We talked last week about what may be the bottom in the “decline of the retail store” story.

Walmart may be leading the way back for traditional retail. And it’s doing so, in part, by pouring money into e-commerce to fight back against Amazon.

Just as the energy industry has been beaten down by the rise of electric vehicles and clean energy, the bricks and mortar retail industry has been beaten down by the rise of Amazon. But those energy and retail companies that have survived the storm may have magnificent comebacks. They’re getting fiscal stimulus, which will lower their tax rates and should pop consumer demand. And they may be getting help with the competition. The regulatory game may be changing for the Internet giants that have nearly put them out of business.

Over the past decade, the Internet giants of today have had a confluence of advantages. They’ve played by a different rule book (one with practically no rules in it). And many of the giants that have emerged as dominant powers today, did so through direct government funding or through favor with the Obama administration.

One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007. In 2008, the DNC convention in Denver gave birth to Airbnb. By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation.

The U.K.’s Guardian has a very good piece (here) on what this has turned into, and the power that has come with it, calling it “winner takes all capitalism.”

This all makes today’s decision to repeal “net neutrality” very interesting. Is this the event that will ultimately lead to the reigning in the powerful tech giants? For the big platforms like Google, Twitter, Facebook and Uber, will it lead to transparency of their practices and accountability for the actions of its users? If so, the business models change and the Wild West days of the Internet may be coming to an end.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click hereto learn more.

As I said on Friday, people continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

We constantly hear about how the fundamentals don’t support the move in stocks. Yet, we’ve looked at plenty of fundamental reasons to believe that view (the gloom view) just doesn’t match the facts.

Remember, the two primary sources that carry the megahorn to feed the public’s appetite for market information both live in economic depression, relative to the pre-crisis days. That’s 1) traditional media, and 2) Wall Street.

As we know, the traditional media business, has been made more and more obsolete. And both the media, and Wall Street, continue to suffer from what I call “bubble bias.” Not the bubble of excess, but the bubble surrounding them that prevents them from understanding the real world and the real economy.

As I’ve said before, the Wall Street bubble for a very long time was a fat and happy one. But the for the past ten years, they came to the realization that Wall Street cash cow wasn’t going to return to the glory days. And their buddies weren’t getting their jobs back. And they’ve had market and economic crash goggles on ever since. Every data point they look at, every news item they see, every chart they study, seems to be viewed through the lens of “crash goggles.” Their bubble has been and continues to be dark.

Also, when we hear all of the messaging, we have to remember that many of the “veterans” on the trading and the news desks have no career or real-world experience prior to the great recession. Those in the low to mid 30s onlyknow the horrors of the financial crisis and the global central bank sponsored economic world that we continue to live in today. What is viewed as a black swan event for the average person, is viewed as a high probability event for them. And why shouldn’t it? They’ve seen the near collapse of the global economy and all of the calamity that has followed. Everything else looks quite possible!

Still, as I’ve said, if you awoke today from a decade-long slumber, and I told you that unemployment was under 5%, inflation was ultra-low, gas was $2.60, mortgage rates were under 4%, you could finance a new car for 2% and the stock market was at record highs, you would probably say, 1) that makes sense (for stocks), and 2) things must be going really well! Add to that, what we discussed on Friday: household net worth is at record highs, credit growth is at record highs and credit worthiness is at record highs.

We had nearly all of the same conditions a year ago. And I wrote precisely the same thing in one of my August Pro Perspective pieces. Stocks are up 17% since.

And now we can add to this mix: We have fiscal stimulus, which I think (for the reasons we’ve discussed over past weeks) is coming closer to fruition.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

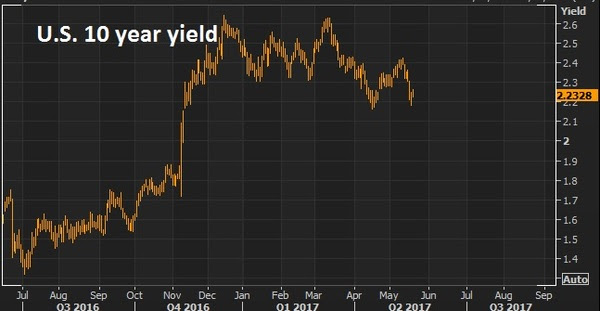

Yesterday we talked about the Draghi remarks (head of the European Central Bank) that were intended to set expectations that the ECB might be moving toward the exit doors on QE and zero interest rate policy. That bottomed out global rates — which popped U.S. rates further today. The Bank of England piled on today, talking about rate normalization soon.

We’ve gone from 2.12% in the U.S. ten year yield to 2.25% in about 24 hours. These are big swings in the interest rate market – a big bounce and, as I’ve said, the bottom appears to be in for rates.

As importantly, this prepared speech by Draghi could very well cement the top in the dollar. It begins to tighten a very wide interest rate spread between the U.S. and global rates. We entered the year with the Fed going one way (tightening) while the rest of the world was going the other way (easing). That’s a recipe for capital to storm into U.S. assets — into the dollar. And now that may be over.

I’ve been researching long-term cycles in the dollar for a very long time and throughout the global financial crisis period, it these cycles in the world’s reserve currency have been my guidepost for drawing a lot of conclusions on markets and the outlook for capital flows over the past several years.

Despite the choppiness in the dollar for much of the crisis, if we look back at the cycles following the failure of the Bretton Woods system, we were able, very early on, to determine the dollar was in a bull cycle.

This view came in the face of all of the negative global sentiment toward the dollar in 2010. Foreign leaders were taking shots at the Fed, accusing the Fed of trying to destroy the dollar. People were calling for the end of the dollar as the world’s reserve currency. All the while, the dollar held firm and ultimately made an aggressive climb.

Take a look below at my chart on the long term dollar cycles…

I’ve watched this chart for quite some time, defining the five complete dollar cycles over the past nearly 40 years, and the most recent bull cycle.

If we mark the top of the most recent cycle in early January, this bull cycle has matched the longest cycle in duration (at 8.8 years) and comes in just shy of the long-term average performance of the five complete cycles. The most recent bull cycle added 47%. The average change over a long term cycle has been 56%. This all argues that the dollar bull cycle is over. And a weaker dollar is ahead. That should go over very well with the Trump administration.

Join the Billionaire’s Portfolioto hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

Today I want to take a look back at my March 7th Pro Perspectives piece. And then I want to talk about why a power shift in the economy may be underway (again).

Big Picture .. Market Perspectives March 7, 2017

“A big component to the rise of Internet 2.0 was the election of Barack Obama. With a change in administration as a catalyst, the question is: Is this chapter of the boom in Silicon Valley over? And is Snap the first sign?

Without question, the Obama administration was very friendly to the new emerging technology industry. One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007, before Obama announced his run for president, and just as Facebook was taking off after moving to and raising money in Silicon Valley (with ten million users). Facebook was an app for college students and had just been opened up to high school students in the months prior to Obama’s run and the hiring of the former Facebook cofounder. There was already a more successful version of Facebook at the time called MySpace. But clearly the election catapulted Facebook over MySpace with a very influential Facebook insider at work. And Facebook continued to get heavy endorsements throughout the administration’s eight years.

In 2008, the DNC convention in Denver gave birth to Airbnb. There was nothing new about advertising rentals online. But four years later, after the 2008 Obama win, Airbnb was a company with a $1 billion private market valuation, through funding from Silicon Valley venture capitalists. CNN called it the billion dollar startup born out of the DNC.

Where did the money come from that flowed so heavily into Silicon Valley? By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S.

When institutional investors see that kind of money flowing somewhere, they chase it. And valuations start exploding from there as there becomes insatiable demand for these new ‘could be’ unicorns (i.e. billion dollar startups).

Who would throw money at a startup business that was intended to take down the deeply entrenched, highly regulated and defended taxi business? You only invest when you know you have an administration behind it. That’s the only way you put cars on the street in NYC to compete with the cab mafia and expect to win when the fight breaks out. And they did. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation. Uber is valued at $60 billion. That’s more thanthree times the size of Avis, Hertz and Enterprise combined.

Will money keep chasing these companies without the wind any longer at their backs?”

Now, this was back in March. And that was the question — will it keep going under Trump? Can they continue to thrive/ if not survive without policy favors. Most importantly for the billion dollar startup world, will the private equity capital dry up. This is what it’s really all about. Will the money that chased the subsidies from D.C. to Silicon Valley for eight years (i.e. the trillion dollar pension funds) stop flowing? And will it begin chasing the new favored industries and policies under the Trump administration?

It seems to be the latter. And it seems to be happening in the form of a return to the public markets — specifically, the stock market.

And it may be amplified because of the huge disparity in what is being favored. In Silicon Valley, innovation is favored. Profitability? Remember, the 90s tech bubble. The measure of success for those companies was “eyeballs.” How much traffic were they getting to their websites? Today, when you hear a startup founder talk about the success benchmarks, it rarely has anything to do with with revenue or profit. It’s all about headcount (how many people they’ve hired) and money raised (which enables them to hire people). They are validated by convincing investors to fund them (mostly with our pension money).

Now, the other side of this coin: Trumponomics. Remember, among the Trump policies (corporate tax cuts, repatriation, deregulation, infrastructure spend), the most common sense play in the stock market has been flooding money into companies that make a lot of money. Those that make a lot of money have the most to gain from a slash in the corporate tax rate — it falls right to the bottom line. Leading the way on that front, is Apple. They make a lot of money. And they will make a lot more when a tax cut comes, making the stock even cheaper. That’s why it’s up 25% year-to-date. That’s 2.5 times the performance of the broader market.

Meanwhile, let’s take a look back at the Snapchat. Snapchat doesn’t make money. And even after a 1/3 haircut on the valuation, trades about 35 times revenue. And now, as a public company, probably doesn’t get the protection from the venture capital/private equity community that may have significant investments in its competitors. So the competitors (like Facebook) are circling like sharks to copy their business.

What about Uber? The Uber armor may be beginning to crack as well, with the leadership shakeup in recent weeks. Maybe a good signal for how Uber may be doing? Hertz! Hertz has bounced about 20% from the bottom this week.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

The Nasdaq trade unwound some today. From the peak this morning in the futures of 5898 the tumble started around 11am, falling to as low as 5660. That’s 238 Nasdaq futures points or 4% – quite a sharp move.

Remember, it seems like an overdone trade (driven by the big tech stocks). But as we discussed last week, the tech heavy Nasdaq has simply been a catch up trade — something that has lagged the strength in the broader market.

Here’s the chart we looked at last week.

This chart goes back to the lows driven by the oil price crash that bottomed out earlier last year.

Still, with the Nasdaq at +18% ytd and S&P 500 +9% ytd, as of this morning, as we’ve seen many times in this post-crisis era, the air pockets of illiquidity in stocks can give back gains very, very quickly. As they say, stocks go up on an escalator and down in an elevator.

The Trump trend, in the chart above, was nearly tested today — the same day a new all-time high was marked!

If we get another few days of sharp downside, it will be a tremendous buying opportunity – get your shopping list ready. And if that downside slide does indeed come, it could come at a very interesting time. It would add another (but very signficant) reason the Fed may balk on a rate hike next week. The other reasons? We discussed them yesterday (here).

Have a great weekend.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

Stocks continue to bounce back today. But the technical breakdown of the Trump Trend on Wednesday

still looks intact. As I said on Wednesday, this looks like a technical correction in stocks (even considering today’s bounce), not a fundamental crisis-driven sell-off.

With that in mind, let’s take a look at the charts on key markets as we head into the weekend.

Here’s a look at the S&P 500 chart….

For technicians, this is a classic “break-comeback” … where the previous trendline support becomes resistance. That means today’s highs were a great spot to sell against, as it bumped up against this trendline.

Very much like the chart above, the dollar had a big trend break on Wednesday, and then aggressively reversed Thursday, only to follow through on the trend break to end the week, closing on the lows.

On that note, the biggest contributor to the weakness in the dollar index, is the strength in the euro (next chart).

The euro had everything including the kitchen sink thrown at it and it still could muster a run toward parity. If it can’t go lower with an onslaught of events that kept threatening the existence of the euro, then any sign of that clearing, it will go higher. With the French elections past, and optimism that U.S. growth initiatives will spur global growth (namely recovery in Europe), then the European Central Bank’s next move will likely be toward exit of QE and extraordinary monetary policies, not going deeper. With that, the euro looks like it can go much higher. That means a lower dollar. And it means, European stocks look like, maybe, the best buy in global stocks.

A lower dollar should be good for gold. As I’ve said, if Trump policies come to fruition, inflation could get a pop. And that’s bullish for gold. If Trump policies don’t come to fruition, the U.S. and global growth looks grim, as does the post-financial crisis recovery in general. That’s bullish for gold.

This big trendline in gold continues to look like a break is coming and higher gold prices are coming.

With all of the above, the most important chart of the week is probably this one …

The 10 year yield has come all the way back to 2.20%. The best reason to wish for a technical correction in stocks, is not to buy the dip (which is a good one), but so that the pressure comes out of the interest rate market (and off of the Fed). The run in the stock market has clearly had an effect on Fed policy. And the Fed has been walking rates up to a point that could choke off the existing economic recovery momentum and, worse, neutralize the impact of any fiscal stimulus to come. Stable, low rates are key to get the full punch out of pro-growth policies, given the 10 year economic malaise we’re coming out of.Invitation to my daily readers: Join my premium service members at Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse portfolio of the most high potential stocks.

Yesterday, following the slide in stocks, we looked at some charts on stocks, gold and the dollar. We talked about the media and Wall Street’s need to fit price action to a story. And we asked if the story did indeed warrant fitting it to the price action. Was a crisis beginning or just a correction for stocks?The answer: It still looks like a market that values fiscal stimulus and structural change over political mudslinging and scandal. For stocks, the news may have been the catalyst to start a healthy technical correction.

Today, the market behavior appears to support that view.

Now, with the idea that a technical correction is (I think) underway for stocks, and maybe for months, until we get a better handle on policy action, remember this: a correction in stocks is a buying opportunity.

Major asset classes, over time, will rise (stocks, bonds, real estate). The value of these core assets will grow faster than the value of cash.

That comes with one simple assumption. The world, over time, will improve, will grow and will be a better and more efficient place to live than it was before. If that assumption turned out to be wrong, we have a lot more to worry about than the value of our stock portfolio.

With that said, as an average investor that is not leveraged, dips in stocks, particularly U.S. stocks—the largest economy in the world, with the deepest financial markets—should be bought, because in the simplest terms, over time, the broad stock market has an upward sloping trajectory. Instead, dips in stocks tend to create fear, and fear creates selling, at precisely the time we should be buying.

With this in mind, we’ve had a brief dip of about 4% in stocks within the “Trump trend” (the post–election rise in stocks). A typical correction is around 10%. But strong bull markets tend to have shallow retracements. A 6%–10% correction in stocks would take us back to the 200–day moving average (minimum), and maybe as low as 2,200 in the S&P 500.

Invitation to my daily readers: Join my premium service members at Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse portfolio of the most high potential stocks.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

Why is the messaging so different? Remember, the financial media and Wall Street are easily distractible. Not only do they have short attention spans, but they’ve been trained throughout their careers to find new stories to obsess about. They need to interpret, pontificate, strategize to feel valued. Approaching their jobs with the idea that a slow moving dominant theme is at work is just too boring.

This is the disconnect between markets and the narrative. We have major central banks around the world that continue to print money. These central banks buy assets with that freshly printed money. That means, stocks, bonds, commodities go higher. And now we have everyone’s fate (the global economy) tied to the outcome of new policies from the leading economy in the world – efforts to restore sustainable growth through structural reform and fiscal stimulus. That hopeful outlook does nothing but underpin the rise in asset prices (stocks, bonds, commodities, real estate).

Yesterday we got a look under the hood of the portfolios of the biggest money managers in the world, via their 13F filings (required quarterly portfolio disclosures to the SEC). It’s been clear that the biggest and best, embrace this big theme, and have been aggressively positioning to take advantage of the very bullish proposed policy tailwinds for stocks, which are: 1) a corporate tax rate cut, which will go right to the bottom line for profitable companies. Not surprisingly, which stocks have been leading the way in the climb in the indicies? The one’s that make a lot of money (Apple, Microsoft, Google). 2) a repatriation tax holiday that will bring back trillions of dollars onshore, to be paid back to shareholders and put to work in the economy through investment and projects. 3) a trillion dollar infrastructure spend that, regardless of how difficult it may be to legislate, should happen in one form or another.

Among the reports on portfolio holdings yesterday, we heard from the Swiss National Bank. As I said above, don’t forget there are still central banks deeply entrenched in QE and, beyond local government bonds, are buying foreign assets (in large amounts). Switzerland’s central bank has more freshly printed money to put to work every quarter, and has been increasing their allocation to equities dramatically – $80 billion of which is now (as of the end of Q1) in U.S. stocks! That’s a 29% bigger stake than they had at the end of 2016. The SNB is the world’s eighth biggest public investor.

So keep this big theme in mind: Central banks remain involved, but the baton has been passed, from a central bank-driven recovery to a fiscal stimulus-driven recovery. And everyone needs it to work.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

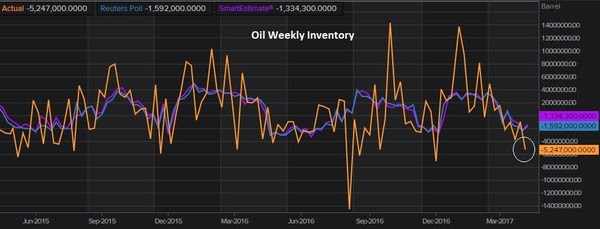

Oil has been on the move the past few days. Was this recent dip a gift to buy?The oil inventory report yesterday showed a big drawdown on oil inventories. The market expectation was for about a drawdown of 1.5 million barrels. It came in at 5 million.

That has oil on a big bounce for the week. It’s trading about 8% higher than it was at the lows of last Friday. But we still sit below the 200 day moving average and below the key $50 level (the comfort zone for those producers, namely the shale industry, to fire back up idle capacity).

The weakness in oil has a lot to do with weakness across broader commodities. And broader commodities typically correlates well with what Chinese stocks are doing.

You can see in the chart above, how closely the two track. This bottom in commodities has/had everything to do with the outlook for a big infrastructure spend out of the Trump administration. It’s yet to bubble up toward the top of the action list. With that, the momentum has either stalled on this trade, or it’s a pause before another leg higher in this early stage multi-year rebound. My bet is on the latter. Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

Those that oppose it warn that it will lead to another financial crisis. On that note, I want to revisit my take from earlier this year on the cause of the crisis that almost destroyed the global economy.

“With all of the complexities of the housing bubble and the subsequent global financial crisis, it can seem like a web of deceit. But it all boils down to one simple actor. It wasn’t Wall Street. It wasn’t hedge funds. It wasn’t mortgage brokers. These entities were operating, in large part, from the natural force of economics: incentives.

It wasn’t even the government’s initiative to promote home ownership that led to the proliferation of mortgages being given to those that couldn’t afford them.

So who was the culprit?

It was the ratingsagencies.

Housing prices were driven sky high by the availability of mortgages. Mortgages were made easily available because the demand to invest in mortgages, to fund those mortgages, was sky high.

But what drove that demand to such high levels?

When the mortgages were combined together in a package (securitized as a mix of good mortgages, and a lot of bad/higher yielding mortgages), they were bought, hand over fist, by the massive multi-trillion dollar pension industry, banks and insurance companies. Yes, the guys that are managing your pension funds, deposit accounts and insurance policies were gobbling up these mortgage securities as fast as they could, but ONLY because the ratings agencies were stamping them all with a top AAA rating. Who would encourage such a thing? Congress. In 1984 they passed a law making it okay for banks, pension funds and insurance companies to buy/treat high rated secondary mortgages like they would U.S. Treasuries.

So as investment managers, in the business of building the best performing risk-adjusted portfolio possible, and in direct competition with their peers, they couldn’t afford NOT to buy these securities. They came with the safest ratings, and with juicy returns. If you don’t buy these, you’re fired.

To put it all very simply, if these securities were not AAA rated, the pension funds would not have touched them (certainly not to the extent). With that, if the there’s no appetite to fund the mortgages (no money chasing it), then the ultra-easy lending practices never happen, and housing prices never skyrocket on unwarranted and unsustainable demand. The housing bubble doesn’t build, doesn’t bust, and the financial crisis doesn’t happen.

That begs the question: Why did the ratings agencies give a top rating to a security that should have received a lower rating, if not much lower?

First, it’s important to understand that the ratings agencies get paid on the products they rate BY the institutions that create them. That’s right. That’s their revenue model. And only a group of these agencies are endorsed by the government, so that, in many cases, regulatory compliance on a financial product requires a rating from one of these endorsed agencies.”

Keep this in mind as the fear mongering over the talk of repeal of rework of Dodd Frank heats up.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

We talked last week about what may be the bottom in the “decline of the retail store” story.

We talked last week about what may be the bottom in the “decline of the retail store” story. As I said

As I said

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.