We had new record highs again in the Dow today. But remember, yesterday we talked about this dynamic where stocks, commodities and the dollar were strong. But a missing piece in the growing optimism about growth has been yields.

Clearly the 10 year at 2.40ish is far different than the pre-election levels of 1.75%-1.80%. But the extension was quick and has since been a non-participant in the full-on optimism vote given across other key markets.

Why? While stocks can get ahead of better growth, yields can’t in this environment. Higher stocks can actually feed higher growth. Higher yields, on the other hand, can kill it.

But there’s something else at work here. As we know Japan’s policy to target the their 10 year at zero provides an anchor to our interest rates, as the BOJ is in unlimited QE mode. Some of that freshly produced liquidity, and the money displaced by their bond buying, undoubtedly finds a happier home in U.S. Treasuries (with a rising dollar, and a 2.4% yield). That caps yields.

But in large part, the quiet drag on U.S. yields has also come from the rising risks in Europe. The election cycle in Europe continues to threaten a populist Trump-like movement, which is very negative for the European Union and for the survival of the single currency (the euro). That creates capital flight, which has been contributing to dollar strength and flows into the parking place of U.S. Treasuries (which pressures yields, which is keeping mortgage and other consumer rates in check).

These flows are also showing up clearly in the safest bond market in Europe: the German bunds. The 2-year German bund hit an all-time record LOW, today of -91 basis points. Yes, while the U.S. mindset is adjusting for the idea of a 3%-4% growth era, German yields are reflecting crisis and money is plowing into the safest parking place in Europe. The spread between German and French bonds are reflecting the mid-2012 levels when Italy and Spain where on the brink of insolvency — only to be saved by a bold threat/backstop from the European Central Bank.

We talked last week about the prospects for higher gold and lower yields as questions arise about the execution of (or speed of execution) Trump’s growth policies, some of the inflation optimism that has been priced in, may begin to soften. That would also lead to a breather for the stock market. I suspect we will begin to see the coming elections in Europe also contribute to some de-risking for the next couple of months. We already have a good earnings season and some solid economic data and optimism about the policy path priced in. May be time for a dip. But as I’ve said, it would create opportunities– to buy any dip in stocks, and sell any rally in bonds.

To peek inside the portfolio of Trump’s key advisor, join me in our Billionaire’s Portfolio. When you do, I’ll send you my special report with all of the details on Icahn, and where he’s investing his multibillion-dollar fortune to take advantage of Trump policies. Click here to join now.

Stocks continue to make new highs – five consecutive days of higher highs in the Dow. The Trump administration continues to make new news. And the Fed continues to become less important. Those have been the themes of the week.

Today was the deadline for all big money managers to give a public snapshot of their portfolios to the SEC (as they stood at the end of Q4). So let’s review why (if at all) the news you read about today, regarding the moves of big investors, matters.

Remember, all investors that are managing over $100 million are required to publicly disclose their holdings every quarter. They have 45 days from the end of the quarter to file that disclosure with the SEC. It’s called a form 13F.

First, it’s important to understand that some of the moves deduced from 13F filings can be as old as 135 days. Filings must be made 45 days after the previous quarter ends.

Now, there are literally thousands of investment managers that are required to report on a 13F. That means there are thousands of filings. And the difference in manager talent, strategies, portfolio sizes, motivations and investment mandates runs the gamut.

Although the media loves to run splashy headlines about who bought what, and who sold what, to make you feel overconfident about what you own, scared about what they sold, anxious, envious or all a combination of it all. The truth is, most of the meaningful portfolio activity is already well known. Many times, if they are big stakes, they’ve already been reported in another filing with the SEC, called the 13D.

With this all in mind, there are nuggets to be found in 13Fs. Let’s revisit how to find them, and the take aways from the recent filings.

I only look at a tiny percentage of filings—just the investors that have long and proven track records, distinct approaches, and who have concentrated portfolios. That narrows the universe dramatically.

Here’s what to look for:

Clustering in stocks and sectors by good hedge funds is bullish. Situations where good funds are doubling down on stocks is bullish. This all can provide good insight into the mindset of the biggest and best investors in the world, and can be a predictor of trends that have yet to materialize in the market’s eye.

For specialist investors (such as a technology focused hedge fund) we take note when they buy a new technology stock or double down on a technology stock. This is much more predictive than when a generalist investor, as an example, buys a technology stock or takes a macro bet.

The bigger the position relative to the size of their portfolio, the better. Concentrated positions show conviction. Conviction tends to result in a higher probability of success. Again, in most cases, we will see these first in the 13D filings.

New positions that are of large, but under 5%, are worthy of putting on the watch list. These positions can be an indicator that the investor is building a position that will soon be a “controlling stake.”

Trimming of positions is generally not predictive unless a hedge fund or billionaire cuts by a substantial amount, or cuts below 5% (which we will see first in 13D filings). Funds also tend to trim losers into the fourth quarter for tax loss benefits, and then they buy them back early the following year.

As for the takeaways from Q4 filings, the best names had built stakes in financials. That’s not surprising given that the Trump win had all but promised a “de-Dodd Franking” of the banking system, especially with the line-up of former Goldman alum that had been announced by late December.

The other big notable in the filings: Warren Buffett’s stake in Apple.

Remember, as we headed into the Brexit vote last year, the broad market mood was shaky. Markets were recovering after the oil price crash, and the unknowns from Brexit had some running for cover. Meanwhile, some of the best investors were building as others were trimming. They were buying energy near the bottom. They were buying health care. And while many were selling the most dominant company in the world, Warren Buffett was buying from them. The guy who has made his fortunes buying when others are selling, did it again with Apple. He was buying near the bottom last summer, and in the fourth quarter he ramped up big time, more than tripling his stake to a $6.6 billion position.

Follow The Lead Of Great Investors Like Warren Buffett In Our Billionaire’s Portfolio

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and follow the world’s best investors into their best stocks. Our portfolio was up over 27% in 2016. Click here to subscribe.

Stocks are hitting new record highs today. That includes the Dow, the S&P 500 and the Nasdaq.

We’ve now seen about 60% of the earnings for Q4, and earnings are very good. As we’ve discussed, earnings guidance and consensus views are made to be beaten. Factset says that, on average, about 67% of S&P 500 companies beat the consensus view on earnings. For Q4, that number, as of last Friday, was 65%.

More importantly, the earnings growth rate for Q4 is +4.6% thus far. That’s better than the 3.1% that was predicted, coming into the earnings season. And that’s the first two consecutive quarters of year-over-year positive EPS growth in a couple of years.

So we have positive earnings surprises driving stocks higher. And finally, revenue growth is coming. After six consecutive quarters of revenue contraction, earnings for U.S. companies had a second consecutive quarter of growth. And the quarters ahead should be much better.

Clearly, in the weak growth environment, the focus has clearly been cutting costs, refinancing debt, selling non-core assets, and buying back shares. That’s all a recipe for juicing EPS, even though revenue growth is sluggish, if existent.

So for all of the people that are constantly hand wringing about the levels of the stock market, ask them this: What happens when you take these companies that are growing earnings by optimizing margins in a 1% growth world, and you give them 3%-4% economic growth? Earnings go up. What happens when you take a profitable company and cut the tax burden by 15 to 20 percentage points? Earnings go up.

When earnings go up, price to earnings goes down. And valuations can become very, very cheap.

We have companies that have been forced to streamline to survive. And now we’re in the early days of a regime shift, where tax cuts will work for them, deregulation will work for them, and a big infrastructure spend will pop demand, to actually fuel some revenue growth.

Below is a nice chart from Yardeni. You can see the flattish revenue growth, but earnings divergence over the past five years.

On the right hand axis, next year’s earnings on the S&P 500 are expected around $133. That doesn’t take into account the impact of a corporate tax cut, which Standard & Poors research has suggested could bump that number up to the mid $150s ($1.31 added for every 1% cut in the corporate tax rate). That would dramatically widen the revenue, earnings divergence — or make the closing of this gap that much more aggressive.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

I talked yesterday about the Fed. As I said, I think we’ll find that the Fed will shift gears again to stay behind the curve on inflation, to let the economy run a little hot. They met today and it was a non-event. They said nothing to build momentum on their rate hike from December.

The news of the day has been Apple (NASDAQ:AAPL) earnings. People over the past couple of years have been calling for the decline in Apple. They’ve said it’s topped. They can’t innovate in the post-Steve Jobs era. The iPhone was magic. But reproducing magic isn’t easy. Once you put a computer in everyone’s pocket, there’s not much more they can do to it with it. These are all of the quips about Apple’s peak. They may be right. But Apple’s peak, at least as a stock, is greatly exaggerated.

They reported a huge positive surprise on earnings yesterday after the close. The stock was up 6% on the day. But even before that, I suspect it has become a much loved stock in the past two months in the “smart money” investor community.

We should see in the coming weeks, as big investors disclose their positioning for the end of Q4, Apple will have returned to a lot of portfolios again. Warren Buffett, an investor that has made his fortune buying when others are selling, built a big stake at the lows of the year last year. And it’s a perfect Buffett stock.

It’s incredibly cheap compared to the market.

The stock still trades at 15x earnings. Much cheaper than the market. Apple trades at 13x next year’s projected earnings. The S&P 500 trades at 16.5x. What about Apple’s monster cash position? Apple has even more cash now — a record $246 billion. If we excluded the cash from the valuation, Apple market cap goes down from $675 billion to $429 billion. That would equate to Apple trading at closer to 9x earnings. Though not an “apples to apples” that valuation would group Apple with the likes of these S&P 500 components that trade around 9 times earnings, like: Dow Chemical, Prudential Financial, Bed Bath & Beyond, a Norwegian chemical company (LBY), and Hewlett Packard Enterprise. It’s safe to say no one is debating whether or not Hewlett Packard is at the pinnacle of its business. Yet, if we strip out the cash in Apple, AAPL shares are trading closer to an HPE valuation.

Add to that, Apple now has a fresh catalyst coming in, Trump policies. The new President Trump is incentivizing Apple (and others) to bring offshore cash hoards back home with a flat 10% tax. And Apple makes money – a lot of it. A cut in the corporate tax rate will be a boon for earnings. Two years ago, Carl Icahn argued that Apple should use (a lot more of) their cash to buyback shares – and, with that, valued the stock at double its current levels.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

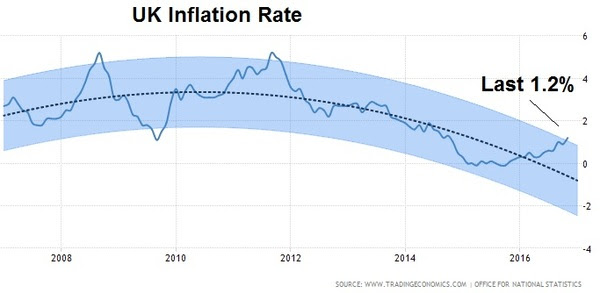

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

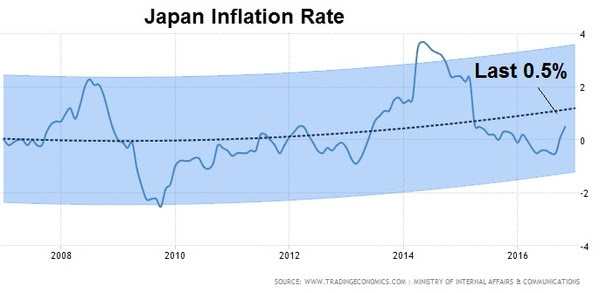

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We talked yesterday about the bad start for global markets in 2016. It was led by China. Today, it was a move in the Chinese currency that slowed the momentum in markets. Yields have fallen back. The dollar slid. And stocks took a breather.

China’s currency is a big deal to everyone. It’s the centerpiece of the tariff threats that have been levied from the U.S. President-elect. I’ve talked quite a bit about that posturing (you can see it again here: Why Trump’s Tough Talk On China May Work).

As we know, China, itself, sets the value of its currency every day. It’s called a managed float. They determine the value. And for the past two years, they’ve been walking it lower — weakening the yuan against the dollar. That’s an about face to the trend of the prior nine years. In 2005, in agreement with their major trading partners (primarily the U.S.), they began slowly appreciating their currency, in an effort to allay trade tensions, and threats of trade sanctions (tariffs).

So what happened today? The Chinese revalued its currency — pegged ithigher by a little more than a percent against the dollar. That doesn’t sound like a lot, but as you can see in the chart, it’s a big move, relative to the average daily volatility. That became big news and stoked a little bit of concern in markets, mostly because China was the sore spot at the open of last year, and the PBOC made a similar move around this time, when global marketswere spiraling.

Why did they do it? This time around, the Chinese have complained about the threat of capital flowing out of the country – it’s a huge threat to their economy in its current form. That’s where they’ve laid the blame, on the two year slide in the value of the yuan. With that, they’ve allegedly been fighting to keep the yuan stable and have been stepping up restrictions on money leaving the country. Today’s move, which included a spike in the overnight yuan borrowing rate, was a way to crush speculators that have been betting against the currency, putting further downward pressure on the currency. But it also likely Trump related – the beginning of a crawl higher in the currency as we head toward the inauguration of the new President Trump. It’s very typical for those under the gun for currency manipulation to make concessions before they meet with trade partners.

So, should we be concerned about the move today in China? No. It’s not another January 2016 moment. But the move did drive profit taking in twobig trends of the past two months: the dollar and U.S. Treasuries. With that, the first jobs report of the year comes tomorrow. It should provide more evidence that the Fed will hike a few times this year. And that should restore the climb in the dollar and in rates.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Remember this time last year? The markets opened with a nosedive in Chinese stocks. By the time New York came in for trading, China was already down 7% and trading had been halted. That started, what turned out to be, the worst opening stretch of a New Year in the history of the U.S. stock market.

The sirens were sounding and people were gripping for what they thought was going to be a disastrous year. And then, later that month, oil slid from the mid $30s to the mid $20s and finally people began to realize it wasn’t China they should be worried about, it was oil. The oil price crash was a ticking time bomb, about to unleash mass bankruptcies on the energy industry and threaten a “round two” of global financial crisis.

What happened? Central banks stepped in. On February 11th, the Bank of Japan intervened in the currency markets, buying dollars/selling yen. What did they do with those dollars? They must have bought oil, in one form or another. Oil bottomed that day. China soon followed with a move to boost bank lending, relieving some fears of a global liquidity crunch. The ECB upped its QE program and cut rates. And then the Fed followed up by taking two of their projected four rate hikes off of the table (of which they ended up moving just once on the year).

What a difference a year makes.

There’s a clear shift in the environment, away from a world on liquidity-driven life support/ and toward structural, growth-oriented change.

With that, there’s a growing sense of optimism in the air that we haven’t seenin ten years. Even many of the pros that have constantly been waiting for the next “shoe to drop” (for years) have gone quiet.

Global markets have started the year behaving very well. And despite the near tripling from the 2009 bottom in the stock market, money is just in the early stages of moving out of bonds and cash, and back into stocks. Following the election in November, we are coming into the year with TWO consecutive record monthly inflows into the U.S. stock market based on ETF flows from November and December.

The tone has been set by U.S. markets, and we should see the rest of the world start to play catch up (including emerging markets). But this development was already underway before the election.

Remember, I talked about European stocks quite a bit back in October. While U.S. stocks have soared to new record highs, German stocks have lagged dramatically and have offered one of the more compelling opportunities.

Here’s the chart we looked at back in October, where I said “after being down more than 20% earlier this year, German stocks are within 1.5% of turning green on the year, and technically breaking to the upside“…

And here’s the latest chart…

You can see, as you look to the far right of the chart, it’s been on a tear. Adding fuel to that fire, the eurozone economic data is beginning to show signs that a big bounce may be coming. A pop in U.S. growth would only bolster that.

And a big bounce back in euro zone growth this year would be a very valuabledefense against another populist backlash against the establishment (first Grexit, then Brexit, then Trump). Nationalist movements in Germany and France are huge threats to the EU and euro (the common currency). Another round of potential break-up of the euro would be destabilizing for the global economy.

With that, as we enter the year with the ammunition to end the decade long economy rut, there are still hurdles to overcome. Along with Trump/China frictions, the French and German elections are the other clear and present dangers ahead that could dull the efficacy of Trumponomics.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

As of the end of last week, 78% of the companies that have reported earnings for the most recent quarter have beaten estimates.

That’s on about a third of S&P 500 companies that have reported thus far. Remember, FactSet says on average (the five-year average), 67% of companies in the S&P 500 beat their analyst expectations. And they beat by an average of 4%. So the numbers in this earnings season are running a little hotter, albeit on a lowered bar.

We’ve talked quite a bit in the past week about the run up to Apple earnings, which came in yesterday after the market close. The earnings number beat expectations. But it was by a slim margin.

The stock was lower on the day. Still, on the second quarter report, this past July, Apple was a sub $100 stock (trading at just above $96). Today it will close above $115. That’s 20% higher in the span of one quarter, and it was on a report that was very much in line with the report we heard yesterday. And the report included only a few weeks of the new iPhone7 release. And it doesn’t reflect implosion of Apple’s competitor, Samsung.

As the media and analyst tend to do, especially when the macro news front is quiet and market volatility is quiet, they picked apart and speculated on the future of Apple today as a company that may have peaked.

Let’s just take a look at the stock, and not pretend to have better visibility on the future of the company than the people do inside — the same one’s that put a transformational supercomputer in our pockets.

The stock still trades at 13x earnings. The S&P 500 trades at 16x. Apple trades at 13x next year’s projected earnings. The S&P 500 trades at 16.5x. Clearly it’s undervalued compared to the broader market. What about Apple’s monster cash position? Apple has even more cash now — a record $237 billion. If we excluded the cash from the valuation, Apple trades at 8.6x earnings. Though not an apples to apples (pun), and just as a reference point, that valuation would group Apple with the likes of these S&P 500 components that trade 8 times earnings: Dow Chemical, Prudential Financial, Bed Bath & Beyond, a Norwegian chemical company (LBY), and Hewlett Packard Enterprise. It’s safe to say no one is debating whether or not Hewlett Packard is at the pinnacle of its business. Yet, if we strip out the cash in Apple, AAPL shares are trading at an HPE valuation.

Apple still looks like a cheap stock.

Click here to get started and get your portfolio in line with our Billionaire’s Portfolio.

By November 15th, the biggest investors in the world will be required to disclose a snapshot of what their portfolios looked like at the end of the third quarter.

I suspect we’ll find that Apple was heavily bought during the period.

You might recall, the media was stirring about the second quarter filings (which were reported back in August). Some big names had sold or trimmed stakes in Apple.

But, as I discussed at that time, the Q2 portfolio snapshots came just days following the big surprising Brexit decision in the UK. Global markets swung violently on the news back in June. Remember, between June 23rd and June 27th, the S&P 500 fell as much as 5.7%. It made it all back the subsequent four days.

With that event in mind, billionaire investors David Einhorn, George Soros and Chase Coleman – all had sold Apple shares by the end of the second quarter.

But remember, unlike most stocks they own, they can all trade Apple with virtual anonymity between quarters. The stock is too large for anyone one investor to take a 5% controlling stake, which would trigger the requirement of a 13D or 13G filing with the SEC, which would require updated filings (or amendments) within 10 days of any change in the position size (sell one share, you have to report it).

Einhorn even bragged in one of his investor letter’s this year that they have done a good job of “trading” Apple.

Make no mistake, even with the trimmed stakes of Q2, Apple was (and is) still the “who’s who” of billionaire investor-owned stocks. It was still Einhorn’s largest position into the end of Q2. Buffett swooped in and bought shares near the 52-week low.

When we see the Q3 filings next month, I would expect those that were cutting stakes at the end of Q2, were adding it all back in early Q3. And with the run-up in Apple shares since, up 22% from the June lows, I predict it will be the most bought stock of the third quarter. If that’s true, I predict the media and Wall Street will be talking about how great Apple is again (i.e. analyst upgrades will follow).

In the past month, there’s been a solid take up on the new iPhone 7 for Apple. Importantly, with the iPhone 7 launch, all four major carriers have returned to the model of offering free new iPhones for long term contracts. That’s a huge positive on the stock as a product-cycle driven company. Add to that, there’s no other stock that, if not owned and owned enough, can get a professional money manager fired than Apple. That creates a “fear of missing out” trade in the institutional investor community — pushing them off of the sidelines and back into Apple.

But perhaps the most important event for Apple has been the very public implosion of their biggest competitor Samsung. Samsung has been forced to recall their competitive smartphone the Galaxy Note 7 because it’s been bursting into flames. It’s projected to cost the company over $5 billion. Most importantly, it’s positioning Apple, right in the sweetspot of their new product (latest phone) rollout, to take more market share.

If we do indeed find next month that the biggest and smartest investors in the world spent Q3 loading up on Apple, it should give a stamp of approval that sentiment has turned for the stock. Apple remains one of the most undervalued stocks in the S&P 500, with the most powerful fundamentals: it’s cheap at 13x trailing and forward earnings, has an incredible balance sheet with $231 billion in cash, and a high analyst price target of $185 a share.

As I noted last week, the company reported a second consecutive quarter of year-over-year earnings decline in July. But it crushed estimates. The stock took off from $96 and trades today at $117. They report on the most recent quarter on October 25. The consensus earnings estimate is $1.64–which would be a third consecutive year-over-year decline. The recent revisions to that estimate have been down (not surprisingly), which sets up for a beat. The last time Apple reported two consecutive quarters of year-over-year declines was mid-2013. The stock bottomed in that period.

Click here to get started and get your portfolio in line with our Billionaire’s Portfolio.

{kind=link}