July 19, 2017, 4:00 pm EST Invest Alongside Billionaires For $297/Qtr

As we know, inflation has been soft. Yet the Fed has been moving on rates, assuming that they have room to move away from zero without counteracting the same data that is supposed to be driving their decision to increase rates.

Thus far, after four (quarter point) increases to the Fed funds rate, the moves haven’t resulted in a noticeable tightening of financial conditions. That’s mainly because the interest rate market that most key consumer rates are tied to have remained low. Because inflation has remained low.

A key contributor to low inflation has been low oil prices (though the Fed doesn’t like to admit it) and commodity prices in general that have yet to sustain a recovery from deeply depressed levels (see the chart below).

But that may be changing.

Commodities have been lagging the rest of the “reflation” trade after the value of the index was cut in half from the 2011 highs. Remember, we looked at this divergence between the stocks and commodities last month. Commodities are up 6% since.

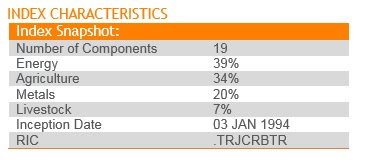

Things are picking up. Here’s the makeup of the broadly followed commodities index.

You can see, energy has a heavy weighting. And oil, with another strong day today, looks like a break out back to the $50 level is coming.With today’s inventory data, we’ve now had 12 out of the past 14 weeks that oil has been in a draw (drawing down on supply = bullish for prices). And with that backdrop, the CRB index, after being down as much as 13% this year, bottomed following the optimistic central bank commentary last month, and is looking like it may be in the early stages of a big catch-up trade. And higher oil (and commodity prices in general) will likely translate into higher inflation expectations.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

May 15, 2017, 4:00pm EST Invest Alongside Billionaires For $297/Qtr

Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick. Last week we discussed the building support for a next leg higher in commodities prices. China is clearly a very important determinant in where commodities go. And with the news last week about cooperation between the Trump team and China, on trade, we may have the catalyst to get commodities moving higher again.It just so happens that oil (the most traded commodity in the world) is rebounding too, on the catalyst of prospects of an OPEC extension to the production cuts they announced last November.In fact, overnight, Saudi Arabia and Russia said they would do “whatever it takes” to cut supply (i.e. whatever it takes to get oil prices higher). Oil was up big today on that news.When you hear these words spoken from policy-makers (those that can dictate outcomes), it should get everyone’s attention. Those are the exact words uttered by ECB head Mario Draghi, that ended the bond market assault in Spain and Italy that were threatening the existence of the euro and euro zone. The Spanish 10-year yield collapsed from 7.8% (unsustainable borrowing rate for the Spanish government, and threatening imminent default) to 1% over the next three years — and the ECB, while threatening to buy an unlimited amount of bonds to push those yields lower, didn’t have to buy a single bond. It was the mere threat of ‘whatever it takes’ that did the trick.

As for oil: From the depths of the oil price crash last year, remember, we discussed the prospects for a huge bounce. Oil prices at $26 were threatening to undo the trillions of dollars of work central banks and governments had done to stabilize the global economy. Central banks couldn’t let it happen. After a series of coordinated responses (from the BOJ, China, ECB and the Fed), oil bottomed and quickly doubled.

Also at that time, two of the best oil traders in the world were calling the bottom and calling for $70-$80 oil by this year (Pierre Andurand and Andy Hall). Another commodities king that called the bottom: Leigh Goehring.

Goehring, one of the best commodities investors on the planet, has also laid out the case for $100 oil by next year. He says he’s “wildly bullish” oil in his recent quarterly investor letter at his new fund, Goehring & Rozencwajg.

Goehring argues that the IEA inventory numbers are flawed. He thinks oil the market is already over-supplied and is in a draw, as of May of last year. With that, he thinks the OPEC cuts will ultimately exacerbate the deficit and send prices aggressively higher. He says “we remain ‘wildly’ bullish and believe that there is a very high probability of oil prices reaching triple digits in the first half of 2018.”

Follow This Billionaire To A 172% WinnerIn our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Join us today and get our full recommendation on this stock, and get your portfolio in line with our BILLIONAIRE’S PORTFOLIO.

|

September 6, 2016, 3:30pm EST

As we headed into the holiday weekend, stocks were sitting near record highs, yields were hanging around near record lows, and oil had been sinking back toward the danger zone (which is sub $40).

In examining the relationship of those three markets, each has a way of influencing the outcome and direction of the others.

First, the negative scenarios: A continued slide in oil would soon sink stocks again, and send yields (the interest rate outlook) falling farther. Cheap oil, in this environment, has dire implications for the energy business, which has a cascading effect, starting with banks, which effects credit and the dominos fall from there.

What about stocks? When stocks are falling, in this environment, it’s self-reinforcing. Lower stocks, equals souring sentiment, equals lower stocks.

What about yields? As we’ve seen, lower yields are supposed to promote spending and borrowing. But, in this environment, it comes with trepidation. Lower yields, especially when much of the world’s government bond markets are in negative yield territory, is having a stifling effect on economic activity, as many see it as a signal of another recession coming, or worse.

Now, for the positive scenarios. Most likely, they all come with intervention. That shouldn’t be surprising.

We’ve already seen the kitchen sink thrown at the stock market. From a monetary policy standpoint, the persistent Fed jockeying through much of the past seven years has now been handed over to Japan and Europe. QE in Europe and Japan continues to promote stability, which incentivizes the flow of capital into stocks (the only liquid alternative for return in a zero and negative interest rate world).

And we’ve seen them influence oil prices as well, through easing, currency market intervention, and likely the covert buying of oil back in February/March of this year (through China, ETFs via the BOJ or an intermediary Japanese bank). Still, OPEC still swings the big ax in the oil market, and it’s been OPEC intervention that has rigged oil prices to cheap levels, and it looks increasingly likely that they will send oil prices higher through a policy move. The news that Russian and Saudi Arabian might coordinate to promote higher oil prices, sent crude 5% higher on Monday.

As for yields, this is where the Fed is having a tough time. They want yields to slowly climb, to slowly follow their policy guidance. But the world hasn’t been buying it. When they hiked for the first time in December, the U.S. 10 year yield went from 2.25%, to 2.30% (for a cup of coffee) and has since printed new record lows and continues to hang closer to those levels than not (at 1.53% today). Lower yields makes it even harder for them to hike because it’s in the face of weaker sentiment.

Last week, we looked at the U.S. 10 year yield. It was trading in this ever narrowing wedge, looking like a big break was coming, one way or the other, following the jobs report on Friday. It looks like we may have seen the break today (lower), following the week ISM data this morning.

What could swing it all in the positive direction? Fiscal intervention.

As we discussed on Friday, the G20 met over the weekend. With world government leaders all in the same room, we know the geopolitical tensions have been rising, relationships have been dividing, but first and foremost priority for everyone at the table, is the economy.

Even those opportunistically posturing for influence and power (i.e. Russia, China), without a stable and recovery global economy, the political and domestic economic outlook is bleak. So we thought heading into the G20 that we could get some broader calls for government spending stimulus was in order.

The G20 statement did indeed focus heavily on the economy. They said, “Our growth must be shored up by well-designed and coordinated policies. We are determined to use all policy tools – monetary, fiscal and structural – individually and collectively to achieve our goal of strong, sustainable, balanced and inclusive growth. Monetary policy will continue to support economic activity and ensure price stability, consistent with central banks’ mandates, but monetary policy alone cannot lead to balanced growth. Underscoring the essential role of structural reforms, we emphasize that our fiscal strategies are equally important to supporting our common growth objectives.”

Keep an ear open for some foreshadowing out of Europe to promote fiscal stimulus – the spot it’s most needed. That would be a huge catalyst for “risk assets” (i.e. commodities, stocks, foreign currencies) and would probably finally signal the top in the bond market.

After a fairly quiet August, we have a full docket of central meetings in the weeks ahead, starting this week. The European Central Bank meets on Thursday.

Join us here to get all of our in-depth analysis on the bigger picture, and our carefully curated stock portfolio of the best stocks that are owned and influenced by the world’s best investors.

September 2, 2016, 12:00pm EST

This time last month, the famed oil trader—and oil bull—Andy Hall was dealing with a sub-$40 oil market again. And he was again explaining losses to investors in his multi-billion dollar hedge fund.

A guy that has made a career, and hundreds of millions of dollar in personal wealth, picking tops and bottoms in oil, had entered 2016 coming off his worst year ever. And 2016 started even worse.

I’ve talked about the oil price bust extensively, at the depths of the decline in January and February. While most were glorifying the benefits of a few extra bucks in the pockets of consumers from low gas prices, we walked through the ugly outcome of persistently low oil prices. It would be another global financial crisis, as failing energy companies and defaulting oil producing countries would crush banks, and the dominos would fall from there. Unfortunately, the central banks don’t have the ammunition to pull the world back from the edge of disaster for a second time.

With that, central banks stepped in with more easing in the face of the oil price threat, and oil bounced sharply.

Hall’s fund bounced sharply too, running up nearly 25% for the year, by the end of June. But he gave a lot of it back by the time July ended. And now, again, oil is closer to $40 than $50. Thanks to a report yesterday, that oil supplies were bigger than expected, the price of crude has fallen 10% since Friday of last week.

Hall was the Citigroup C +0.13% oil trader who made billions of dollars for the bank energy trading arm, Phibro, in the early-to mid-2000s. He was one of the first to load up on oil futures in 2002, when oil was sub-$30, on the thesis that a boom in demand was coming from China.

He reportedly made $800 million in profits for Citi in 2005 from his original bullish bet. He then made more than $1 billion in 2008 for the bank, as oil prices soared to $147 a barrel and then abruptly crashed. He profited handsomely from both sides, earning a payout from Citi of more than $100 million.

So he’s a guy that has been very right about turning points, and big trends. And he’s been pounding the table for much higher oil prices. He thinks oil prices are in for a “violent reversal” (higher). With an important OPEC meeting scheduled for later this month, Hall, in a past investor letter, reminded people how powerful an OPEC policy shift can be. In 1986, the mere hint of an OPEC policy move sent oil up 50% in just 24 hours.

In our Billionaire’s Portfolio, we’re positioned in deep value stocks that have the potential to do multiples of the broader market—all stocks that are owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and get yourself in line with our portfolio. You can join here.

2/2/16

It’s unimaginable that governments and central banks that have coordinated and committed trillions of dollars in guarantees, backstops, commitments and outright bailouts will stand by and let weak oil prices (rigged by OPEC) undo everything they’ve done over the past seven years to create stability and manufacture a global economic recovery.

Oil represents a systemic threat to the global economy. Just as housing created a cascade of trouble, through the global financial system, then through countries, the oil price crash can do the same.

When you see forecasts of $20 oil or lower, and some of it is coming from Wall Street, these people should also follow by telling you to buy guns and build a bunker, because that’s what you would need if oil went there and stayed there.

Not to mention, if they believe in that forecast, they should be formulating a plan for what they will do to make a living going forward, because their employers will likely go bust in that scenario.

The persistence of lower oil, especially less than or equal to $20 oil, would financially ruin the U.S. energy sector. Oil producing countries would be next, starting with Russia (and ultimately reaching the big OPEC nations). A default in Russia would create tremors in countries that hold Russia sovereign debt and rely on trade with Russia. Remember the fallout from the Asian Crisis? A default in Russia was the catalyst. Oil driven sovereign defaults would create a massive flight of global capital to safety and global credit/liquidity would dry up, again. All of this would put the world’s banks back on the brink of failure, just as we experienced in 2008. The only problem is, this time around, the global economy cannot absorb another 2008. Governments and central banks have fired their bullets and have nothing left to fend off another near global economic apocalypse.

With that, we have to believe that this crash in oil prices will not persist, especially when it’s being rigged by OPEC. Intervention now (or soon) is easy (relatively speaking) and returns the world to the recovery path. Intervention too late will require more resources than are available.

To follow the stock picks of the world’s best billionaire investors, subscribe at Forbes Billionaire’s Portfolio.

What’s the solution? An OPEC cut in production has a way of swinging oil in the other direction dramatically. Back in 1986, just a hint of an OPEC cut swung oil by 50% in just 24 hours. This assumes that the pressure builds on OPEC and they realize that the game of chicken that they are playing with U.S. producers has put themselves, also, precariously close to an endpoint.

Alternatively, we made the case last week that either China, the Bank of Japan or the European Central Bank could step in and outright buy commodities as a policy response to their ailing economies. Both the ECB and the BOJ in the past two weeks have said that there are “no limits” to what they can buy as part of their respective QE programs. That would immediately put a floor under crude, and likely global stocks, commodities and put in a top in sovereign bonds. Remember, when China stepped in, bought up and hoarded dirt cheap commodities in 2009, oil went from $32 to above $100 again.

So what’s the latest on oil?

Chart

This morning, the threat intensified. Oil dropped 5%, trading below the very key level of $30 per barrel. It was driven by an earnings report from the huge oil and gas company, BP. It reported a $6.5 billion loss. The company followed with an announcement of 7,000 job cuts by the end of 2017. Shares of BP stock are now trading back to 2010 levels, when the company was facing the prospects of bankruptcy after the fall–out from its gulf oil spill. This is one of the largest oil and gas companies in the world trading at levels last seen when people were speculating on its demise.

With the move in oil this morning, global stocks took another hit. Commodities were hit and sovereign debt yields were hit (with U.S. 10–year yields falling below 1.9%).

While there is a lot of talk about China and concerns there, clearly oil is what is dictating markets right now.

Take a look at this chart of oil vs. the S&P 500…

You can see the significant correlation historically in the price of oil and stocks. And you can see where oil and stocks came unhinged back in July 2014. The dramatic disconnect started in November 2014 (Thanksgiving Day) when an OPEC meeting concluded. The poorer members of OPEC called for production cuts. Saudi Arabia blocked the requests. That set off the plunge in oil prices.

You can see clearly in this chart where the price of oil is projecting the S&P. And stocks at those levels suggest the scenario we described above (global apocalypse round 2).

Again, a capitulation from OPEC is probably less likely. More likely, a central bank steps in to become an outright buyer of commodities (especially cheap oil). For those that have been shorting oil (and remain heavily short), either scenario would put them out of business quickly.

At this stage, OPEC is not just in a price war with U.S. shale producers, but it’s playing a game of chicken with the global economy. We’ve had plenty of events over the past seven years that have shaken confidence and have given markets a shakeup – European sovereign debt, Greece potentially leaving the euro, among them. In Europe, we clearly saw the solution. It was intervention. Oil prices are creating every bit as big a threat as Europe was; it’s reasonable to expect intervention will be the solution this time as well.

Bryan Rich is co-founder of Billionaire’s Portfolio, a subscription-based service that empowers average investors to invest alongside the world’s best billionaire investors. To follow the stock picks of the world’s best billionaire investors, subscribe at Billionaire’s Portfolio.