Since the election, almost a year ago, we’ve talked about the great passing of the torch, from a monetary policy-driven global economic recovery (which proved dangerously weak and shallow) to a fiscal stimulus-driven recovery (which finally gives us a chance to return to trend growth).

Now, almost a year in, policy execution on the fiscal stimulus front is moving. The Fed has hiked rates three times. In the past week, the ECB has signaled the end of QE in Europe is coming. And this Thursday the Bank of England is expected to raise rates for the first time in a decade.

Again, if you can block out the day-to-day noise, this is all confirming the exit of the post-crisis deleveraging era of the past decade – it’s all playing out fairly close to script.

With that, I want to revisit my note from early January of this year, which argues the case for this “passing of the torch” and emphasizes the value of having some bigger picture perspective…

From my Market Perspectives piece: JANUARY 18, 2017

“Two weeks ago, in my daily Market Perspectives note, I talked about the five reasons, even at Dow 20,000, that stocks look extraordinarily cheap as we head into 2017.

Today I want to talk a bit more about the idea that the timing is right for a pop in economic growth.

For the past ten years, we’ve heard experts pontificate about ‘what inning we’re in,’ during the crisis era. I think there are good reasons to believe the game is over, and it was ended on election night–that was the catalyst.The policy responses and regime shift have more to do with the evolution of the global financial crisis and human psychology, than it does with the character behind it all.

I want to focus on a study from Carmen Reinhart and Kenneth Rogoff – the two economists that laid out the script, back in 2008, for precisely what the world has experienced over the past ten years. Fortunately, Bernanke was a believer in it. That’s why the Fed kept its foot on the gas, even in the face of a lot of scrutiny from people that blamed the Fed on extending the crisis.

Reinhart and Rogoff studied eight centuries of financial crises and they found striking commonalities in the aftermath. They found that financial crises tend to lead to sovereign debt crises. And sovereign debt crises tend to be contagious. Clearly, we’ve seen it.

Reinhart went on to look at the 15 severe financial crises since World War II and found that they were typically driven by credit bubbles. Check.

Importantly, they found that the credit bubble typically took as long to unwind (or de-lever) as it took to build. And the deleveraging period tends to mean ultra-slow economic activity as consumers, businesses and governments are paying down debt, not spending. And because of this, the research suggested that throughout this ten-year deleveraging period we should expect: 1) economic growth will trend at lower levels than pre-crisis growth, 2) housing prices will remain anywhere from 20% to 50% below peak levels and 3) unemployment will hover around 5% higher than pre-crisis levels. Check, check and check.

In the current case, Reinhart and Rogoff said the credit bubble was built over about a decade. That means we all should all have expected a decade long deleveraging period.

Now, with that, you can mark the top in the bubble as the 2006 housing top, or in 2007 when we the first big mortgage company and Bear Stearns hedge fund failed, or 2008, when consumer credit peaked. We’re somewhere in the middle of this window now and major turning points in markets tend to come with significant events. It’s a fair argument to make that the Trump election was a significant event for the world. With that, we may find that the crisis period officially ended with the election, when the history books look back on this current period of time.’

So that was my take back in January. It’s not easy to watch the process play out. It can be slow and ugly. But we’re seeing the reaction in stocks to this thesis – now at 23k in the DJIA. And we’re getting some momentum building on the policy making side that further supports this structural turning point is here (or has been here).

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

As I said on Friday, people continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

We constantly hear about how the fundamentals don’t support the move in stocks. Yet, we’ve looked at plenty of fundamental reasons to believe that view (the gloom view) just doesn’t match the facts.

Remember, the two primary sources that carry the megahorn to feed the public’s appetite for market information both live in economic depression, relative to the pre-crisis days. That’s 1) traditional media, and 2) Wall Street.

As we know, the traditional media business, has been made more and more obsolete. And both the media, and Wall Street, continue to suffer from what I call “bubble bias.” Not the bubble of excess, but the bubble surrounding them that prevents them from understanding the real world and the real economy.

As I’ve said before, the Wall Street bubble for a very long time was a fat and happy one. But the for the past ten years, they came to the realization that Wall Street cash cow wasn’t going to return to the glory days. And their buddies weren’t getting their jobs back. And they’ve had market and economic crash goggles on ever since. Every data point they look at, every news item they see, every chart they study, seems to be viewed through the lens of “crash goggles.” Their bubble has been and continues to be dark.

Also, when we hear all of the messaging, we have to remember that many of the “veterans” on the trading and the news desks have no career or real-world experience prior to the great recession. Those in the low to mid 30s onlyknow the horrors of the financial crisis and the global central bank sponsored economic world that we continue to live in today. What is viewed as a black swan event for the average person, is viewed as a high probability event for them. And why shouldn’t it? They’ve seen the near collapse of the global economy and all of the calamity that has followed. Everything else looks quite possible!

Still, as I’ve said, if you awoke today from a decade-long slumber, and I told you that unemployment was under 5%, inflation was ultra-low, gas was $2.60, mortgage rates were under 4%, you could finance a new car for 2% and the stock market was at record highs, you would probably say, 1) that makes sense (for stocks), and 2) things must be going really well! Add to that, what we discussed on Friday: household net worth is at record highs, credit growth is at record highs and credit worthiness is at record highs.

We had nearly all of the same conditions a year ago. And I wrote precisely the same thing in one of my August Pro Perspective pieces. Stocks are up 17% since.

And now we can add to this mix: We have fiscal stimulus, which I think (for the reasons we’ve discussed over past weeks) is coming closer to fruition.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Yesterday we looked at the charts on oil and the U.S. 10 year yield. Both were looking poised to breakout of a technical downtrend. And both did so today.

Here’s an updated look at oil today.

And here’s a look at yields.

We talked yesterday about the improving prospects that we will get some policy execution on the Trumponomics front (i.e. fiscal stimulus), which would lift the economy and start driving some wage pressure and ultimately inflation (something unlimited global QE has been unable to do).

No surprise, the two most disconnected markets in recent months (oil and interest rates) have been the early movers in recent days, making up ground on the divergence that has developed with other asset classes.

Now, oil will be the big one to watch. Yields have a lot to do, right now, with where oil goes.

Though the central banks like to say they look at inflation excluding food and energy, they’re behavior doesn’t support it. Oil does indeed play a big role in the inflation outlook – because it plays a huge role in financial stability, the credit markets and the health of the banking system. Remember, in the oil price bust last year the Fed had to reverse course on its tightening plan and other major central banks coordinated to come to the rescue with easing measures to fend off the threat of cheap oil (which was quickly creating risk of another financial crisis as an entire shale industry was lining up for defaults, as were oil producing countries with heavy oil dependencies).

So, if oil can sustain above the $50 level, watch for the inflation chatter to begin picking up. And the rate hike chatter to begin picking up (not just with the Fed, but with the BOE and ECB). Higher oil prices will only increase this divergence in the chart below, making the interest rate market a strong candidate for a big move.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Stocks are sliding more aggressively today. Wall Street and the media always have a need to assign a reason when stocks move lower. There have been plenty of negatives and uncertainties over the past seven months — none of which put a dent in a very strong opening half for stocks.

But markets don’t go straight up. Trends have retracements. Bull markets have corrections. And despite what many people think, you don’t need a specific event to turn markets. Price can many times be the catalyst.

If we look across markets, it’s safe to say it doesn’t look like a market that is pricing in nuclear war. Gold is higher, but still under the highs of a month ago. The 10 year yield is 2.21%. Two weeks ago, it was 2.22%. That doesn’t look like global capital is fleeing all parts of the world to find the safest parking place.

Now, on the topic of North Korea, the media has found a new topic to obsess about– and to obsessively denounce the administration’s approach. With that, let’s take a look at the Trump geopolitical strategy of calling a spade a spade.

As we know, Mexico was the target heading into the election. Trump’s tough talk against illegal immigration and drug trafficking drew plenty of scrutiny. People feared the protectionist threats, especially the potential of alienating the U.S. from its third biggest trading partner. We’re still trading with Mexico. And the U.S. is doing better. So is Mexico. Mexican stocks are up 11% this year. The Mexican currency is up 13% this year.

China has been a target for Trump. He’s been tough on China’s currency manipulation and, hence, the lopsided trade that contributed heavily to the credit crisis. Despite all of the predictions, a trade war hasn’t erupted. In fact, China has appreciated its currency by 5% this year. That’s a huge signal of compliance. That’s among the fastest pace of currency appreciation since they abandoned the peg against the dollar more than 12 years ago (which was China’s concession to threats of a 30% trade tariff that was threatened by two senators, Schumer and Graham, back in 2005). And even in the face of a stronger currency (which drags on exports, a key driver of the economy), stocks are up 5% in China through the first seven months of the year.

Bottom line: It’s fair to say, the tough talk has been working. There has been compromise and compliance. So now Trump has stepped up the pressure on North Korea, and he has been pressuring China, to take the side of the rest of the world, and help with the North Korea situation – and through China is how the North Korea threat will likely get resolved.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

As we know, inflation has been soft. Yet the Fed has been moving on rates, assuming that they have room to move away from zero without counteracting the same data that is supposed to be driving their decision to increase rates.

Thus far, after four (quarter point) increases to the Fed funds rate, the moves haven’t resulted in a noticeable tightening of financial conditions. That’s mainly because the interest rate market that most key consumer rates are tied to have remained low. Because inflation has remained low.

A key contributor to low inflation has been low oil prices (though the Fed doesn’t like to admit it) and commodity prices in general that have yet to sustain a recovery from deeply depressed levels (see the chart below).

But that may be changing.

Commodities have been lagging the rest of the “reflation” trade after the value of the index was cut in half from the 2011 highs. Remember, we looked at this divergence between the stocks and commodities last month. Commodities are up 6% since.

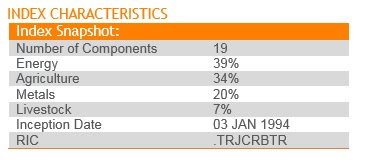

Things are picking up. Here’s the makeup of the broadly followed commodities index.

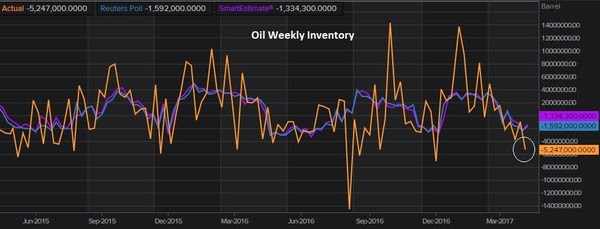

You can see, energy has a heavy weighting. And oil, with another strong day today, looks like a break out back to the $50 level is coming.With today’s inventory data, we’ve now had 12 out of the past 14 weeks that oil has been in a draw (drawing down on supply = bullish for prices). And with that backdrop, the CRB index, after being down as much as 13% this year, bottomed following the optimistic central bank commentary last month, and is looking like it may be in the early stages of a big catch-up trade. And higher oil (and commodity prices in general) will likely translate into higher inflation expectations.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

As for oil: From the depths of the oil price crash last year, remember, we discussed the prospects for a huge bounce. Oil prices at $26 were threatening to undo the trillions of dollars of work central banks and governments had done to stabilize the global economy. Central banks couldn’t let it happen. After a series of coordinated responses (from the BOJ, China, ECB and the Fed), oil bottomed and quickly doubled.

Also at that time, two of the best oil traders in the world were calling the bottom and calling for $70-$80 oil by this year (Pierre Andurand and Andy Hall). Another commodities king that called the bottom: Leigh Goehring.

Goehring, one of the best commodities investors on the planet, has also laid out the case for $100 oil by next year. He says he’s “wildly bullish” oil in his recent quarterly investor letter at his new fund, Goehring & Rozencwajg.

Goehring argues that the IEA inventory numbers are flawed. He thinks oil the market is already over-supplied and is in a draw, as of May of last year. With that, he thinks the OPEC cuts will ultimately exacerbate the deficit and send prices aggressively higher. He says “we remain ‘wildly’ bullish and believe that there is a very high probability of oil prices reaching triple digits in the first half of 2018.”

Follow This Billionaire To A 172% WinnerIn our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Oil has been on the move the past few days. Was this recent dip a gift to buy?The oil inventory report yesterday showed a big drawdown on oil inventories. The market expectation was for about a drawdown of 1.5 million barrels. It came in at 5 million.

That has oil on a big bounce for the week. It’s trading about 8% higher than it was at the lows of last Friday. But we still sit below the 200 day moving average and below the key $50 level (the comfort zone for those producers, namely the shale industry, to fire back up idle capacity).

The weakness in oil has a lot to do with weakness across broader commodities. And broader commodities typically correlates well with what Chinese stocks are doing.

You can see in the chart above, how closely the two track. This bottom in commodities has/had everything to do with the outlook for a big infrastructure spend out of the Trump administration. It’s yet to bubble up toward the top of the action list. With that, the momentum has either stalled on this trade, or it’s a pause before another leg higher in this early stage multi-year rebound. My bet is on the latter. Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Over the past week, I’ve talked about the potential for disruption in what has been very smooth sailing for financial markets (led by stocks). While the picture has grown increasingly murkier, markets had been pricing in the exact opposite – which makes things even more vulnerable to a shakeout of the weak hands.

With that, it looked like we are indeed working on a correction in stocks. But it’s not just because stocks are down. It’s because we have some very important technical developments across key markets. The Trump trend has been broken.

Let’s take a look at the charts …

The above chart is the S&P 500. We looked at a break in the futures market last week. Today we get a big break in the cash market. This trendline represents the nice 45 degree climb in stocks since election night on November 8th. We have a clean break today.

Stocks ran up on the prospects that Trumponomics can end the decade long malaise in, not just the U.S. economy, but the global economy too. With that, the money that has been parked in U.S. Treasuries begins to leave. Moreover, any speculators that were betting the U.S. would follow the world into negative rate territory run for the exit doors. That sends Treasury bond prices lower and yields higher (as you can see in the chart above). So today, we also get a break of this “Trump trend” in rates as well (the yellow line). Remember, this is after the Fed’s rate hike last week — rates are moving lower, not higher.

Next up, gold …

I talked about gold yesterday — as being the clearest trade (higher) in an increasingly murkier picture for global financial markets. You can see in the chart above, gold is now knocking on the door of a break in this post-election Trump trend.

Remember, we’ve talked about the buy-the-rumor sell-the-fact phenomenon in markets. The beginning of the Trump trend in stocks started on election night (buying “the rumor” in anticipation of pro-growth policies). The top in stocks came the day following the President’s speech to the joint sessions of Congress (selling “the fact”, entering the “show me” phase).

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recent addition to the portfolio – a stock that one of the best activist investors in the world thinks will double.

We had a heavy event calendar last week for markets, with the Fed, BOJ and BOE meetings. And then we had the anticipation of the G-20 Finance Minister’s meeting as we headed into the weekend.

As I said to open the week last week, markets were pricing in a world without disruptions. But disruptions looked likely. Still, the week came and went and stocks were little changed on the week, but yields came in lower (despite the Fed’s third rate hike) and the dollar came in lower (again, despite the Fed’s third rate hike).

Is that a signal?

Maybe. But as we discussed on Friday, the divergence between market rates and the rate the Fed sets is part central bank-driven Treasury buying (from those still entrenched in QE — Japan, Europe), and part market speculation that higher rates are threatening to the economy, and therefore traders sell short term Treasuries (rates go higher) and buy longer term Treasuries (rates go lower). With that, the Fed has been ratcheting the Fed Funds rate higher, now three times, but the 10 year government bond yield is doing nothing.

As for the dollar, if your currency has been weak, no one wanted to head into a G-20 Finance Ministers meeting and sit across the table from the new Treasury Secretary under the Trump administration (Mnuchin) and be drawn into the fray of currency manipulation claims. With that, the dollar weakened across the board last week.

All told, we had little disruption last week, but things continue to look vulnerable this week. Today we have the FBI Director testifying before Congress and acknowledging an open investigation of Trump associates contacts with Russia during the election. Fed officials have already been out in full force today make a confusing Fed picture even more confusing. And it sounds like the UK will officially notify the EU on March 29 that they will exit.

With all of the above in mind, and given the growth policies from the Trump administration still have little visibility on “when” they might get things done, the picture for markets has become muddied.

This all makes stocks vulnerable to a correction, though dips should be met with a lot of buying interest. Perhaps the clearest trade in this picture that’s become more confusing to read, is gold.

Gold jumped on the Fed rate hike last week, and Yellen’s more hawkish tone on inflation. If she’s right, gold goes higher. If she’s wrong, and the Fed has made a big mistake by hiking three times in a world that still can’t sustain much growth or inflation, gold probably goes higher on the Fed’s self-inflicted wounds to the economy.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

We’ve talked about the drift (now slide) lower in interest rates over the past couple of days. This is a big deal and something to keep a close eye on. Remember, this move lower comes in the face of a strong jobs number on Friday. Following that number, the yield on the 10-year traded up to 2.50%. Today we’re looking at 2.35% (low of 2.32%).

In contrast to this move in rates, stocks are sitting on record highs, if not making new record highs. Oil has been stable in a $50-$55 range. The dollar isn’t doing much. Implied volatility on the stock market is dead. And commodities are relatively quiet, except for gold.

On that note, yesterday we looked at the tight correlation of the inverse price of gold and yields since the election (i.e. gold goes up, yields go down). And in recent weeks, yields have been lagging the strength in gold, making the case for even lower yields to come.

We looked at the below trendline on the 10-year yesterday that was testing… that gave way today.

This move lower in yields puts both the Trump administration and the Fed in a much more comfortable spot.

A continued rise in market interest rates would force the Fed to be more aggressive, both of which would work against fiscal stimulus, dulling the contribution to growth, if not neutralizing it all together. Higher rates would slow the housing market and slow spending, especially in a fragile economy. Among the things to be worried about, higher rates, too soon, could be the biggest (bigger than protectionism, European elections…)

President Trump was said to be asking for advice on the administration’s view on the dollar overnight. I suspect the upcoming meeting with Japan’s Prime Minister (and co.) had something (a lot) to do with it. This is precisely what we’ve been talking about. The dollar and the yen are squarely in the crosshairs for this face-to-face meeting. But Trump may learn from the meeting that he would far prefer a stronger dollar and weaker yen, than a 4-4.5% ten year yield by the end of the year.

As I’ve said, Japan’s QE policies, which weaken the yen, also offer an anchor to U.S. interest rates, keeping them in check. I suspect the softening of U.S. yields, as all other markets are quiet, may have something to do with Chinese money leaving China (as we discussed yesterday). But it also may be influenced by Japan, finding the best, safest parking place for freshly printed money (i.e. buying U.S. Treasuries, which pushed down U.S. rates) – and showing that benefits of that influence to the new President.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Since the election, almost a year ago, we’ve talked about the great passing of the torch, from a monetary policy-driven global economic recovery (which proved dangerously weak and shallow) to a fiscal stimulus-driven recovery (which finally gives us a chance to return to trend growth).

Since the election, almost a year ago, we’ve talked about the great passing of the torch, from a monetary policy-driven global economic recovery (which proved dangerously weak and shallow) to a fiscal stimulus-driven recovery (which finally gives us a chance to return to trend growth). As I said

As I said

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.