, 3.2% off of the January highs (which were record highs). But I suspect we will now close that gap quickly.

Remember, we have two very hot earnings quarters under our belt, and building momentum in the economic data, as fuel for stocks. And I suspect the China news, to break the stalemate on trade negotiations, will also fuel the resumption of the young bull market in commodities, which should offer very attractive investing outcomes in the coming months.

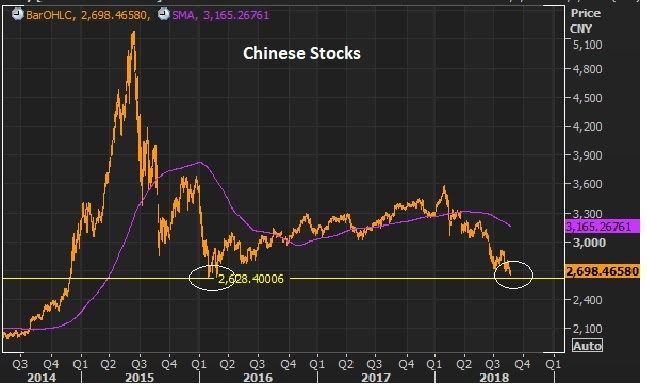

Maybe the best signal for commodities is this chart on Chinese stocks, which looks like it may have bottomed TODAY into these 2016 lows (circled).

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Back in July, we talked about the significance of the President of the European Commission coming to Washington to make a deal on trade. That was a big day for Trump’s fight to level the playing field on global trade.

Why? Because concessions out of Europe paved the way to more concessions globally.

That’s what we’re getting. Fast forward a little less than a month and now we have China (the center of the global trade dispute universe) coming back to the table on trade negotiations with the U.S.

This is what happens when you negotiate from a position of strength. Trump has the leverage of a strong economy, and the credibility to act on tough threats. And that is bringing about progress. Trading partners risk being left behind in the global economic recovery if they don’t play ball.

So we should expect “movement” from China. And movement equals success.

With that, as I said, I suspect that will be the catalyst to get stocks back on the path toward double-digit gains by year-end.

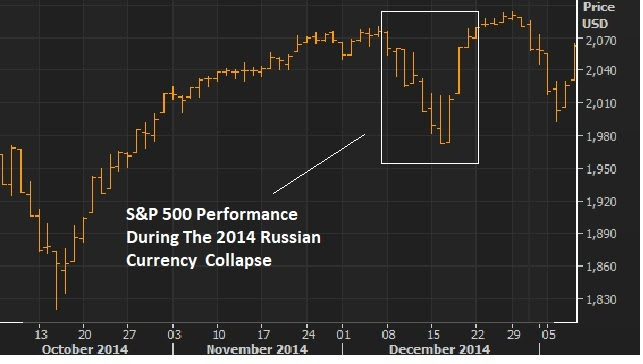

On Tuesday, we looked at the similarities between the recent currency collapse in Turkey, and the 2014 collapse of the Russian ruble.

And we looked at this chart of how the S&P 500 behaved back in 2014.

The S&P 500 is the proxy on global market stability. And stocks were shaken on Russia back in 2014. When the ruble collapsed, U.S. stocks lost 5% of its value in just 7 days.

But the decline was fully recovered in just 3 days.

Given the similarities of these two currency crises (a currency attack on a bad behaving leader), I thought we might see the same behavior in stocks this time. And that’s what we appear to be getting – a shallower decline but a swift recovery.

So, why the quick recovery?

As we also discussed on Tuesday, while the Turkish lira has been the center of attention in the financial media, the real reason global markets were shaking had more to do with China.

If a currency crisis that started in Turkey ended in China, there would be big geopolitical fallout.

As we’ve discussed over the past month, the biggest risk from China is a big one-off devaluation. That would stir up a response from other big trading partners (i.e. Europe and Japan), where they would likely coordinate to blocktrade from China all together. That’s where things would get very ugly and likely (ultimately) culminate in a military war.

But the probability of that outcome was reduced yesterday. We had news that a China delegation would travel to the U.S. to re-open trade negotiations. They’re coming back to the table.

So we should expect concessions from China. That’s good news for the globlal economy and for global stability. And that news drove the big bounce in stocks yesterday, which continued today. I suspect this will be the catalyst to get stocks back on the path toward a double-digit gains by year-end.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We talked yesterday about the sharp currency devaluation in Turkey over the past few days. The Lira bounced aggressively today, which soothes some fears in global markets.

As I said, many have made comparisons to the Asian currency crisis of the late 90s, and have speculated on the potential for the events in Turkey to ultimately destabilize global markets. But as we discussed yesterday, this looks more like the 2014 currency attack on the Russian ruble — a geopolitically-driven crippling of an economy with bad behaving leadership.

With that in mind, here’s what happened to U.S. stocks back in 2014, when the ruble lost 5% of its value (vs the dollar) in just 7 days. But the decline was fully recovered in just 3 days.

U.S. stocks have been the proxy for global market stability throughout the past decade (the crisis and post-crisis era). So, for perspective on just how shaky the Turkey influence is being perceived, the S&P 500 sits just one percent off of all-time highs at today’s close.

Remember, the ECB stands ready to plug any holes necessary in European bank exposure to Turkish debt. That euro-denominated debt has been the risk people immediately homed in on.

The real question is, will this (currency crisis) ultimately end in China, with a revaluation of the yuan, or perhaps a free-floating yuan?

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Last week Larry Kudlow, the White House Chief Economic Advisor, hinted that Jean-Claude Juncker (head of European Commission) would be coming to Washington with some concessions on trade.

As I write, we’ve yet to hear the results of the Trump/Juncker meeting today, but this could be a major turning point in the perception of the U.S. trade offensive. Movement equals success. And in that case, concessions out of Europe may pave the way to more concessions globally. That signal could trigger a big rally in global markets.

One particular market to watch is copper. Copper is the first place you should look if you think the world is escaping the slugglish post-crisis growth period, and possibly entering an economic boom period. It has been sensitive to the global trade disputes. A clearing of that, would resume what should be a multi-year bull market in copper.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

As we head into the long holiday weekend, let’s look at some key charts.

First, just a week ago, the U.S. interest rate market was spooking investors, as 10-year yields were hanging around 3.10%. The fear was, would 3% yields quickly turn into 4% yields, and hit economic activity.

As of today, we’re trading closer to 2.90% again, back below 3%.

But you can see, we run into this big trendline that represents this ascent in rates for 2018, which also reflects the outlook of a hotter economy, thanks to tax cuts (fiscal stimulus).

Bottom line here: The concern in interest rates is speed, not trajectory. The trajectory should continue to be UP, which is a signal that the economy is improving, and finally gaining the tracking to perform at trend, if not better than trend growth. The concern about ‘speed’ should be far less than it was a week ago.

Next, here’s a look at the S&P 500.

You can see in the chart above, we’ve broken the downtrend of this correction cycle. The longer-term trend is UP. And this bull trend started, not coincidentally, at the bottom of the oil price crash in 2016, when global central banks stepped in with measures to stem the slide in confidence.

So, we’ve had a healthy 12% correction in stocks, we’ve held the 200-day moving average, we’ve maintained the longer-term trend, and we’ve broken out of the downtrend of the correction. Small cap stocks have already returned to new record highs. And we have an economy on pace to grow at 3% this year or better, with corporate earnings expected to grow at 20% for the year. So, the second half of the year should be very good for stocks.

There has been a lot of attention over the past couple of days on China and trade relations.

China has moved down tariffs on auto and auto parts imports. And a source today said the government has “encouraged” China’s largest oil refiner to buy more U.S. crude oil. Based on the reports, China is now taking about 8 times the daily volume of U.S. crude imports, compared to averages a few months ago.

These are concessions! This is a distinct power shift. Not long ago, the world was afraid to rattle the cage of China. They (global trading partners) tiptoed around touchy matters like Chinese currency manipulation prior to the global financial crisis a decade ago, and even more so after the crisis.

But now, you can see the leverage that has been created by Trump. This is exactly what we talked about the day after the election.

Here’s an excerpt from my November 9, 2016 ProPerspectives note, back when the experts were predicting Draconian outcomes for poking the China giant: “As we’ve seen with Grexit and Brexit, the votes came with dire warnings, but have resulted in creating leverage. Trump’s complaints about China are right. And a threat of slapping a tariff on Chinese goods creates leverage from which to negotiate.”

Now, we have an economy that is leading the global economic recovery. China wants and needs to be part of it. And we have a President that has a loud bark, and the credibility to bite. And that is creating movement. Let’s revisit, also from one of my 2016 notes, why this China negotiation is so important …

TUESDAY, SEPTEMBER 27, 2016

China’s biggest and most effective tool is and always has been its currency. China ascended to the second largest economy in the world over the past two decades by massively devaluing its currency, and then pegging it at ultra-cheap levels.

Take a look at this chart …

In this chart, the rising line represents a weaker Chinese yuan and a stronger U.S. dollar. You can see from the early 1980s to the mid-1990s, the value of the yuan declined dramatically, an 82% decline against the dollar. China trashed its currency for economic advantage—and it worked, big time. And it worked because the rest of the world stood by and let it happen.

For the next decade, the Chinese pegged its currency against the dollar at 8.29 yuan per dollar (a dollar buys 8.29 yuan).

With the massive devaluation of the 1980s into the early 1990s, and then the peg through 2005, the Chinese economy exploded in size. It enabled China to corner the world’s export market, and suck jobs and foreign currency out of the developed world. This is precisely what Donald Trumpis alluding to when he says ‘China is stealing from us.’

China’s economy went from $350 billion to $3.5 trillion through 2005, making it the third largest economy in the world.

This next chart is U.S. GDP during the same period. You can see the incredible ground gained by the Chinese on the U.S. through this period of mass currency manipulation.

And because they’ve undercut the world on price, they’ve become the world’s Wal-Mart (sellers to everyone) and have accumulated a mountain for foreign currency as a result. China is the holder of the largest foreign currency reserves in the world, at more than $3 trillion dollars (mostly U.S. dollars). What do they do with those dollars? They buy U.S. Treasurys, keeping rates low, so that U.S. consumers can borrow cheap and buy more of their goods—adding to their mountain of currency reserves, adding to their wealth and depleting the U.S. of wealth (and the cycle continues).

This is the recipe for big trade imbalances — lopsided economies too dependent upon either exports or imports. And it’s the recipe for more cycles of booms and busts … and with greater frequency.”

Again, China has to be dealt with. And we’re starting to see signs of progress on that front. Good news.

The move in the 10-year yield was the story of the day today. Yields broke back above 3% mark, and moved to a new seven-year high.

That fueled a rally in the dollar. And it put pressure on stocks, for the day.

We’re starting to see more economic data roll in, which should continue building the story of a hotter global economy. And it’s often said that the bond market is smarter than the stock market. There’s probably a good signal to be taken from the bond market that has pushed the 10-year yield back to 3% and beyond (today). It’s a story of better growth and growing price pressures, which finally represents confidence and demand in the economy.

From a data standpoint, we’re already seeing early indications that fiscal stimulus may be catapulting the economy out of the rut of the sub-2% growth and deflationary pressures that we dealt with for the decade following the financial crisis. We’ve had a huge Q1 earnings season. We’ve had a positive surprise in the Q1 growth number. The euro zone economy is growing at 2.5% year-over-year, holding toward the highest levels since the financial crisis. And we’ll get Q1 GDP from Japan tonight.

Another key pillar of Trumponomics has been deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more by regulation than Wall Street. And under the Trump administration, those regulations are getting slashed.

Among the most damaging for big money center banks has been the banning of proprietary trading. That’s a huge driver of bank profitability that has been gone now for the past eight years. But it looks like it’s coming back. Bloomberg reported this morning that the rewrite of the Volcker Rule would drop the language that has kept the banks from short term trading.

That should create better liquidity in markets (less violent swings). And it should drive better profitability in banks. Will it lead to another financial crisis? For my take on that, here’s a link to my piece from last year: The Real Cause Of The Financial Crisis.