Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

For perspective: As of the close yesterday, the Nasdaq was up 18% year to date (just five months in). Gold was in the middle of a three year range. Market interest rates (the U.S. 10-year government bond yield) was just above the middle of the range of the past four years. The dollar was not far off its strongest levels in 15 years.

Today the media has explicitly printed the headline of impeachment for Trump (actually, they’ve run those headlines a various times over the past several months). Nonetheless, stocks (the S&P 500) today are off by 1.6%.

This gets the bears very excited. I saw the story about consumer debt, surpassing 2008 levels, floating all over the internet today. People tried to make the bubble connection — implying another debt crisis was coming.

The real story: Total household indebtedness finally surpassed the previous peak from 2008. That’s precisely what the Fed was attempting to do with zero interest rates. Make existing debt cheaper to manage, and at some point, break the psychology of the debt burden and get people borrowing (at ultra-cheap rates), investing and spending again. Otherwise, our economy and the world economy would have gone into a deflationary spiral.

That said, as I’ve found in my 20 years in this business, people tend to find a story to fit the price. The story hadn’t been fitting the price for much of the past six months. Today, it seems pretty easy. See the chart below of stocks ….

We had the first breakdown of the Trump trend in March, but all it could muster was about a 3% correction. This looks much more like a technical correction (a double top, and trend break today) – than a Trump impeachment trade. I suspect with the earnings catalyst behind us, this is the start of a deeper technical correction, which is healthy in a bull market. And it may take significant progress made in tax reform to see new highs in the broad stock indicies. We shall see.This next chart is the dollar index. This too had a significant trend break today. This translates into a higher euro, which would spell out a story where Europe is improving and the ECB is able in start discussing exit from QE.

What about the Trump/Comey saga? Aren’t people dumping dollars because of that? Not likely. If that were potentially destabilizing to the U.S., it would be destabilizing to the global economy, and people would buy dollars not sell them.

With that in mind, here’s gold. Gold sits on the brink of a big trend break (higher). When looking at gold and the dollar, it’s important to remember this: back in the heat of the crisis, gold and the dollar moved together, higher! That’s opposite of the traditional correlation. They moved higher together because people bought gold and they bought dollars (and dollar denominated assets, like Treasuries) as they viewed it the safest alternative in the world to park money – with the chance of getting it back.

With a break higher in gold looking imminent, and the dollar looking lower, it looks like a more traditional relationship. It’s not communicating crisis.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

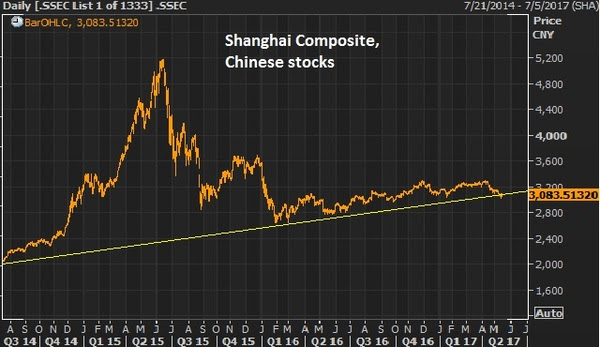

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

Let’s take at the chart…

While the agreements out of China were said not to touch on steel and industrial metals, the first steps of cooperation could put a bottom in the slide in metals like copper and iron ore. These are two commodities that should be direct beneficiaries in a world with better growth prospects, especially with prospects of a $1 trillion infrastructure spend in the U.S. With that, they had a nice run up following the election but have backed off in the past couple of months, as the infrastructure spend appeared not to be coming anytime soon.

Here’s copper and the S&P 500…

Trump policies are bullish for both. Same said for iron ore…

This is right in the wheelhouse of Wilbur Ross, Trump’s Secretary of Commerce. He’s made it clear that he will fight China’s dumping of steel on the U.S. markets, which has driven steel prices down and threatened the livelihood of U.S. steel producers. Keep an eye on these metals next week, and the stocks of producers.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

Over the past few days, some of the most influential investors in the world have publicly shared views on some of their best ideas.First, over the weekend, it was Buffett at his annual shareholders meeting. The take away, as I said yesterday, “stocks are dirt cheap” if you think rates will stay low for longer (i.e. below long term averages). His assumption in that statement is that the Fed’s benchmark rate goes to 3ish% and done – well below the long run average neutral rate of 5%.

In addition, he was quite vocal on Apple, a stake he picked up as others were selling in fear in the first half of last year (i.e. being greedy when others are fearful). And he doubled his stake earlier this year, now holding north of $20 billion worth of the stock. The analyst community thinks Apple is a juggling act, with balls that will drop if they don’t come up with another revolutionary product every quarter. Buffett thinks Apple is cheap even if they don’t have another single new invention in the future. Why? Because they’ve developed a services business around their hardware that has quickly become one of the biggest and fastest growing businesses in the world.

Remember, back on February 1, I made the case for why Apple could double. You can see that here. It’s gone from a $560 billion company to an $800 billion company since we added it in our Billionaire’s Portfolio early last year. Even at $154 a share (today’s levels) if we strip out the quarter of a trillion dollars in cash, we get the existing business for 12 times earnings.

Now, let’s talk about one of the big ideas presented yesterday at the annual Sohn Conference in New York, where many of top billionaire investors and hedge fund managers give their outlook on the stock market, the economy and talk about their favorite long and/or short picks.

Billionaire investor Jeff Gundlach, who oversees the world’s largest bond fund likes selling the S&P 500 against emerging market stocks. He thinks value is distorted relative to global GDP. But it’s more a view on undervaluation of EM, rather than overvaluation of U.S. stocks. He took to Twitter to defend that view…

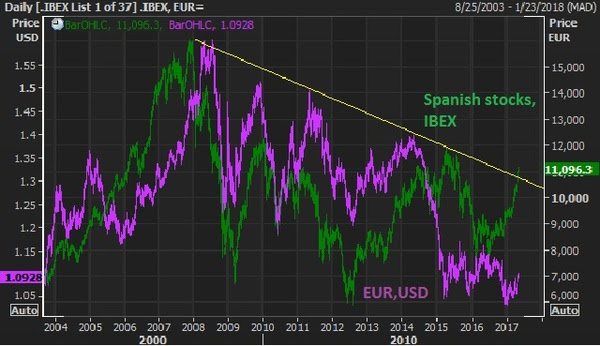

Assuming a stable to improving world economy, emerging market stocks have lagged and offer a great opportunity to catch up with the strength in the U.S. stock market. It also requires that emerging market currencies are a good bet against the dollar, if policy makers around the world are able to follow the lead of the Fed, where rising interest rate cycles follow. This is a very similar view to the one we discussed yesterday, where Spanish stocks (supported by a stronger euro) present a big catch up trade opportunity (to the tune of about 40% to revisit the 2007 highs), with the destabilization risk of the French elections in the rear-view mirror.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

Brexit. Russia. Trump’s protectionist threats. Trump’s inability to get policies legislated. The French election.

The bears, those looking for a recession around the corner and big slide in stocks, are losing ammunition for the story.

With the threat of instability from the French election now passed, these are two of the more intriguing catch-up trades.

In the chart above, the green line is Spanish stocks (the IBEX). U.S., German and UK stocks have not only recovered the 2007 pre-crisis highs but blown past them — sitting on or near (in the case of UK stocks) record highs. Not only does the French vote punctuate the break of this nine year downtrend, but it has about 45% left in it to revisit the 2007 highs. And the euro, in purple, could have a dramatic recovery with the cloud of French elections lifted, which was an imminent threat to the future of the single currency.Next … Japanese stocks. While the attention over the past five months has been diverted toward U.S. politics and policies, the Bank of Japan has continued with unlimited QE. As U.S. rates crawl higher, it pulls Japanese government bond yields with it, moving the Japanese market interest rate above and away from the zero line. Remember, that’s where the BOJ has pegged the target for it’s 10 year yield – zero. That means they buy unlimited bonds to push the yield back down. That means they print more and more yen, which buys more and more Japanese stocks.

The Nikkei has been one of the biggest movers over the past couple of weeks (up almost 10%) since it was evident that the high probability outcome in the French election was a Macron win.Again, German, U.S., and UK stocks are at or near record highs. The Nikkei has been trailing behind and looks to make another run now, with 25,000 in sight.If you need more convincing that stocks can go much higher, Warren Buffett reiterated over the weekend that this low interest rate environment and outlook makes stocks “dirt cheap.” Last year he made the point that when interest rates were 15% [in the early 1980s], there was enormous pull on all assets, not just stocks. Investors have a lot of choices at 15% rates. It’s very different when rates are zero (or still near zero). He said, in a world where investors knew interest rates would be zero “forever,” stocks would sell at 100 or 200 times earnings because there would be nowhere else to earn a return.

Buffett essentially said at zero interest rates into perpetuity, the upside on the stock market (and any alternative asset class with return) is essentially infinite, as people are forced to find return by taking risk. Why you would buy a treasury bond that has no growth, and little-to-no yield and the same or worse balance sheet than high quality dividend stock.

This “forcing of the hand” (pushing investors into return producing assets) is an explicit objective by the interest rate policies of the Fed and the other major central banks of the world. They need us to buy stocks. They need us to spend money. They need economic growth.

If you have an brokerage account, and can read a weekly note from me, you can position yourself with the smartest investors in the world. Join us in The Billionaire’s Portfolio.

As we discussed last week, we should expect more volatility in markets in the coming months, with the continued discovery surrounding Trump Policies (timing, size) and with UK/EU Brexit negotiations officially opening. That’s a dose of unknowns which should send stocks swinging around quite a bit more than we’ve seen for the past four months.

Remember, on Friday I noted the message the bond market was sending — with market interest rates (U.S. 10 year yields) closing the week, and quarter, at 2.39%. That’s almost a quarter point lower than the high that followed the March rate hike (the third in the Fed’s “normalization” process). And it’s about 10 basis point lower than where the 10 year stood going into the December 2015 rate hike. That’s a negative signal. And I suspect stocks will get that message.

With that said, the first day of the second quarter opened today with a slide in stocks, a slide further in yields and a rise in the price of gold.

When stocks go down, people get nervous and buy downside protection. That tends to spike implied volatility. There’s an index that measures that called the VIX.

Let’s talk about the VIX…

The VIX measures the implied volatility of options on the S&P 500. This is a key component in the price investors pay for downside protection on their portfolios.

So what is implied volatility? Implied volatility measures both actual volatilityand the options market maker community’s expectations (or perception of certainty) about future volatility. When market makers feel confident about the stability in markets, implied vol is lower, which makes the price of options cheaper. When they aren’t confident in stability, implied vol goes up, which makes the price of an option go up. To compensate those that are taking the other side of your trade, for the lack of predictability, you pay a premium.

You can see in the chart below, vol is very, very low — but has been ticking up.

Still, it takes a significant event – a high dose of uncertainty – to create a spike in implied volatility.

That spike tends to correlate well with a sharp slide in stocks. Otherwise, we’re looking at a garden-variety correction in stocks — and that’s what this low vol environment is spelling out.

With the Fed’s third rate hike this week in the post-financial crisis era, let’s take a look at how market rates have reponded.

Here’s a chart of the U.S. 10 year government bond yield.

On December 16, 2015, the Fed moved for the first time. The 10-year traded up to 2.33% that day and didn’t see that level again for 11-months. Despite the fact that the Fed forecasted four hikes over the next twelve months, the bond market wasn’t buying it. A month later, the fall in oil prices turned into a crash. And the 10 year yield printed a new record low at 1.32%, just under the crisis lows.

On December 14, 2016, the Fed made the second move. This was after they had spent the better part of the last nine months walking back on what they thought would be their 2016 hiking campaign. The difference? Trump was elected the new President and he was already fueling confidence from talk of big, bold fiscal stimulus. The Fed’s big hiking campaign was placed back on the table. The high in yields the day the Fed made hike #2 was 2.58%. The next day it put in a top at 2.64% that we have not seen since.

And, of course, this past week, we’ve had hike #3. The 10 year yield traded up to 2.60% that day (Wednesday) and we haven’t seen it since, despite the fact that the Fed has continued to tell us another couple of hikes this year, and that the economy is doing well, expect about three hikes a year through 2018. Yields go out at 2.50% today.

So why aren’t market rates screaming? The 10 year yield should be 3.5%+ by now. And consumer rates should be surging. Is it the Bank of Japan, the European Central Bank and China buying our Treasuries, keeping a cap on yields? Is it that the market doesn’t believe it and thus the yield curve is flattening (which would project recession)? Probably a bit of both. The important point is that the Fed absolutely cannot do what they are doing if they think they will push the 10 year yield up to 3.5%+, and fast.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

The last data point for everyone to obsess about going into next week’s Fed meeting will be this Friday’s jobs report.

But as I’ve said for quite a while, the jobs data has been good enough in the Fed’s eyes for quite some time. Nonetheless, they’ve had many, many balks along the path of normalizing rates over the past couple of years. Here’s a look at a chart of the benchmark payrolls data we’ll be seeing Friday.

You can see in this chart, the twelve-month moving average is 195k. The three-month moving average is 182k. The six-month moving average is 182k. This is all fairly consistent with historical/pre-crisis levels.

So the numbers have been solid for quite some time, even meeting and exceeding the Fed’s targets, especially when it comes to the unemployment rate (4.7% last). However, when the Fed’s targets have been met, the Fed has moved the goal posts. When those goal posts were then exceeded, the Fed found new excuses to justify their decisions to avoid the path of aggressive hikes/normalization of rates that they had guided.

Among those excuses: When jobs were trending at 200k and unemployment breached 5%, the Fed started to acknowledge underemployment. Then the lack of wage growth became the focus. Then it was macro issues. To name a few: It’s been soft Chinese economic data, a Chinese currency move, Russian geopolitical tensions, collapsing oil prices, Brexit and weak productivity.

And just prior to the election last year, the Fed became, confusingly, less optimistic about the U.S. economic outlook, which was the justification to ratchet down the aggressive projected path for rates.

I suspected last year, when they did this that they were making a strategic pivot, to set expectations for a much easier path for rates, in hopes to keep people spending, borrowing and investing — instead of promoting a tighter path, which proved for the better part of two years (prior to the election) to create the opposite effect.

Remember, Bernanke (the former Fed Chair) even wrote a public piece on this last August, criticizing the Fed for being too optimistic in its projections for the path of interest rates. By showing the market/the world an expectation that rates will be dramatically higher in the coming months, quarters and years, Bernanke argued in his post that this “guidance” has had the opposite of the desired effect – it’s softened the economy.

A month later, in September, in Yellen’s post-FOMC press conference, she said this in response to why they didn’t raise rates: “the decision not to raise rates today and to wait for some further evidence that we’re continuing on this course is largely based on the judgment that we’re not seeing evidence that the economy is overheating.” Safe to argue, the economy isn’t overheating, still.

Again, as I said on Friday, the only difference between now and then, is the prospects of major fiscal stimulus, which is precisely what the Fed claims to be ignoring/leaving out of their forecasts – a believe it when I see it approach, allegedly.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

We closed last Friday with another new weekly record high on the Dow. But we closed with an all-time record low in the German 2-year bund. That development in Europe, weighed on U.S. yields, pulling yields down here from 2.5 to 2.31%.

So we had this divergence between what was happening in stocks and what the bond market was communicating. The bond market was telling us there was growing concern about danger to European economic stability, and therefore global economic stability, in the upcoming French elections. Stocks were telling us, growth is king – the ultimate problem solver, and growth is coming.

With that, Trump’s address to Congress on Tuesday night became a major sentiment gauge/the arbiter on which would win out, based on the perception of whether or not the Trump administration could execute on its economic plans.

The vote was “affirmative” for the growth story. Stocks gapped higher to new record highs (closing this week at another weekly record high). And the bond market turned on a dime, following Trump on Tuesday night, and have been climbing since. German yields have bounced. And U.S. yields have bounced. That leads us up to today’s speech from Janet Yellen.

There has been a tremendous shift in the past week in the expectations for a March rate hike. It’s gone from a 27% chance of a March 15 rate hike being priced in last Friday. By Wednesday morning, after Trump’s speech, it was 70%! And we close out the week with an 80% chance of a hike this month.

That additional bump came today on a speech and Q&A session from Janet Yellen today. Here’s the expectations bar she chose to set: She said the Fed would likely be moving faster than it had in 2015 and 2016. It should be said that they only hiked once in 2015 and 2016 because their forecasts proved grossly overly optimistic and they had to adjust on the fly. So they’ve already told us, back in December, that they think it will be three times this year. That’s faster than one. And today she reiterated that today.

And today she also said that if the data continued to improve as they forecast, they can hike this month.

Now, they have a post-FOMC meeting press conference scheduled FOUR more times this year (March, June, September and December). Despite what they suggest, that they could hike at any meeting and just call an impromptu press conference, they would be crazy to introduce such a surprise in markets. Stability and confidence work in their favor. Surprises threaten stability and confidence.

So if they indeed hike three times, they have a narrow window. And if they think they need to hike faster, because perhaps fiscal policy accelerates growth and inflation, they may need to keep the December meeting open for a fourth hike.

But, Yellen and company have recently gone out of their way to tell us that they are not even factoring in fiscal stimulus and deregulation (growth policies) into their view on the economy. They’ll believe when they see it and take that information as it comes, which puts them in an even more vulnerable position to needing more tightening this year, if you take them at their word and trust their forecasting abilities.

So with that in mind, why has the Fed become so bulled up on interest rate picture since December? Is it because the inflation and jobs data has gotten that much better? The unemployment rate has been below 6% (the Fed’s original target) since September of 2014 and below 5% for the past year. And the core inflation rate has been above 2% since November of 2015, which includes all year last year, when the Fed was reversing course on its promises for a big tightening year. That’s near normal employment in the Fed’s eyes and above its target for inflation – a clear signal to normalize interest rates. But they’ve barely budged.

Why? Because last year the global economy looked vulnerable. With that, they threw every other guiding data point out the window and went back to playing defense. And as recent as August of last year, the Fed messaging was quite dovish. What’s the biggest difference between now and then? The prospects of major fiscal stimulus – precisely what they say they are leaving out of their forecasts for now.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Markets are quiet as we head into President Trump’s address to Congress tonight. As we’ve discussed over the past week or so, the markets seem to have run the course on the outlook of fiscal stimulus and regulatory reform within an environment of a gradual rise in interest rates.

That “expectation” backdrop seems to be pretty well priced in. Now, it’s a matter of detail and timing, and that puts the new President squarely in focus for tonight.

We’ve already heard from his Treasury Secretary last week that tax reform wouldn’t be coming until August-ish. And he said we shouldn’t expect that big growth bump from Trumponomics until 2018. That’s been the first real downward management of the expectations that have been set over the past three months.

What hasn’t been discussed much is the big infrastructure spend, which is really at the core of the pro-growth policies of the Trump administration. For years, the Fed has been begging Congress for help in stabilizing the economy and stimulating growth in it — from the FISCAL side.

Given the wounds of the debt crisis, it was politically unpalatable for Congress. They ignored the calls. And as a result, just six months ago we (and the rest of the world) were dangerously close to slipping back into crisis. Only this time, the central banks would not have had the ammunition to fight it.

So now we have Congress with the will and position to act. It’s a matter of detailing a plan and getting it moving. Of the many positive things that could come from tonight’s speech by President Trump, details and timeline on fiscal stimulus would be the biggest and most meaningful.

The bickering about deficits and debt will continue, but a big stimulus package will happen — it has to happen. A government spending led growth pop is, at this stage, the only chance we have of returning to a sustainable path of growth and ultimately reducing the debt load down the line, which now is about 100% of GDP. A move back to 80% of GDP would make the U.S. debt load, relative to the rest of the world, a non-issue.

Follow The Lead Of Great Investors Like Warren Buffett In Our Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

The big event of the week will be President Trump’s speech to Congress tomorrow. We know the pro-growth agenda of the Trump administration. We know the framework is in place to make it happen (with a Republican controlled Congress). That alone has led to a “clear shift in the environment” as Ray Dalio has called it (head of the biggest hedge fund in the world) – I agree.

But we’re at a point now, with European elections approaching and political risk rising there, and with the reality setting in that execution on fiscal stimulus from Trumponomics won’t be coming quickly, markets are calming down a bit. As we discussed last week, yields are falling back, following the lead of record level lows set in the German 2-year bund yield (in deeply negative territory). That dislocation in the German government bond market, as other key market barometers have been pricing in bliss, has come as a warning signal.

Another event of interest: Warren Buffett’s annual letter was released over the weekend, and he was on CNBC for a long interview this morning.

First, I want to revisit his letter from last year: Last year, in the face of an oil price crash, and a stock market that had opened the year with the worse decline on record, Buffett addressed the fears and uncertainty in markets. He said the growth trajectory for America has been and will continue to be UP. “America’s economic magic remains alive and well.”

And the growth trajectory has to do with two key factors: Improvements in productivity and innovation.

On productivity, he said:“America’s population is growing about .8% per year (.5% from births minus deaths and .3% from net migration). Thus 2% of overall growth produces about 1.2% of per capita growth. That may not sound impressive. But in a single generation of, say, 25 years, that rate of growth leads to a gain of 34.4% in real GDP per capita. (Compounding effects produce the excess over the percentage that would result by simply multiplying 25 x 1.2%.) In turn, that 34.4% gain will produce a staggering $19,000 increase in real GDP per capita for the next generation. Were that to be distributed equally, the gain would be $76,000 annually for a family of four. Today’s politicians need not shed tears for tomorrow’s children. All families in my upper middle–class neighborhood regularly enjoy a living standard better than that achieved by John D. Rockefeller Sr. at the time of my birth. Transportation, entertainment, communication or medical services.”

On innovation, he said:“A long–employed worker faces a different equation. When innovation and the market system interact to produce efficiencies, many workers may be rendered unnecessary, their talents obsolete. Some can find decent employment elsewhere; for others, that is not an option. When low–cost competition drove shoe production to Asia, our once–prosperous Dexter operation folded, putting 1,600 employees in a small Maine town out of work. Many were past the point in life at which they could learn another trade. We lost our entire investment, which we could afford, but many workers lost a livelihood they could not replace. The same scenario unfolded in slow–motion at our original New England textile operation, which struggled for 20 years before expiring. Many older workers at our New Bedford plant, as a poignant example, spoke Portuguese and knew little, if any, English. They had no Plan B. The answer in such disruptions is not the restraining or outlawing of actions that increase productivity. Americans would not be living nearly as well as we do if we had mandated that 11 million people should forever be employed in farming. The solution, rather, is a variety of safety nets aimed at providing a decent life for those who are willing to work but find their specific talents judged of small value because of market forces. (I personally favor a reformed and expanded Earned Income Tax Credit that would try to make sure America works for those willing to work.) The price of achieving ever–increasing prosperity for the great majority of Americans should not be penury for the unfortunate.”

And, finally on stocks, he said (my paraphrase): Overtime, with the above growth dynamic in mind, stocks go up.“In America, gains from winning investments have always far more than offset the losses from clunkers. (During the 20th Century, the Dow Jones Industrial Average — an index fund of sorts — soared from 66 to 11,497, with its component companies all the while paying ever–increasing dividends.”

What a difference a year makes. This time, he releases his letter into a stock market that’s UP 6% on the year already. And there’s new leadership and policy change underway.

So all of this in the above was written a year ago, what does he think now? In his letter released over the weekend, Buffett AGAIN addresses the fears and uncertainties in markets.

We discussed on Friday the stages of a bull market which slowly moves from the state of broad pessimism, to skepticism to optimism and finally to euphoria, which tends to end the bull market. But as Paul Tudor Jones says (one of the great macro investors), the “last third of a great bull market is typically a blow-off, whereas the mania runs wild and prices go parabolic” (i.e. euphoria can last for a while).

The fact that Buffett is still addressing concerns about valuations and the future of the American economy, is more evidence that we’re far from euphoria (bubble-like territory that some like to often talk about) and were probably more like the area between skepticism to optimism.

About Valuation: As we’ve discussed many times here my daily Pro Perspectives piece, when rates are low, historically, valuations run higher than normal (a P/E of 20 or better). At a ten year yielding at 2.4% and fed funds at 75 basis points (well below the long run average) the forward P/E on the S&P is just 17.8x. That’s still cheap, relative to the alternative of owning bonds. That incentivizes money to continue to flow into stocks. And if we apply a 20 P/E earnings estimates for the next twelve months, we get about 12% higher on the S&P 500.

Now, let’s hear from the legend himself on the topic: Buffett said this morning, “We’re not in bubble territory, if interest rates were 7% or 8% then these prices would look exceptionally high, but you measure everything against interest rates, measured against interest rates, stocks are on the cheap side compared to historic valuations.”

By the way, on that “valuation note” for stocks, as you may recall I made the case early this month for why Apple (the largest component of the S&P 500) was cheap (Is Apple A Double From Here?). What does Buffett think? Buffett disclosed that he’s doubled his position in Apple since the beginning of the year. It’s now his second largest position at $17 billion. He thinks Apple will be the first trillion dollar company. Full disclosure: We own Apple in our Billionaire’s Portfolio along with Buffett and his fellow billionaire investor David Einhorn. We’re up 30% since adding it in March of last year.

Follow The Lead Of Great Investors Like Warren Buffett In Our Forbes Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

Yesterday we talked about the disconnect between the daily drama from the media in Washington (doom and gloom), and what the markets have been communicating (an economic expansion is underway). Today, you might think that connection is happening — the doom and gloom scenario is finally being realized in markets. Probably not.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

As we ended this past week, stocks remain resilient, hovering near highs. The Nasdaq had a visit to the 200-day moving average intraweek for a slide of a whopping (less than) 1%, and quickly it bounced back.It’s a Washington/Trump policies-driven market now, and while the media carries on with narratives about Russia and the FBI, the market cares about getting health care done (which there was progress made last week), getting tax reform underway, and getting the discussion moving on an infrastructure spend.We looked at oil and commodities yesterday. Chinese stocks look a lot like the chart on broader commodities. With that, the news overnight about some cooperation between the Trump team and China on trade has Chinese stocks looking interesting as we head into the weekend.

Over the past few days, some of the most influential investors in the world have publicly shared views on some of their best ideas.First, over the weekend, it was Buffett at his annual shareholders meeting. The take away, as I said yesterday, “stocks are dirt cheap” if you think rates will stay low for longer (i.e. below long term averages). His assumption in that statement is that the Fed’s benchmark rate goes to 3ish% and done – well below the long run average neutral rate of 5%.

Over the past few days, some of the most influential investors in the world have publicly shared views on some of their best ideas.First, over the weekend, it was Buffett at his annual shareholders meeting. The take away, as I said yesterday, “stocks are dirt cheap” if you think rates will stay low for longer (i.e. below long term averages). His assumption in that statement is that the Fed’s benchmark rate goes to 3ish% and done – well below the long run average neutral rate of 5%.