One of the best investors on the planet, David Tepper, was on CNBC this morning. Let’s talk about how he sees the world and how he is positioned.

What I appreciate about Tepper: He’s a common sense guy.

And his common sense view of the world happens to be in alignment with the view and themes we discuss here every day. So he agrees with me – another thing I appreciate about him.

As you know, Wall Street and the media are always good at overcomplicating the investment environment with their day-to-day hyper analysis. Because of that, they tend to forge a path that moves further and further away from the simple realities of the big picture. That’s actually good. Because it creates opportunity for those that can avoid those distractions.

Right now, as we’ve discussed, the big picture is straight forward. We have a President that wants deregulation, tax cuts and a big infrastructure spend. And we have a Congress in place that can approve it. And this all comes at a time when the world has been in a decade long economic slog following the global financial crisis – in desperate need of growth. With that, we have a Fed that still has rates at very, very low levels. And the ECB and BOJ are still priming the pump with QE.

This is precisely Tepper’s view. He says the bowl is still full, i.e. the stimulus from the monetary policy side is still full, and now we get stimulus coming in from the fiscal side. What more could you ask for (my words) to pump up growth and asset prices, which will likely spill over into a pop in global growth. Still, people are underestimating it. And as he says, the Fed is underestimating it.

Are there risks? Yes. But the probability of growth, with the above in mind, well outweighs the probable downside scenarios. What about execution risk? Even if tax reform and infrastructure are slow to come, Tepper says deregulation is a done deal. It drives earnings and “animal spirits.”

He likes stocks. He likes European stocks. And I think he really likes Japanese stocks, but he stopped short of talking about it (my deduction).

Among the risks: Inflation picking up too fast, which would require the Fed to move faster, which could choke off growth (undo or neutralize fiscal stimulus).

This is why, among other reasons, Tepper’s favorite trade is short bonds. – i.e. higher interest rates. If he’s right and economic growth has a big pop, he wins. If the risk of hotter inflation materializes and rates move faster, he wins.

For context, this is the guy that literally changed global investing sentiment in late 2010 when he sat in front of a camera on CNBC, in a rare high profile TV interview (maybe first), when investing sentiment was all but destroyed by the global financial crisis and the various landmines that kept popping up. Tepper said in a very confident voice that the Fed, by telegraphing a second round of QE, had just given us all a free put on stocks (i.e. the Fed is protected the downside, it’s a greenlight to buy stocks). For all of the market jockeys that were constantly focusing on the many problems in the world, that commentary from Tepper, for some reason, woke them up.

For perspective on Tepper: Here’s a guy that is probably the best investor in the modern era. He’s returned between 35%-40% annualized (before fees) for more than 20 years. He made $7.5 billion in 2009 betting on financial stocks that most people thought were going bankrupt. And he was telling everyone that what the Fed is doing will make ‘everything’ go up. It sparked, in 2010, what is known as the “Tepper rally” in stocks.

When Tepper speaks it’s often smart to listen. And he likes the Trump effect!

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

As we discussed last week, the Presidential address to the joint sessions of Congress last night was a big market event. And as I discussed yesterday, growth and fiscal stimulus needed to be moved to the front burner of the daily narrative. The President delivered last night.

After he began speaking, one of the early headlines on my Reuters feed last night: TRUMP SAYS HE WILL BE ASKING CONGRESS TO APPROVE LEGISLATION THAT PRODUCES $1 TRILLION INVESTING IN INFRASTRUCTURE FINANCED THROUGH BOTH PUBLIC AND PRIVATE CAPITAL.

Bingo! There’s a lot of talk about the inspiration of the speech, but growth is king in this environment, after 10 years of malaise and no improvement in sight. And the focus has shifted to growth. Stocks have had a huge day. Meanwhile, yields have been up but relatively tame. Gold has been down, but relatively tame. And the dollar has been up, but relatively tame.

German 2 year yields, which have been the sour spot, as they’ve slipped toward -1% in the past week, were up bouncing nicely today.

It’s not uncommon to see big global market participants ignore all else in key market moments, and just focus on one spot. That has been the case. And that spot is the stock market. The U.S. stock market is where the impact of a trillion dollar infrastructure spend, a massive tax cut, and broad deregulation can be most directly influenced and, as importantly, stocks are capable to absorbing large, large amounts of capital.

Now, it’s time to revisit some great catch up trades I’ve discussed for a while: German and Japanese stocks. A better U.S. is better for everyone, make no mistake. Hotter growth here, will mean hotter global growth, and it gives Europe and Japan a shot at recovery, especially with their central banks priming the pump with big QE, still.

On that note, let’s take a look at the charts …

So you can see the same period here for U.S., German and Japanese stocks, dating back to 2012, when the European Central Bank stepped in with intervention in the European sovereign bond market (at least promised to do so), that turned global economic sentiment and then then Japan came in months later with promises of a huge stimulus program. All stocks went up.

But you can see, stocks in Europe and Japan have yet to regain highs of 2015, after the oil price crash induced correction.

These stock markets look like a big catch up trade is coming, and it may be quick, following the catalyst of last nights U.S. Presidential address.

Follow The Lead Of Great Investors Like Warren Buffett In Our Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

Stocks finished the week on record highs. We talked earlier in the week about Trump’s meeting with Japan’s Prime Minister and his economic and finance advisors.

I suspect that Trump will come away, after a weekend in Palm Beach with Abe, learning that Abenomics is good for the U.S., and good global growth and stability (in the current global economic environment).

And one of the keys to success in Abenomics is a weaker yen, which translates to a stronger dollar. As I’ve said, the weak yen has been pulled into the fray with Trump’s tough talk on trade imbalances, but his beef on currency advantage is really directed toward China – not Japan, not Mexico, not even Europe.

With that, and with the assumption that the yen may be pardoned for a while, the dollar bouncing against the yen as we head into the weekend. And it looks like we may see a technical breakout and an even higher dollar, lower yen in our future.

And Japanese stocks look set to break out too, to catch up to the strength of U.S. stocks. The Nikkei is 8% off of the 2015 highs, while U.S. stocks are on record highs, and 8% ABOVE its 2015 highs.

Another catch up trade: German stocks. Despite the growing attention given to the French nationalist candidate, Le Pen, who has been anti-euro and anti-European Union, right or wrong the bond market isn’t showing any new interest in disaster insurance in Europe, nor is the euro.

With that, German stocks look very good, still about 8% from the 2015 highs, and the technical correction clearly ended last summer.

Lastly, let’s take a look at another big sleeper stock market, China…

You can see how Copper is on a big run (up 10% ytd). That typically correlates well with expectations of global growth. Global growth is typically good for China. Of course, China is in the crosshairs of Trump’s fair trade movement, but if you think there’s a chance that more fair trade terms can be a win for the U.S. and a win for China, then Chinese stocks are a bargain here.

Have a great weekend!

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We’ve talked about the drift (now slide) lower in interest rates over the past couple of days. This is a big deal and something to keep a close eye on. Remember, this move lower comes in the face of a strong jobs number on Friday. Following that number, the yield on the 10-year traded up to 2.50%. Today we’re looking at 2.35% (low of 2.32%).

In contrast to this move in rates, stocks are sitting on record highs, if not making new record highs. Oil has been stable in a $50-$55 range. The dollar isn’t doing much. Implied volatility on the stock market is dead. And commodities are relatively quiet, except for gold.

On that note, yesterday we looked at the tight correlation of the inverse price of gold and yields since the election (i.e. gold goes up, yields go down). And in recent weeks, yields have been lagging the strength in gold, making the case for even lower yields to come.

We looked at the below trendline on the 10-year yesterday that was testing… that gave way today.

This move lower in yields puts both the Trump administration and the Fed in a much more comfortable spot.

A continued rise in market interest rates would force the Fed to be more aggressive, both of which would work against fiscal stimulus, dulling the contribution to growth, if not neutralizing it all together. Higher rates would slow the housing market and slow spending, especially in a fragile economy. Among the things to be worried about, higher rates, too soon, could be the biggest (bigger than protectionism, European elections…)

President Trump was said to be asking for advice on the administration’s view on the dollar overnight. I suspect the upcoming meeting with Japan’s Prime Minister (and co.) had something (a lot) to do with it. This is precisely what we’ve been talking about. The dollar and the yen are squarely in the crosshairs for this face-to-face meeting. But Trump may learn from the meeting that he would far prefer a stronger dollar and weaker yen, than a 4-4.5% ten year yield by the end of the year.

As I’ve said, Japan’s QE policies, which weaken the yen, also offer an anchor to U.S. interest rates, keeping them in check. I suspect the softening of U.S. yields, as all other markets are quiet, may have something to do with Chinese money leaving China (as we discussed yesterday). But it also may be influenced by Japan, finding the best, safest parking place for freshly printed money (i.e. buying U.S. Treasuries, which pushed down U.S. rates) – and showing that benefits of that influence to the new President.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Yesterday we looked at the slide in yields (U.S. market interest rates — the 10-year Treasury yield). That continued today, in a relatively quiet market.

Let’s take a look at what may be driving it.

If you take a look at the chart below, you can see the moves in yields and gold have been tightly correlated since election night: gold down, yields up.

As markets began pricing in a wave of U.S. growth policies, in a world where negative interest rates were beginning to emerge, the benchmark market-interest-rate in the U.S. shot up and global interest rates followed. The German 10-year yield swung from negative territory back into positive territory. Even Japan, the leader of global negative interest rate policy early last year, had a big reversal back into positive territory.

And as growth prospects returned, people dumped gold. And as you can see in the chart above of the “inverted price of gold,” the rising line represents falling gold prices.

Interestingly, gold has been bouncing pretty aggressively since mid December. Why? To an extent, it’s pricing in some uncertainty surrounding Trump policies. And that would also explain the slow down and (somewhat) slide in U.S. yields. In fact, based on that chart above and the gold relationship, it looks like we could see yields back below 2.10%. That would mean a break of the technical support (the yellow line) in this next chart …

Another reason for higher gold, lower yields (i.e. higher bond prices), might be the capital flight in China. Where do you move money if you’re able to get it out in China? The dollar, U.S. Treasuries, U.S. stocks, Gold.

The data overnight showed the lowest levels reached in the countries $3 trillion currency reserve stash in 6 years. That, in large part, comes from the Chinese central banks use of reserves to slow the decline of their currency, the yuan. Of course a weakening yuan only inflames U.S. trade rhetoric.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We ended last week with a very strong jobs report, yet the measure of wage pressure was soft. That, for the near term, reduces expectations on how aggressive the Fed might be (but not a lot).

Still, the 10-year yield has drifted lower to start the week. It was 2.50% Friday afternoon. Today it’s closer to 2.40%. When the 10-year yield drifts lower, mortgage rates drift a little lower, back very close to 4% today. This all helps two of the most important tools the Fed has been focused on for the past eight years to drive economic recovery: stocks and housing.

The Trump administration, like the Fed, will need both stocks and housing to continue higher to maintain confidence in the economy, and in the agenda.

Now, on Friday I said Trump was hosting Japan’s Prime Minister Abe in Florida over the weekend for a round of golf at Mar-a-Lago. It looks like it’s this coming weekend, instead.

Interestingly, this comes as the Trump administration made a conscious effort on Friday to refocus the messaging from a protectionist narrative to an economic growth narrative.

Abe will be entering this meeting with President Trump under some peripheral scrutiny about trade imbalances. Japan runs about a $60 billion surplus with the United States. That’s about on par with Mexico, which has become a target for Trump in recent weeks. Still, as I said last week, it’s peanuts compared to China, and that’s where the Trump administration’s real attention lies.

Nonetheless, Abe is expected to come in with a plan to balance trade with the U.S., which includes working together on a big U.S. infrastructure program. And there is still considerable sensitivity surrounding the value of the yen (the Japanese currency).

As we know, under Abenomics, the yen has devalued by about 40% against the dollar. But as China has done often over the past decade, as they have headed into big meetings with global leaders, Japan seems to be walking its currency up in the days heading into the Abe/Trump meeting.

You can see in the chart above, the dollar has been in decline against the yen this year (the orange line falling represents a weaker dollar, stronger yen). The top in the USD/JPY exchange rate this year came when Trump’s chief trade negotiator was named on January 3rd. Robert Lighthizer worked in the Reagan administration and happened to be behind stiff tariffs imposed on Japan during that era on electronics.

Trump’s tough talk on trade, and the market’s continued focus on upcoming elections in Europe (that threaten to continue the trend of nationalism and protectionism) have stocks in Japan and Europe diverging from the strength we’re seeing in U.S. stocks. The Dow is above 20k. Meanwhile, Japanese stocks are still 10% off of the 2015 highs. German stocks are 7% off of 2015 highs.

But as I’ve said, growth solves a lot of problems. In addition to the underlying current of a better performing U.S. economy (with the pro-growth agenda in the pipeline), the data is already improving in both Germany and Japan. I suspect that Europe and Japan will soon be cleared from the fray of the trade protectionist rhetoric, and we’ll start seeing major European stock markets and the Japanese stock market climbing, and ultimately putting up a big number in 2017.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The Trump agenda continues to dominate the market focus as we entered the second week of Trumponomics.

To this point the market focus has been on the pro-growth agenda. With that, stocks have been higher, yields have been higher, the dollar has been higher, and global commodities have been broadly rising. Meanwhile, gold (the fear trade) has been falling and the VIX has been falling, toward ultra-low levels. The VIX, like gold, is a good market indicator of uncertainty and/or fear.

Let’s talk about the VIX…

The VIX measures the implied volatility of options on the S&P 500. This is a key component in the price investors pay for downside protection on their portfolios.

So what is implied volatility? Implied volatility measures both actual volatility and the options market maker community’s expectations (or perception of certainty) about future volatility. When market makers feel confident about the stability in markets, implied vol is lower, which makes the price of options cheaper. When they aren’t confident in stability, implied vol goes up, which makes the price of an option go up. To compensate those that are taking the other side of your trade, for the lack of predictability, you pay a premium.

With that in mind, on Friday, the VIX traded to the lowest levels since the days before the failure of Lehman Brothers. That indicates that the market had (or has) become a believer that pro-growth policies, combined with ultra-easy central bank policies have created a buffer against the downside in stocks. But that perception of downside risk is changing today, with the more vocal uprising against Trump social policies. You can see the spike (in the far right of the chart) today…

So as big money managers were closing the week last Friday, looking at Dow 20,000+ and a VIX sliding toward levels not too far from pre-crisis levels, buying downside protection was dirt cheap. This morning, they’re paying quite a bit more for that protection.

With that said, this pop in the VIX and the Dow trading off by more than 100 points today gets a lot of attention. But is there justification to think that market turbulence will begin to reflect the turbulence and division in public opinion toward Trump policies? Just gauging the extent of the market reaction from the VIX today, it’s unlikely. The chart below is the longer term view of the VIX.

My observations: The VIX has had a small bounce from very, very low levels. On an absolute basis, vol is still very cheap. When there is real fear in the air, real uncertainty about the future, you can see from the spikes in the longer term chart above, the premium for the unknown gets priced in quickly and aggressively. Given that there has been virtually no risk premium priced into the market for any falter in the Trump Presidency, or the execution of Trump policies, the moves today have been very modest. And gold (as I write) is barely changed on the day.

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We’re finishing the first full week under Trumponomics. And it’s been an active one.

It’s clear now that President Trump intends to follow through on his campaign promises. While that’s making waves with the media and with Washington types, it’s creating more certainty about the outlook for growth for the real economy and, therefore, for financial markets.

We close the week with the Dow above 20,000, on new record highs. And as we discussed yesterday, stock markets around the world are rallying too on the prospects of a stronger U.S. economy translating into a stronger global economy. We looked at the charts of Mexican and Canadian stocks yesterday–both of which are sitting on record highs. U.K. stocks are near record highs and German stocks are quickly closing in.

We already know that small business optimism in the U.S. has hit 12-year highs, jumping by the most in since 1980–on Trump’s pro-growth agenda. Today the consumer sentiment report showed sentiment is on the rise too–at 13-year highs.

Let’s talk about the data that we’re leaving behind. Fourth quarter GDP was reported today at just 1.9%. This, more than seven years removed from the failure of Lehman Brothers, an $800 billion stimulus package, seven years of zero interest rates and three rounds of quantitative easing, and the economy is running at about 60% of its normal pace. And even after taking the Fed’s balance sheet from $800 billion to $4.5 trillion, we have inflation running at less than 50% of its normal pace. This malaise is consistent throughout the world. And this is precisely why big, bold fiscal stimulus and structural change is desperately needed, and is being embraced by those that understand the dangers of the stall-speed global economy that has been kept alive by global central bank intervention. As I’ve said, at Dow 20,000, it’s just getting started.

Have a great weekend!

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

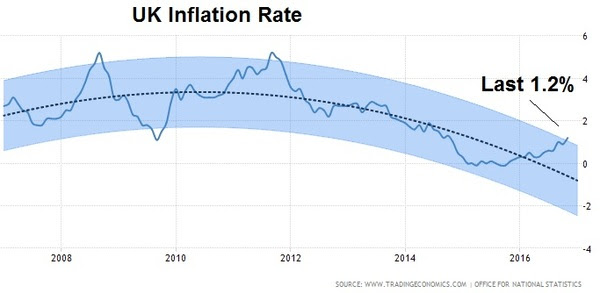

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

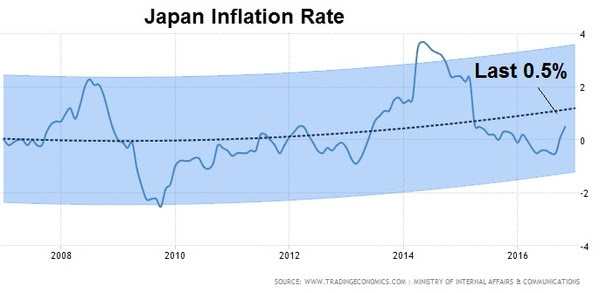

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Stocks finished the week on record highs. We talked earlier in the week about Trump’s meeting with Japan’s Prime Minister and his economic and finance advisors.

Stocks finished the week on record highs. We talked earlier in the week about Trump’s meeting with Japan’s Prime Minister and his economic and finance advisors.