Yesterday CNBC hosted their Delivering Alpha conference. This conference is primarily an opportunity for investors to hear views and ideas from some of Wall Street’s best.

However, the bigger picture geopolitical environment is far more important for the market at the moment, than what a big hedge fund manager thinks about valuation (for example).

On that note, there were some interesting takeaways from yesterday’s event. As we discussed yesterday, we heard from Larry Kudlow, the White House Chief Economic Advisor. And we also heard from Steve Bannon, the former White House Chief Strategist.

Bannon has been given plenty of unappealing labels by the media in recent years, but his perspective on the White House game plan and how it’s executing is invaluable. I think everyone would agree that the communication on the economy and foreign policy could be handled better by the White House.

And Bannon articulates the issues in the Trump plan, maybe better than anyone. It’s an interview everyone should watch (here’s a link).

As we’ve discussed here in my ProPerspectives piece since I started writing this nearly three years ago, the trade war is nothing new. And it’s all about China. As Bannon said, China has been waging an economic and cyber war with the U.S. for the better part of the past 25 years. Now they’ve run into a wrecking ball in Trump: someone with the leverage and the credibility to act on threats to end the gutting of global economies (including the U.S. and other major developed market economies). Bannonsays we’re in the early stages of a “reorientation of the supply-chain around freedom loving countries.”

As we’ve discussed, the best reflection of China’s strategic response to Trump’s pressure is their currency. What are they doing with it? They continue to walk it lower every day. This is a signal that they have no options–playing by the rules and getting slower economic growth isn’t an option for the ruling regime in China. They can only fight back by offsetting tariffs with a weaker currency. And that may ultimately lead to blocking China trade completely.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We’ve talked about the case for a shakeout in Amazon. It was up big today on news that it would be buying a big online pharmacy.

That worked to curtail the slide in the stock (for now). But it only exacerbates the building regulatory scrutiny and the President’s wrath against Amazon’s developing monopoly and power (much of which has been garnered overtime from the unfair advantages Amazon has enjoyed from operating as an internet company).

If there’s one thing we know about Trump as a President, he’s done what he says he’s going to do. And he’s had plenty of verbal threats directed squarely at Amazon. We can only assume that he will carry out the offensive he’s been promising — against a company that has crushed industries by price wars.

On a similar note, let’s talk about China. As we’ve discussed quite a bit, China’s rapid economic ascent in the world came through currency manipulation. They held their currency down, to underprice the world on exports. And as the world stood by and watched (and bought lots of stuff from them), they became the world’s second largest economy, and the accumulated the largest war chest of foreign currency reserves.

China is to the world, as Amazon is to corporate America. And Trump is attempting to deal with them both head on.

Interestingly, China is quietly fighting back, via the currency. The go to tool in China is currency devaluation.

That’s what they’ve been doing over the past three months. And that has accelerated in just the past 10 days – they’ve devalued by almost 4% against the dollar. This is something to watch closely. A big one-off devaluation out of China would be a geopolitical cage rattling.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We have a lot of geopolitical noise surrounding markets.

Let’s step through them:

1) Yesterday, we discussed the Trump trade threats with China:

How is it playing out?

We have an economy that is leading the global economic recovery. China wants and needs to be part of it. Trump’s bark, with the credibility to bite, is creating movement. It’s creating compliance. That’s becoming a very positive catalyst for global economy and for geopolitical stability (the exact opposite of what the experts have predicted these tactics would produce).

2) We’ve talked about the shock-risk developing in Europe. A coalition government forming in Italy, with an “Italy first” approach to the social and economic agenda, has created some flight of Italian bond market capital toward safety. This has people skittish about another blowup threat of the euro zone.

How is it playing out?

The last time Italy was on default/blow up watch, the 10 year yields were 7% (unsustainable levels). At those levels, the ECB had to intervene.

This recent move in the Italian bond markets leaves yields at just 2.4% …

This looks like Grexit, Brexit and the Trump election. It creates leverage for the third largest economy in the European Union (excluding Britain). In this case, we may see it result in a loosening of fiscal constraints in the European Union – and an EU wide fiscal stimulus plan to follow the lead of the U.S.

3) The North Korean nuclear threat …

How is it playing out?

Eight months ago, North Korea launched a missile over Japan. Markets barely budged, and the world continued to turn. Now, we’ve quickly gone from an imminent threat to potential denuclearization. And now a meeting has been cancelled. With that, on the continuum of this relationship, I’d say it’s closer to its best point, rather than its worst.

Bottom line, these risks should do little to stop the momentum of the economy and the stock market.

There has been a lot of attention over the past couple of days on China and trade relations.

China has moved down tariffs on auto and auto parts imports. And a source today said the government has “encouraged” China’s largest oil refiner to buy more U.S. crude oil. Based on the reports, China is now taking about 8 times the daily volume of U.S. crude imports, compared to averages a few months ago.

These are concessions! This is a distinct power shift. Not long ago, the world was afraid to rattle the cage of China. They (global trading partners) tiptoed around touchy matters like Chinese currency manipulation prior to the global financial crisis a decade ago, and even more so after the crisis.

But now, you can see the leverage that has been created by Trump. This is exactly what we talked about the day after the election.

Here’s an excerpt from my November 9, 2016 ProPerspectives note, back when the experts were predicting Draconian outcomes for poking the China giant: “As we’ve seen with Grexit and Brexit, the votes came with dire warnings, but have resulted in creating leverage. Trump’s complaints about China are right. And a threat of slapping a tariff on Chinese goods creates leverage from which to negotiate.”

Now, we have an economy that is leading the global economic recovery. China wants and needs to be part of it. And we have a President that has a loud bark, and the credibility to bite. And that is creating movement. Let’s revisit, also from one of my 2016 notes, why this China negotiation is so important …

TUESDAY, SEPTEMBER 27, 2016

China’s biggest and most effective tool is and always has been its currency. China ascended to the second largest economy in the world over the past two decades by massively devaluing its currency, and then pegging it at ultra-cheap levels.

Take a look at this chart …

In this chart, the rising line represents a weaker Chinese yuan and a stronger U.S. dollar. You can see from the early 1980s to the mid-1990s, the value of the yuan declined dramatically, an 82% decline against the dollar. China trashed its currency for economic advantage—and it worked, big time. And it worked because the rest of the world stood by and let it happen.

For the next decade, the Chinese pegged its currency against the dollar at 8.29 yuan per dollar (a dollar buys 8.29 yuan).

With the massive devaluation of the 1980s into the early 1990s, and then the peg through 2005, the Chinese economy exploded in size. It enabled China to corner the world’s export market, and suck jobs and foreign currency out of the developed world. This is precisely what Donald Trumpis alluding to when he says ‘China is stealing from us.’

China’s economy went from $350 billion to $3.5 trillion through 2005, making it the third largest economy in the world.

This next chart is U.S. GDP during the same period. You can see the incredible ground gained by the Chinese on the U.S. through this period of mass currency manipulation.

And because they’ve undercut the world on price, they’ve become the world’s Wal-Mart (sellers to everyone) and have accumulated a mountain for foreign currency as a result. China is the holder of the largest foreign currency reserves in the world, at more than $3 trillion dollars (mostly U.S. dollars). What do they do with those dollars? They buy U.S. Treasurys, keeping rates low, so that U.S. consumers can borrow cheap and buy more of their goods—adding to their mountain of currency reserves, adding to their wealth and depleting the U.S. of wealth (and the cycle continues).

This is the recipe for big trade imbalances — lopsided economies too dependent upon either exports or imports. And it’s the recipe for more cycles of booms and busts … and with greater frequency.”

Again, China has to be dealt with. And we’re starting to see signs of progress on that front. Good news.

We’ve talked about the stock market’s discomfort with the 3% mark in rates. People have been concerned about whether the U.S. economy can withstand higher rates–the impact on credit demand and servicing. That fear seems to be subsiding.

But often the risk to global market stability is found where few are looking. That risk, now, seems to be bubbling up in emerging market currencies. We have a major divergence in global monetary policies (i.e. the Fed has been normalizing interest rates while the rest of the world remains anchored in emergency level interest rates). That widening gap in rates, creates capital flight out of low rate environments and in to the U.S.

That puts upward pressure on the dollar and downward pressure on these foreign currencies. And the worst hit in these cases tend to be emerging markets, where foreign direct investment in these countries isn’t very loyal (i.e. it comes in without much commitment and leaves without much deliberation).

You can see in this chart of the Brazilian real, it has been ugly …

Oil has become the potential breaking point here. At $40-oil maybe these countries hang in there until the global economic recovery heats up to the point where they can begin raising rates without crushing growth (and with a closing rate gap, their currencies begin attracting capital again). But at $70-oil, their weak currencies make their dollar-denominated energy requirements very, very expensive. They’ve had nearly a double in oil over the past ten months, and a 15% drop in their currency since January (in the case of Brazil).

Something to watch, as a lynchpin in this EM currency drama, is the Hong Kong dollar. Hong Kong has maintained a trading band on its currency since 2005 that is now sitting on the top of the band, requiring a fight by the central bank to maintain it. If they find that spending their currency reserves on defending their trading band is a losing proposition, and they let the currency float, then we could have another shock event for global markets, as these EM currencies adjust and their foreign-currency-denominated debt becomes a default risk. This all may force the rest of the global economy to start following the Fed’s lead on interest rates earlier then they would like to (to begin closing that rate gap, and avoid a shock event).

As we discussed yesterday, stocks have fully recovered the decline that people were attributing to Trump’s trade barrier announcement last week.

With that, the tariff hysteria seems to have subsided a bit, as they struggle for evidence to support their hyperbole. Perhaps people may start acknowledging that we are now in a higher volatility environment, and that we will be slowly working out of this recent price correction until corporate earnings and economic growth data start confirming the benefits of tax cuts.

Interestingly, they seem to hate the trade threat, far more than the love the tax incentives and the pro-growth initiatives. And while trade is a complicated issue, everyone seems to suddenly have an expert opinion on it. And everyone is an expert on the Smoot-Hawley Act (which, by the way was a tariff on over 20,000 goods) and depression-era economics.

If they indeed were reflective about the economy, I think they would agree that we (and the world) desperately need growth initiatives to save us from terminal central bank life support (which wouldn’t be so terminal given they have fired all of their bullets to keep us afloat as long as they did). And they would know that we are in for a perpetual cycle of booms and busts (repeat of the credit bubble and burst) if the trade imbalances (mainly between China overproducing and the U.S. overconsuming) ultimately are not corrected.

Now, as more of the conversation on trade turns more toward China, I want to revisit an excerpt from my note in December of 2016 (when Trump was President-elect):

MONDAY, DECEMBER 19, 2016 — “While many think Trump will provoke a military conflict, that’s far from a certainty. With the credibility to act, however, Trump’s tough talk on China creates leverage. And from that leverage, there may be a path to a mutually beneficial agreement, where the U.S. can win in trade with China, and China can win. But it may get uglier before it gets better. In the end, growth solves a lot of problems. A hotter growing U.S. economy (driven by reform and fiscal stimulus), will ultimately drive much better growth in the global economy. And China has a lot to gain from both. Though in a fair-trade environment, they won’t get as much of the pie as they’ve gotten over the past two decades. But it has the chance of leading to a more balanced and sustainable economy in China, which would also be a win for everyone.”

Now, why not just focus on China now? Because they will continue to abuse other countries. And those open trade channels will still allow that product to enter the U.S. As we discussed yesterday, the global economy has been damaged by China’s currency/trade policy, yet the rest of the world has been relying on the U.S. to lead the fight. They need to join the fight to create the leverage to make it ultimately work – so that the global economy can find a sustainable path of recovery and robust growth.

Stocks continue to swing around, and in wider ranges than we’ve seen in a while. We should expect this type of action following a sharp technical correction–a correction that shook many of the players out of the market, that were contributors to suppressing volatility in recent years (the short vol ETFs among them).

Now, as I’ve said in the past, people always search for a story to fit the price. Despite the fact that stocks have been swinging around, with little or no story for them to attribute, they were quick to pounce on Trump’s announcement about steel tariffs, and have since blamed every down tick in the stock market for it. And they’ve run wild with trade war scenarios. For those trying to capitalize on that fear scenario, it shows how uninformed, naive or intellectually dishonest they are (most the latter). They like to evaluate it as if there is no context or history.

Where have they all been the past 20-plus years?

China has been manipulating the global markets through their cheap currency policy for the better part of the past 25 years. In pinning down their currency, they cornered the world’s export market. And in the process, they emerged as the second largest economy in the world. They also accumulated the world’s largest reserve of foreign currencies, which they plowed into global credit markets (mainly our Treasurys) to fuel cheap credit, which ultimately led to the global credit bubble and bust (the global financial crisis). We buy their cheap stuff. They take our dollars and buy Treasurys, supplying more credit to us to buy more of their cheap stuff. And so the cycle goes.

Currencies are the natural balancing mechanism to prevent this bubble/global imbalance from forming. When freely traded in an open economy, the market demand for yuan, given the aggressive growth in the economy, would have driven the value of China’s currency higher, making its exports less attractive, and therefore slowing their breakneck growth and wealth accumulation in China, and its ability to fuel global credit. But of course, the government determines the value of the yuan, and keeping the currency cheap is part of the economic model in China (still).

For those that fear retaliation (a historic response to protectionism), this is retaliation… for 20 years of wealth transfer.

The tariff threats address metals, but the currency is a key tool that makes it all happen. For those that like to play it as a political football, Trump is not the architect of the plan. A staunch democratic Senator from New York, Charles Schumer, led the push in Congress for a bill in 2005 to impose a 35% tariff on China. That’s what ultimately led to the agreement by the Chinese to allow their currency to weaken (somewhat). With that, I want to revisit my note from late September 2016 (prior to the elections) for a little more backstory on Why Trump Is Right About China (read more here).

If you are hunting for the right stocks to buy on this dip, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

Yesterday we talked about the case for commodities and the opportunity for a rotation into commodities stocks.

The valuation of commodities relative to stocks has only been this disconnected (stocks strong, commodities weak) twice, historically over the past 100 years: at the depths of the Great Depression in the early 30s and toward the end of the Bretton Woods currency system.

That supports the case that we’re in the early days of a bull market in commodities, especially considering where we stand in the global economic recovery, underpinned by the “reflation” focus at both the monetary and fiscal policy levels. It’s a recipe for hotter demand for commodities.

With that, let’s take a look at a few charts as we close the week.

Copper

We talked about copper yesterday. This continues to ring the bell, alerting us that better economic growth is coming – maybe a boom.

Copper is up 6.5% in the past two weeks, back of $3 and closing in on the highs of the year – which is a three year high. And remember, we looked at the potential break of this big six-year downtrend back in August. That has broken, retested and confirms the trend change.

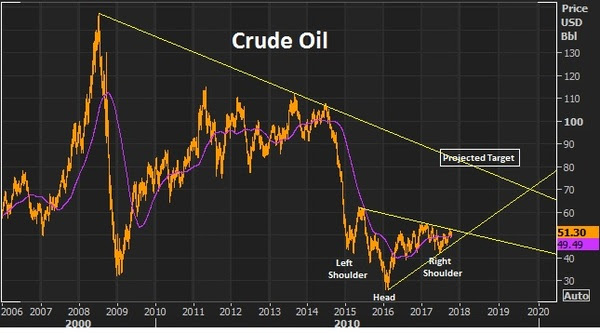

Crude Oil

We talked about the fundamental case for oil this week. And we looked at the technical case, as it made a brief test of the 200 day moving average and quickly bounced back. It’s up about 4% on the week.

We have this inverse head and shoulder (in the chart below) that projects a move back to the low $80s. And as part of that technical picture, we’re setting up for a break of a big two-year trendline that should open the doors to a move back into the $70+ oil area.

Iron Ore

Iron ore was the biggest mover of the day – up 6% today. This has been a deeply depressed market through the post-financial crisis era. In addition to the broad commodities weakness, iron ore prices have suffered from the dumping of poor quailty iron ore by Chinese producers. Those times seem to be changing.

This week there was a fraud claim on a big Japanese steel maker for fudging it’s quality data. Keep an eye on this one as it could lead to more, and could lead to a supply disruption in industrial metals.

Then today we had Chinese data that showed record imports of iron ore. This is a signal that there’s both an envirionmental movement and an anti-dumping movement against low grade iron ore that has been influencing supply and prices (and crushing producers). This big Chinese data point is also in line with the message copper is sending: perhaps the Chinese economy is doing better than most think.

With that, let’s take a look at a few charts as we close the week. The valuation of commodities relative to stocks has only been this disconnected (stocks strong, commodities weak) twice, historically over the past 100 years: at the depths of the Great Depression in the early 30s and toward the end of the Bretton Woods currency system.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Stocks are sliding more aggressively today. Wall Street and the media always have a need to assign a reason when stocks move lower. There have been plenty of negatives and uncertainties over the past seven months — none of which put a dent in a very strong opening half for stocks.

But markets don’t go straight up. Trends have retracements. Bull markets have corrections. And despite what many people think, you don’t need a specific event to turn markets. Price can many times be the catalyst.

If we look across markets, it’s safe to say it doesn’t look like a market that is pricing in nuclear war. Gold is higher, but still under the highs of a month ago. The 10 year yield is 2.21%. Two weeks ago, it was 2.22%. That doesn’t look like global capital is fleeing all parts of the world to find the safest parking place.

Now, on the topic of North Korea, the media has found a new topic to obsess about– and to obsessively denounce the administration’s approach. With that, let’s take a look at the Trump geopolitical strategy of calling a spade a spade.

As we know, Mexico was the target heading into the election. Trump’s tough talk against illegal immigration and drug trafficking drew plenty of scrutiny. People feared the protectionist threats, especially the potential of alienating the U.S. from its third biggest trading partner. We’re still trading with Mexico. And the U.S. is doing better. So is Mexico. Mexican stocks are up 11% this year. The Mexican currency is up 13% this year.

China has been a target for Trump. He’s been tough on China’s currency manipulation and, hence, the lopsided trade that contributed heavily to the credit crisis. Despite all of the predictions, a trade war hasn’t erupted. In fact, China has appreciated its currency by 5% this year. That’s a huge signal of compliance. That’s among the fastest pace of currency appreciation since they abandoned the peg against the dollar more than 12 years ago (which was China’s concession to threats of a 30% trade tariff that was threatened by two senators, Schumer and Graham, back in 2005). And even in the face of a stronger currency (which drags on exports, a key driver of the economy), stocks are up 5% in China through the first seven months of the year.

Bottom line: It’s fair to say, the tough talk has been working. There has been compromise and compliance. So now Trump has stepped up the pressure on North Korea, and he has been pressuring China, to take the side of the rest of the world, and help with the North Korea situation – and through China is how the North Korea threat will likely get resolved.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

The past few days we’ve looked at the run up in bitcoin. Remember, I said: “If you own it, be careful. The last time the price of bitcoin ran wild, was 2013. It took about 11 days to triple, and about 18 days to give it all back. This time around, it’s taken two months to triple (as of today). ”

It looks to be fueled by speculation, and likely Chinese money finding its way out of China (beating capital controls). And yesterday we talked about the potential disruption to global markets that could come with a crash in bitcoin prices.

I suspect that’s why gold is finally beginning to move today, up almost 1%, and among the biggest movers of the day as we head into the long holiday weekend (an indication of some money moving to gold to hedge some shock risk).

Remember yesterday we looked at the chart on Chinese stocks back in 2015 and compared it to bitcoin. The speculative stock market frenzy back thin was pricked when the PBOC devalued the yuan later in the summer.

Probably no coincidence that bitcoin’s recent acceleration happened as Moody’s downgraded China’s credit rating this week for the first time since 1989 (an event to take note of). Yesterday, the PBOC was thought to be in buying Chinese stocks (another event to take note of). And this morning, the PBOC stepped in with another currency move! Historically, major turning points in markets tend to come with some form of intervention. Will a currency move be the catalyst to end the bitcoin run, as it did the runup in Chinese stocks two years ago?

Let’s take a look at what the currency move overnight means …

Keep in mind, the currency is China’s go-to tool for fixing problems. And they have problems. The economy is crawling around recession like territory. The debt was just downgraded. And they’ve had a tough time managing capital flight. As an easy indicator: Global stocks are soaring. Chinese stocks are dead (flat on the year).

Remember, their rapid economic ascent in the world came through exports (via a weak currency). The move overnight is a move back toward tying its currency more closely to the dollar. Which, if this next chart plays out, will also weaken the yuan compared to other big exporting competitors in the world.

That should help the Chinese economic outlook, which may help stem the capital flight (which has likely been a significant contributor to bitcoin’s rise).

Yesterday we talked about the case for commodities and the

Yesterday we talked about the case for commodities and the