|

|

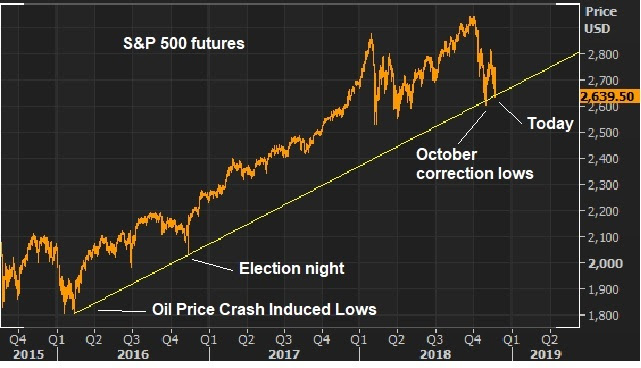

November 30, 5:00 pm EST As we close the week and month, let’s take a look at some key charts. Stocks have now bounced 5% since last Friday. And that bounce was technically supported by this big long-term trendline we’ve been watching … |

|

|

And, as of this week, stocks now have the additional fuel of a more stable outlook for interest rates. |

|

|

The surge above 3% on the ten-year yield sustained that level, even in the face of a stock market decline. That signal created fears that the Fed might be on course to choke-off economic momentum. But that has now been quelled by the Fed’s clear signal this week that they are near the end of their rate normalization program. The 10-year ends the week well off the highs of the past two months, and at the important 3% level. The dramatic adjustment lower in oil prices should also be additional fuel for stocks … |

|

|

An overhang of risk to global markets has been the potential for sanctions on the Saudi government. But the issue seems to be now settled, with the sanctioning of Saudi individuals which do NOT include the Saudi Crown Prince and/or government. And as we’ve discussed, Trump has used the leverage over the Saudi Crown Prince to influence oil prices lower (for the moment). With that above in mind, stocks finish the week well bid. If we can get at least a standstill agreement on the U.S./China trade war from this weekends meetings between Presidents Trump and Xi, that may be enough to fuel a melt-UP to new highs on stocks by the end of December. It may be time for Trump to get a deal done, and solidify economic momentum to get him to a second term, where he may then re-address the more difficult structural issues with China/U.S. relations. What stocks do you buy? Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

|

November 28, 5:00 pm EST Yesterday we talked about the perfect setup, coming into today’s scheduled speech by the Fed Chair, for Powell to signal a pause in the Fed’s rate normalization program. The sharp fall in oil prices in the past two months has taken some of the edge off of inflation concerns. And there has already been evidence that the speed at which rates have moved has caused a slowdown in housing. So this was the perfect opportunity for the Fed Chair to give a clear signal that they are near the end on rate normalization. Indeed, that’s what we got. And that did indeed provide a positive catalyst for stocks, and I suspect it will be a positive catalyst for what has been some deterioration of confidence in the economic outlook. That all aligns nicely with the technical picture we’ve been watching in stocks. Here’s another look at the bounce off of this big trendline for stocks, that continues to grow in scale. |

|

|

So this adjustment in the market’s perception on the interest rate outlook is a catalyst for what could be a very aggressive rebound in stocks into the year end. More fuel would be a positive outcome from the Trump/Xi meetings on U.S./China trade, which will come toward the end of the week. With the above in mind, among the biggest rebounds in global markets should be emerging markets. |

|

|

As of last month, the MSCI Emerging Markets Index was down 27% from the January highs.

What stocks do you buy? Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

November 27, 5:00 pm EST

Earlier this month, we talked about the big fall in oil prices.

If we look back over the past five years, the magnitude of that move is only matched (or exceeded) in cases where there was significant manipulation in the oil market and/or a systemically threatening oil price crash.

As we’ve discussed, the pressure on oil this time around seems to be about manipulation — and appears to have everything to do with Trump’s leverage over the Saudis (related to sanctioning the Kingdom over the Khashoggi murder).

But we’ve now traded down to the important $50 mark. That’s 35% from the highs of just October 3. And this is an inflection point where it could go bad, but it also could present a goldilocks scenario (a level that’s just right for the U.S. economy).

Sure, cheap oil is good for consumers. You save a few extra bucks at the pump. But in the current environment, it presents risks to the financial system. The shale industry’s break-even point on producing oil is said to be $50. Below that, they dial down production, lay off workers, stop investing and quickly become a default risk to their creditors (U.S. and global banks). We saw it back in 2016. The same can be said for those countries heavily dependent on oil revenues (i.e. they become default risks as oil prices move lower).

That’s the bad side. The good side to the oil price slide? As we’ve discussed, it should relieve some pressure on the Fed. The Fed likes totalk about their inflation readings excluding effects of volatile oil prices. But they have a record of acting on monetary policy when oil is moving.

The bottom line: Oil plays a big role in their view on inflation. And given the quick drop in oil prices, the Fed’s concerns about inflation should be cooling. Again, this opens up the door for the Fed Chair, tomorrow, to take the opportunity in a prepared speech at the Economic Club of New York, to signal a pause coming in the Fed’s rate normalization program. That would be a positive catalyst for economic and market confidence.

|

November 26, 5:00 pm EST After a down 7% October, the S&P 500 was down another 3% for November as we started the week. But stocks had a nice day, continuing to bounce from this big trendline we’ve been watching over the past week. |

|

|

And the better news: We have potential positive catalysts on the docket for this week that could put a final stamp on this correction. Powell (Fed Chair) gives a prepared speech on Wednesday at the Economic Club of New York. Remember, we were looking for some signal a couple of weeks ago that the Fed might take a pause normalizing rates. We got it, but from the Atlanta Fed President. This week, any indication from the Fed Chair that rate hikes are nearing an end would be a greenlight for stocks. And then we get new information on U.S./China trade relations by the week’s end as Trump and Xi are scheduled for a sit down at the G20 meetings. Among all of the concerns that might be curbing risk appetite (both in markets and the economy) this one is among the biggest. Progress on that front should also trigger relief in stocks. The combination of a more dovish Fed and some clarity on trade would set up for what could be a very aggressive bounce for stocks into the year end. What stocks do you buy? Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

|

November 20, 5:00 pm EST Stocks hit this big trendline today and bounced. |

|

|

This line comes in from the oil price crash-induced lows of 2016. And, as you can see, we have the bottom of the fallout in the futures market on election night, and the lows of last month. This area also puts the S&P 500 right at a 10% decline from the October highs. Is it the bottom of this sharp two-day slide? Maybe. Let’s talk about why stocks have gotten hit, again, this week. Last week, it looked like the fog had lifted. We were looking for the Fed to signal a pause on rates. We got it, to a degree, with the message that the ‘normalization phase’ for rates was in the “final days.” We had the U.S. Treasury name those Saudis to be sanctioned in the Khashoggi murder. The Crown Prince wasn’t one of them – which means the Kingdom was not being sanctioned. And we had news that progress was being made on U.S. China trade. That was all good news for stocks. But the latter two of these hurdles for stocks was reversed over the weekend. We had some confrontational talk from Pence and Xi. And we had news that the CIA investigation would implicate the Crown Prince in the murder of Khashoggi. Everyone is well aware of the U.S./China trade implications. As for the Saudi, implications, it’s more complicated. First, Trump has been trying to make the case for Saudi Arabia’s critical alliance in the fight to defeat ISIS and check of Iran. Maybe more importantly, pushing Saudi Arabia toward an alignment with China and Russia in the long-game would be a grave danger for the U.S. Taking action against the Crown Prince would jeopardize both. So, as I suggested earlier in the month, Trump seems to be leveraging the Saudi crisis to get oil prices lower. He said as much today. And to this point, it appears that he’s settled on the sanctions that have already been levied. If that holds, that’s good for stocks. The risk, given the amount of wealth Saudi Arabia has in U.S. capital markets, is any change in that stance that might mean broad sanctions on the Kingdom of Saudi Arabia. That’s where Saudi liquidations, in effort to secure assets, is dangerous for the stock market. Join me here to get all of my in-depth analysis on the big picture, and to get access to my carefully curated list of “stocks to buy” now.

|

|

|

November 14, 5:00 pm EST Later today Fed Chair Powell will be speaking at a Dallas Fed event. We’ve talked over the past two days about the potential for Powell to use this opportunity to dial down expectations of a December rate hike. Overnight, Japan reported a contraction in their economy for the third quarter. And this morning Germany’s GDP report showed the first contraction in more than three years. Meanwhile, U.S. core CPI came in softer than expected this morning. And the headline number will be hit, in the next reading, by a 28% plunge in oil prices. Add this to the outlook for gridlock in Washington on any further pro-growth policy-making, and Powell has the perfect excuse to start telegraphing a pause on rate hikes. If he does, expect stocks to respond very favorably. We will see. He speaks at 6:05pm EST. Here’s a look at stocks and the decline of the past month, as we head into this Fed discussion on the economy … |

|

|

Technically, today the S&P and the Dow both hit a big retracement level and bounced aggressively. This sets up nicely for the Fed discussion.

Join me here to get all of my in-depth analysis on the big picture, and to get access to my carefully curated list of “stocks to buy” now.

|

November 13, 5:00 pm EST

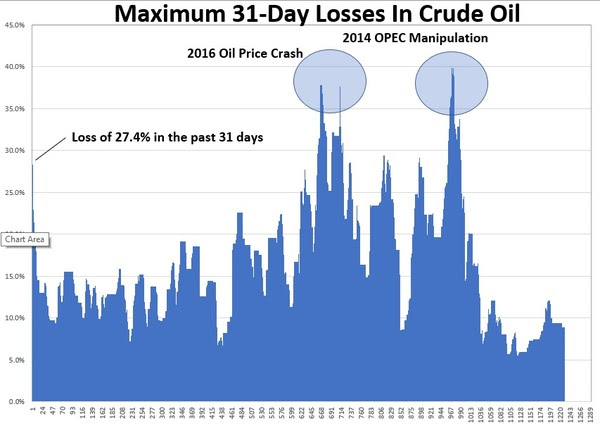

In the past two notes, I’ve focused on oil. And that does indeed seem to be the tail that is wagging the global markets dog.

Oil lost another 8% today. Over the past 31 days, crude prices have dropped 27%.

If we look back over the past five years, the magnitude of that move is only matched (or exceeded) in cases where there was significant manipulation in the oil market and/or a systemically threatening oil price crash.

You can see in the chart above, we’ve dropped 27% over the past 31 days. The other big drops in crude were in February of 2016 (the crash) and in November of 2014 (OPEC’s refusal to cut oil production).

Interestingly, these historic crude price declines were occurring as the Fed was preparing markets for the beginning of its normalization campaign (i.e. moving rates away from the emergency zero interest rate level). And it was these price declines that threw a wrench in those plans.

Despite what the central bankers say, oil prices have a big influence on their read on inflation. Lower oil prices put downward pressure on inflation. And as oil prices were plunging from 2014 through 2016, the Fed clearly and dramatically held back on their rate hiking plans.

On that note, remember yesterday we talked about the prospects that Powell (Fed Chair) may use the opportunity to dial down expectations of a December rate hike, if we see some soft data this week (growth data from Japan and Europe and inflation data from U.S., Europe and UK). We now have a big haircut on oil prices to factor into the inflation data. That too, may give him the excuse to pause on rates. We’ll hear from him tomorrow at a Dallas Fed meeting.

November 12, 5:00 pm EST

Stocks continue to swing around following last weeks midterm elections. Perhaps it has something to do with the uncertain outcome that remains in Florida, given the role Florida will play in the 2020 Presidential election. Perhaps it has something to do with the continuation of the unraveling of the tech giants.

Maybe more importantly, we head into a week with key inflation data hitting for the U.S., Europe and the UK. And we have Q3 GDP numbers coming from Japan and Europe. The Japanese economy is expected to have contracted last quarter.

Slowing numbers in Japan and Europe, along with some tame inflation data might give the Fed Chair (Powell) an excuse to dial down expectations of a December Fed hike. He is scheduled to speak Wednesday afternoon at a Dallas Fed event.

With the idea that the new divided Congress will put the brakes on any new pro-growth economic policies, Powell may be looking for the excuse to slow the pace that rates are rising. That would be a huge catalyst for stocks.