We talked yesterday about run up in bitcoin. The price of bitcoin jumped another 14% today before falling back.

As I said yesterday, it looks like Chinese money is finding it’s way out of China (despite the capital controls) and finding a home in bitcoin (among other global assets). If you own it, be careful. The last time the price of bitcoin ran wild, was 2013. It took about 11 days to triple, and about 18 days to give it all back. This time around, it’s taken two months to triple (as of today).

If you’re looking for a warning signal on why it might not be sustainable (this bitcoin move), just look at the behavior across global markets. It’s not exactly an environment that would inspire confidence.

Gold is flat. Interest rates are soft. Stocks are constantly climbing. Commodities are quiet, except for oil — which fell back below $50 today on news that OPEC did indeed agree to extend its production cuts out to March of next year (bullish, though oil went south).

When the story is confusing, conviction levels go down, and cash levels go up (i.e. people de-risk). And maybe for good reason.

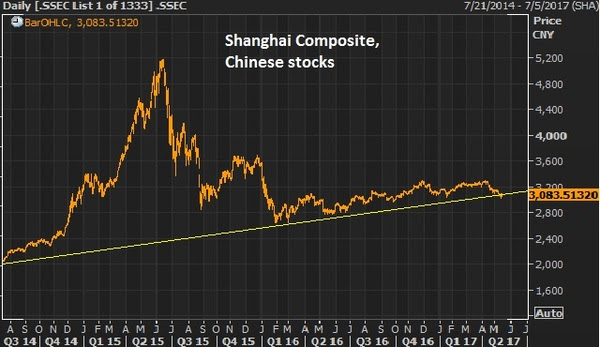

In looking at the bitcoin chart today, I thought back to the run up in Chinese stocks in early 2015. Here’s a look at the two charts side by side, possibly influenced by a lot of the same money.

The crash in Chinese stocks took global markets with it. It’s often hard to predict that catalyst that might prick a bubble and even harder to see the links that might lead to broader market instability. In this case, though, there are plenty of signs across markets that things are a little weird.

Invitation to my daily readers: Join my premium service members atBillionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse stock portfolio where I follow the lead of the best activist investors in the world. Our goal is to do multiples of what broader stocks do. Our portfolio was up 27% in 2016. Join me today, risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

Let’s take at the chart…

While the agreements out of China were said not to touch on steel and industrial metals, the first steps of cooperation could put a bottom in the slide in metals like copper and iron ore. These are two commodities that should be direct beneficiaries in a world with better growth prospects, especially with prospects of a $1 trillion infrastructure spend in the U.S. With that, they had a nice run up following the election but have backed off in the past couple of months, as the infrastructure spend appeared not to be coming anytime soon.

Here’s copper and the S&P 500…

Trump policies are bullish for both. Same said for iron ore…

This is right in the wheelhouse of Wilbur Ross, Trump’s Secretary of Commerce. He’s made it clear that he will fight China’s dumping of steel on the U.S. markets, which has driven steel prices down and threatened the livelihood of U.S. steel producers. Keep an eye on these metals next week, and the stocks of producers.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

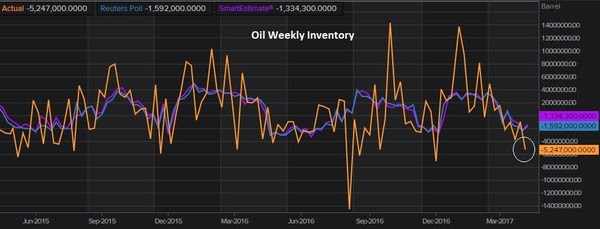

Oil has been on the move the past few days. Was this recent dip a gift to buy?The oil inventory report yesterday showed a big drawdown on oil inventories. The market expectation was for about a drawdown of 1.5 million barrels. It came in at 5 million.

That has oil on a big bounce for the week. It’s trading about 8% higher than it was at the lows of last Friday. But we still sit below the 200 day moving average and below the key $50 level (the comfort zone for those producers, namely the shale industry, to fire back up idle capacity).

The weakness in oil has a lot to do with weakness across broader commodities. And broader commodities typically correlates well with what Chinese stocks are doing.

You can see in the chart above, how closely the two track. This bottom in commodities has/had everything to do with the outlook for a big infrastructure spend out of the Trump administration. It’s yet to bubble up toward the top of the action list. With that, the momentum has either stalled on this trade, or it’s a pause before another leg higher in this early stage multi-year rebound. My bet is on the latter. Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

As we discussed last week, we should expect more volatility in markets in the coming months, with the continued discovery surrounding Trump Policies (timing, size) and with UK/EU Brexit negotiations officially opening. That’s a dose of unknowns which should send stocks swinging around quite a bit more than we’ve seen for the past four months.

Remember, on Friday I noted the message the bond market was sending — with market interest rates (U.S. 10 year yields) closing the week, and quarter, at 2.39%. That’s almost a quarter point lower than the high that followed the March rate hike (the third in the Fed’s “normalization” process). And it’s about 10 basis point lower than where the 10 year stood going into the December 2015 rate hike. That’s a negative signal. And I suspect stocks will get that message.

With that said, the first day of the second quarter opened today with a slide in stocks, a slide further in yields and a rise in the price of gold.

When stocks go down, people get nervous and buy downside protection. That tends to spike implied volatility. There’s an index that measures that called the VIX.

Let’s talk about the VIX…

The VIX measures the implied volatility of options on the S&P 500. This is a key component in the price investors pay for downside protection on their portfolios.

So what is implied volatility? Implied volatility measures both actual volatilityand the options market maker community’s expectations (or perception of certainty) about future volatility. When market makers feel confident about the stability in markets, implied vol is lower, which makes the price of options cheaper. When they aren’t confident in stability, implied vol goes up, which makes the price of an option go up. To compensate those that are taking the other side of your trade, for the lack of predictability, you pay a premium.

You can see in the chart below, vol is very, very low — but has been ticking up.

Still, it takes a significant event – a high dose of uncertainty – to create a spike in implied volatility.

That spike tends to correlate well with a sharp slide in stocks. Otherwise, we’re looking at a garden-variety correction in stocks — and that’s what this low vol environment is spelling out.

Following the Fed yesterday, we heard from the Bank of Japan overnight, and the Bank of England this morning. As for Europe, we heard from the ECB last week.

Coming into this week we’ve had this ongoing dynamic, for quite some time, of the Fed going one way on rates (up) and everyone else going the other way (cutting rates, QE, etc.).

That’s been good for the dollar, as global capital tends to flow toward areas with rising interest rates and better growth prospects. That combination tends to mean a rising currency and rising investment values. What really determines those flows though, is the perception of how that policy spread, between countries, may change. Most recently, that perceived change in the spread has been in favor of it growing, i.e. Fed policy tighter or at least stable, while other spots of the world considering even easier on monetary policy.

That divergence in policy has been bad for currencies like the euro, the pound and the yen. But that hit to the currency is part of the recipe. It promotes higher asset prices, better exports and growth. And as Bernanke says, QE tends to make stocks go up, which helps.

Still, those stocks have lagged the strength in U.S. stocks. With that, over the past six months or so, I’ve talked about the opportunities in European and Japanese stocks for a catch up trade.

While U.S. stocks have continued to set new record highs, stocks in Europe and Japan have yet to regain the highs of 2015 — when the global economy was knocked off course, first by slowing China and a surprise currency devaluation, and later by a crash in oil prices.

With that, if you think Trumponomics marked the end of the decade long deleveraging period (post-financial crisis), and that the Fed is signaling that by ending emergency level monetary policy, then the rest of the world should follow. That means the next move in Europe, Japan, the UK will be toward normalization, not toward more emergency policies.

That means the expectations on the policy gap narrows. With that, we may have seen the bottom in the euro. If negative interest rates and an election cycle that has parties that are outright promising to destroy the euro can’t push it to parity, what can? If it can’t go lower, it will go higher.

And if the euro has bottomed and the next move for the central bank in Europe is tapering, the first step toward ending emergency policies, then this stock market in Europe looks the most intriguing for a big catch up trade – still about 20% off of the 2015 highs and well below the pre-crisis all time highs.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Stocks finished the week on record highs. We talked earlier in the week about Trump’s meeting with Japan’s Prime Minister and his economic and finance advisors.

I suspect that Trump will come away, after a weekend in Palm Beach with Abe, learning that Abenomics is good for the U.S., and good global growth and stability (in the current global economic environment).

And one of the keys to success in Abenomics is a weaker yen, which translates to a stronger dollar. As I’ve said, the weak yen has been pulled into the fray with Trump’s tough talk on trade imbalances, but his beef on currency advantage is really directed toward China – not Japan, not Mexico, not even Europe.

With that, and with the assumption that the yen may be pardoned for a while, the dollar bouncing against the yen as we head into the weekend. And it looks like we may see a technical breakout and an even higher dollar, lower yen in our future.

And Japanese stocks look set to break out too, to catch up to the strength of U.S. stocks. The Nikkei is 8% off of the 2015 highs, while U.S. stocks are on record highs, and 8% ABOVE its 2015 highs.

Another catch up trade: German stocks. Despite the growing attention given to the French nationalist candidate, Le Pen, who has been anti-euro and anti-European Union, right or wrong the bond market isn’t showing any new interest in disaster insurance in Europe, nor is the euro.

With that, German stocks look very good, still about 8% from the 2015 highs, and the technical correction clearly ended last summer.

Lastly, let’s take a look at another big sleeper stock market, China…

You can see how Copper is on a big run (up 10% ytd). That typically correlates well with expectations of global growth. Global growth is typically good for China. Of course, China is in the crosshairs of Trump’s fair trade movement, but if you think there’s a chance that more fair trade terms can be a win for the U.S. and a win for China, then Chinese stocks are a bargain here.

Have a great weekend!

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Yesterday we looked at the slide in yields (U.S. market interest rates — the 10-year Treasury yield). That continued today, in a relatively quiet market.

Let’s take a look at what may be driving it.

If you take a look at the chart below, you can see the moves in yields and gold have been tightly correlated since election night: gold down, yields up.

As markets began pricing in a wave of U.S. growth policies, in a world where negative interest rates were beginning to emerge, the benchmark market-interest-rate in the U.S. shot up and global interest rates followed. The German 10-year yield swung from negative territory back into positive territory. Even Japan, the leader of global negative interest rate policy early last year, had a big reversal back into positive territory.

And as growth prospects returned, people dumped gold. And as you can see in the chart above of the “inverted price of gold,” the rising line represents falling gold prices.

Interestingly, gold has been bouncing pretty aggressively since mid December. Why? To an extent, it’s pricing in some uncertainty surrounding Trump policies. And that would also explain the slow down and (somewhat) slide in U.S. yields. In fact, based on that chart above and the gold relationship, it looks like we could see yields back below 2.10%. That would mean a break of the technical support (the yellow line) in this next chart …

Another reason for higher gold, lower yields (i.e. higher bond prices), might be the capital flight in China. Where do you move money if you’re able to get it out in China? The dollar, U.S. Treasuries, U.S. stocks, Gold.

The data overnight showed the lowest levels reached in the countries $3 trillion currency reserve stash in 6 years. That, in large part, comes from the Chinese central banks use of reserves to slow the decline of their currency, the yuan. Of course a weakening yuan only inflames U.S. trade rhetoric.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We’re finishing the first full week under Trumponomics. And it’s been an active one.

It’s clear now that President Trump intends to follow through on his campaign promises. While that’s making waves with the media and with Washington types, it’s creating more certainty about the outlook for growth for the real economy and, therefore, for financial markets.

We close the week with the Dow above 20,000, on new record highs. And as we discussed yesterday, stock markets around the world are rallying too on the prospects of a stronger U.S. economy translating into a stronger global economy. We looked at the charts of Mexican and Canadian stocks yesterday–both of which are sitting on record highs. U.K. stocks are near record highs and German stocks are quickly closing in.

We already know that small business optimism in the U.S. has hit 12-year highs, jumping by the most in since 1980–on Trump’s pro-growth agenda. Today the consumer sentiment report showed sentiment is on the rise too–at 13-year highs.

Let’s talk about the data that we’re leaving behind. Fourth quarter GDP was reported today at just 1.9%. This, more than seven years removed from the failure of Lehman Brothers, an $800 billion stimulus package, seven years of zero interest rates and three rounds of quantitative easing, and the economy is running at about 60% of its normal pace. And even after taking the Fed’s balance sheet from $800 billion to $4.5 trillion, we have inflation running at less than 50% of its normal pace. This malaise is consistent throughout the world. And this is precisely why big, bold fiscal stimulus and structural change is desperately needed, and is being embraced by those that understand the dangers of the stall-speed global economy that has been kept alive by global central bank intervention. As I’ve said, at Dow 20,000, it’s just getting started.

Have a great weekend!

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We talked yesterday about the significance of Dow 20,000. Higher stock prices are fuel for higher stock prices. And higher stock prices are fuel for better economic growth. It’s all self-reinforcing, and we discussed the reasons why stocks can still go much, much higher from here.

As I said, this serves as a validation marker for some that have been waiting to see what the Trump effect might be on markets. If you’ve listened to the consensus voice on Trumponomics, they’ve told you over and over how disastrous the protectionist rhetoric would be the U.S. economy and for the world. I’ve said, given the position of the world, post-Great recession, that Trump’s tough talk is leverage that can be used to ultimately create a fair playing field on trade, which can ultimately lead toward a rebalancing of the global economy — something that has to take place to put the world back on a path of sustainable growth, and end the cycle of booms and busts. That’s a win-win for everyone.

We’ve seen it working with industry leaders (they’re playing ball). And expect a similar outcome on the geopolitical front. This approach doesn’t work in normal times, but we’re not in normal times, almost a decade after the onset of the global financial crisis — where global economies remain weak and vulnerable.

With this in mind, Mexico and Canada are in focus with the announcement this week of the NAFTA renegotiation, the wall and the Keystone pipeline. And the media is hot and heavy on the cancellation of a trip to the White House by the Mexican President.

Let’s take a look at how Trumponomics is working for our two biggest trading partners, thus far.

This is the chart of the dollar versus the Mexican Peso. The rising line represents the dollar strengthening and the peso weakening, and vice versa.

If we look at this exchange rate as a gauge of trade partner health, we’ve seen the peso hit hard through the campaigning period under the protectionist fears of a Trump administration – and post election. That has represented a negative-scenario message for Mexico. But since the inauguration, the peso has been strengthening (not weakening), even as President Trump signed an executive order to renegotiate NAFTA. The message behind that usually means: the U.S. does better, Mexico does better.

What about Mexican stocks? Similar story. As the U.S. stock market is on record highs, the Mexican stock market too, is sitting on record highs. When the prospects are better for U.S. growth, our trade partners do better.

What about Canada? The same story. The Canadian stock market is on record highs.

The worst-case scenarios are good fodder for attracting readers and viewers. That’s why the media is obsessively focused on the potential negatives. But with some perspective on the bigger picture, and with respect to the position of the world coming out of the crisis period, those worst-case scenarios have lower probabilities than they think, and would have you believe. That’s why reality is crafting a very different story.

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

President Trump officially took office today. From the close of business on November 8th, as people across the country were still voting, the S&P 500 has climbed 6% – from election night through today. The dollar index has risen 2.8. The broad commodities index is up 6%. The 10 year Treasury note is down 4% — which means the yield is UP from 1.80% to about 2.50%.

His policy agenda has clearly been a game changer.

But if you recall, the broad sentiment going into the election was that a Trump Presidency would cause a stock market crash. These were people that weren’t calibrating the meaningful shift in sentiment that came from projecting pro-growth policies in a world that has been starved for growth. That event (the election) alone did more to cure the global deflation risk than the trillions of dollars that central banks have been pouring into the global economy.

But many still aren’t buying it. I don’t often read financial news. I’d rather look at the primary sources (the data or hear from the actors themselves/ the horse’s mouth) and interpret for myself. But today, I had a look across the web. Four of the five top headlines on a major financial news site, on inauguration day, ranged from negative to doom-and-gloom — all laying blame on the dangers of Trump.

Because Trump has talked tough on trade, the common threat most refer to is a potential trade war. But remember, Trump has also talked tough on U.S. companies moving jobs overseas. Thus far, he hasn’t created enemies, he’s gotten concessions and has created allies. He’s used leverage, and he’s negotiated win-wins. Expect him to do the same with trade partners. With pro-growth policies coming down the pike and a meaningful pop in U.S. economic growth coming, no country, especially in the current state of the global economy, will want to be locked out of trade with the United States.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.