We’ve talked about the glaring lag in the performance of blue chip stocks coming out of this recent stock market correction. This is creating a huge opportunity to buy the Dow, now.

With all of the complexities you can make of investing, this one is simple. The blue-chip Dow Jones Industrials Index is down on the year (as of this morning). The Nasdaq is up 13% on the year. Small caps (the Russell 2000) is up 11%.

And we’re in an economy that’s running at better than 3% growth, with low inflation, ultra-low rates, and corporate earnings growing at 20% year-over-year. With this formula, and yet a tame P/E multiple on stocks, we’ll probably see stocks up doubledigits before the year is over. Meanwhile, we are already in July, and the DJIA — the most important benchmark stock index for global markets – is starting from near zero.

You may be thinking the boring “industrials” average is out-dated, and flat for a reason. But as far as the makeup of the indices is concerned: The index curators will shuffle the constituents to ensure that the biggest, best performing companies are in it. Bad stocks get kicked out. Good stocks get added. And, to be sure, your retirement money will be methodically plowed into it (the benchmark indices) every month by Wall Street investment professionals.

Bottom line: The DJIA is presenting a gift here to invest, at a discount, in an economy that’s heating up. And you get this chart, which we’ve been watching in recent weeks. This big trend line has held, and so has the 200-day moving average.

How do you buy it? Your financial advisor will put you into mutual funds with big sales loads and fees in attempt to track the Dow. But you can buy an ETF that tracks the Dow for as little as 17 basis points (example: symbol DIA, the SPDR DJIA ETF). This Dow looks like low hanging fruit.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We talked yesterday about the big influence of oil. And how the swings of the past few years have directly impacted the global economy.

Too low was threatening another global financial crisis. Now, too high is threatening to choke off the strength of the economic recovery.

Both high and low prices have been manipulated by OPEC. And we now await a decision from OPEC nations on whether or not a they will hike production to curb the level of oil prices. For a group that operates for their best interest, it doesn’t seem to be in their best interest. That decision will be announced tomorrow at a press conference.

Given the attention the Trump has given to OPEC and oil prices recently, a negative surprise (i.e. no production hike) may trigger the oil price/stock market inverse correlation trade (oil goes up, stocks go down).

On that note, we have some negative momentum going into tomorrow. Before today’s close, the Nasdaq was up 14% year-to-date. Meanwhile, the S&P 500 is up just around 3%. That’s a lopsided market.

But today we get a big outside day (key reversal signal) in the Nasdaq futures.

And the catalyst for this technical reversal setup was the Supreme Court ruling today that internet sales should be subject to state tax.

We’ve talked about the building scrutiny from the Trump administration facing the tech giants. This is another “level the playing field” step. If Amazon is pricing in the prospects of taking over everything (i.e. monopoly), this is the shot across the bow.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We’ve talked the past couple of days about economic growth and the likelihood that we’re just beginning to see the positive surprises from Trumponomics materialize in the economic data.

The formula for GDP is consumption + investment + government spending + net exports. So you can see in these components, the direct targeting of economic stimulus in the Trump economic plan to drive growth: tax cuts, deregulation, repatriation, infrastructure and trade negotiations.

Now, consumption makes up about two-thirds of GDP. Let’s look at consumption today, and we’ll step through the other contributors to GDP over the next few days.

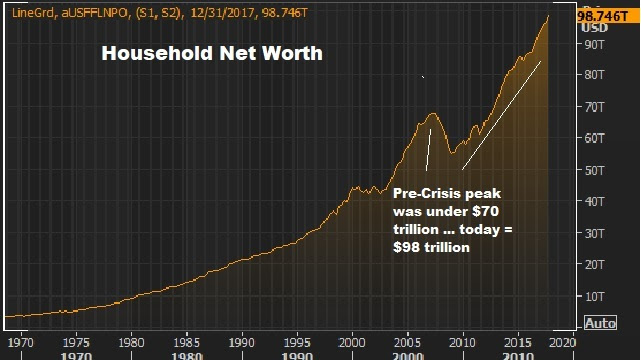

First, what is the key long-term driver of economic growth over time? Credit creation. When credit is used to buy productive resources, wealth goes up. And when wealth goes up consumption tends to go up. With that in mind, in the chart below you can see the sharp recovery in consumer credit (in orange) since the depths of the economic crisis (this excludes mortgages). And you can see how closely GDP (the purple line, economic output) tracks creditgrowth.

And we have well recovered and surpassed pre-crisis levels in householdnetworth — sitting at record highs now (up another $2 trillion since we last looked at it) …

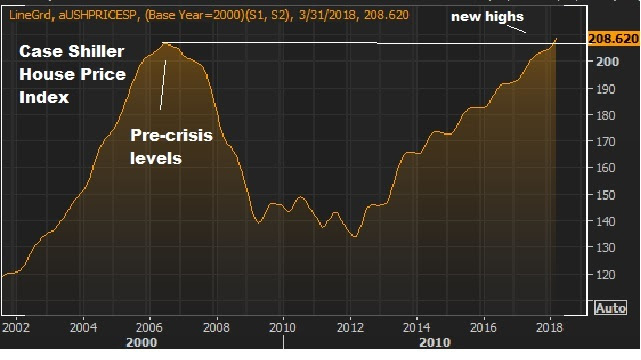

A large contributor to the state of consumption is the recovery and stability in housing. We are now back to new highs on the broad housing index …

When we consider this solid backdrop, remember, we’ve yet to have a return of ‘animal spirits’ — a level of trust and confidence in the economy that fuels more aggressive hiring, spending and investing.

And with that, as we discussed yesterday, while we are in the second longest post-War economic expansion, we’ve yet to have the aggressive bounce back in growth that is characteristic of post-recession recoveries.

But we now have the pieces in place to see the return of animal spirits and a big pop in economic growth. And that should continue to fuel for much higher stock prices. And there are stocks that will do multiples of what the broader stock market does.

On Friday, we talked about the building momentum in the economy. We’ve already had huge positive surprises in corporate earnings for the first quarter. And we’re probably just beginning to see the positive surprises on economic data roll in.

Remember, despite the execution success on Trumponomics over the past year (deregulation, repatriation, tax cuts and $400 billion in new government spending approved), the Fed is still expecting growth to come in well below trend (3%), at 2.7%. That’s just 20 basis points higher than they projected prior to the execution of massive tax cuts in late December.

The good news: Positive surprises are fuel for confidence and fuel for stocks.

Remember, we’ve yet to have a return of ‘animal spirits’–a level of trust and confidence in the economy that fuels more aggressive hiring, spending and investing. We should see this reflected in wage growth. Wage growth has been the missing piece of the economic recovery puzzle.

On that note, we’re now near the best wage growth in nine years, and that tax rate cut is still in the early stages of working through the economy.

Don’t underestimate the value of confidence in the outlook (and the return of “animal spirits”) to drive economic growth higher than the number crunchers in Washington can imagine. Remember, these are the same experts that couldn’t project the credit bubble, and didn’t project the sluggish ten years that have followed.

Remember, while we’re in the second longest post-War economic expansion, we’ve yet to have the aggressive bounceback in growth that is characteristic of post-recession recoveries. We now have the pieces in place to finally get it.

So, as we’ve discussed throughout the year, the backdrop continues to get better and better for stocks.

As we head into the long holiday weekend, let’s look at some key charts.

First, just a week ago, the U.S. interest rate market was spooking investors, as 10-year yields were hanging around 3.10%. The fear was, would 3% yields quickly turn into 4% yields, and hit economic activity.

As of today, we’re trading closer to 2.90% again, back below 3%.

But you can see, we run into this big trendline that represents this ascent in rates for 2018, which also reflects the outlook of a hotter economy, thanks to tax cuts (fiscal stimulus).

Bottom line here: The concern in interest rates is speed, not trajectory. The trajectory should continue to be UP, which is a signal that the economy is improving, and finally gaining the tracking to perform at trend, if not better than trend growth. The concern about ‘speed’ should be far less than it was a week ago.

Next, here’s a look at the S&P 500.

You can see in the chart above, we’ve broken the downtrend of this correction cycle. The longer-term trend is UP. And this bull trend started, not coincidentally, at the bottom of the oil price crash in 2016, when global central banks stepped in with measures to stem the slide in confidence.

So, we’ve had a healthy 12% correction in stocks, we’ve held the 200-day moving average, we’ve maintained the longer-term trend, and we’ve broken out of the downtrend of the correction. Small cap stocks have already returned to new record highs. And we have an economy on pace to grow at 3% this year or better, with corporate earnings expected to grow at 20% for the year. So, the second half of the year should be very good for stocks.

Stocks have a huge influence on sentiment. And sentiment has a huge influence on economic activity.

With that, for the better part of the past four months, we’ve discussed the technical correction we’ve seen in stocks. And we’ve waited patiently for a catalyst to end the correction and resume the long-term bull trend for the stock market.

That catalyst, we anticipated, would be first quarter data (namely earnings and GDP growth). Indeed, that data has confirmed that fiscal stimulus is stoking the economy – shifting it into a higher growth gear than what we’ve seen coming out of the global financial crisis.

Let’s take a look at how this has played out, and the important technical break we’ve had today in the Dow that further supports that the correction is over.

As you can see, we put in the low of this technical correction in the Dow the day after the first quarter ended. And we’ve since seen Q1 earnings roll in, with record positive earnings surprises, record margins and the hottest revenue growth we’ve seen in a long time. Toward the end of April, we had our first look at Q1 GDP growth. That too beat expectations and showed an economy that is growing at 2.875% over the past three quarters — closing in on that big 3% trend-growth level.

Along the way, we’ve tested the 200-day moving average (the purple line) and held. And today, we get a break of this big trendline from the highs of January.

And this beak in stocks comes with the 10-year yield back at 3%, and with oil above $70. While some have seen these levels as a risk to growth, they are rather reflecting a stronger economy, with surging demand.

At the end of last week, I said “it looks like the all-clear signal has been given to stocks.”

Well, we had some more discomfort to deal with this week, but that statement probably has more validity today than it did last Friday.

With that, let’s review the events and conditions of the past two weeks, that build the case for that all-clear signal.

As of last Friday, more than half of first quarter corporate earnings were in, with record level positive surprises in both earnings and revenues (that has continued). And we got our first look at first quarter GDP, which came in at 2.3%, better than expected, and putting the economy on a 2.875% pace over the past three quarters.

What about interest rates? After all, the hot wage growth number back in February kicked the stock market correction into gear. The move in the 10-year yield above 3% last week started validating the fears that rising interest rates could quicken and maybe choke off the recovery. But last week, we also heard from the ECB and BOJ, both of which committed to QE, which serves as an anchor on global rates (i.e. keeps our rates in check).

Fast forward a few days, and we’ve now heard from the last but most important tech giant: Apple. Like the other FAANG stocks, Apple also beat on earnings and on revenues.

Still, stocks have continued to trade counter to the fundamentals. And we’ve been waiting for the bounce and recovery to pick up the pace. What else can we check off the list on this correction timeline? How about another test of the 200-day moving average, just to shake out the weak hands? We got that yesterday.

Yesterday, in the true form of a market that is bottoming, we had a sharp slide in stocks, through the 200-day moving average, and then a very aggressive bounce to finish in positive territory, and on the highs of the day. That took us to this morning, where we had another jobs report. Perhaps this makes a nice bookend to the February jobs report. This time, no big surprises. The wage growth number was tame. And stocks continued to soar, following through on yesterday’s big reversal off the 200-day moving average.

With all of this, it looks like “the all-clear signal has been given to stocks.”

Yields continue to grind higher toward 3%. That has put some pressure on stocks, despite what continues to be a phenomenal earnings season. This creates another dip to buy.

Yesterday, we talked about a reason that people feel less good about stocks, with yields heading toward 3%. [Concern #1] It conjures up memories of the “taper tantrum” of 2013-2014. Yields soared, and stocks had a series of slides.

My rebuttal: The domestic and global economies are fundamentally stronger and much more stable. But maybe most importantly, the economy (still) isn’t left to stand on its own two feet, to survive (or die) in a normalizing interest rate environment. We have fiscal stimulus doing a lot of heavy lifting.

Let’s look at a couple of other reasons people are concerned about stocks as yields climb:

[Concern #2] Maybe this is the beginning of a sharp run higher in market interest rates — like 3% quickly becomes 4%?

My Rebuttal: Very unlikely given the global inflation picture, but more unlikely with the Bank of Japan still buying up global assets in unlimited amounts (Treasuries among them, through a variety of instruments). They can/and are controlling the pace, for the benefit of stimulating their own economy and for the benefit of stimulating and maintaining stability in, the global economy.

[Concern #3] I hear the chatter about how a 3% 10-year note suddenly creates a high appetite for Treasuries over stocks at this point, especially from a risk-reward perspective (i.e. people are selling stocks in favor of capturing that scrumptious 3% yield).

My Rebuttal: In this post-crisis environment, a rise toward 3% promotes the exact opposite behavior. If you are willing to lend for 10-years locked in at a paltry rate, you are forgoing what is almost certainly going to be a higher rate decade than the past decade. If you need to exit, you’re going to find the price of your bonds (very likely) dramatically lower down the road. Coming out of a zero-interest rate world, bond prices are going lower/not higher.

Remember this chart …

The bond market has become a high risk-low reward investment. Meanwhile, with earnings set to grow more than 20% this year, and stock prices already down 7% from the highs of the year, we have a P/E on stocks that continues to slide lower and lower, making stocks cheaper and cheaper. That makes stocks a far superior risk/reward investment, relative to bonds – especially with the prospects of the first big bounce back in economic growth we’ve seen since the Great Recession.

As we’ve discussed, the proxy on the “tech dominance” trade is Amazon. That’s the proxy on the stock market too. And it’s not going well. The President hammered Amazon again over the weekend, and again this morning.

Here’s what he said …

Remember, we had this beautiful heads-up on March 13, with the reversal signal in Amazon.

That signal we discussed in my March 13 note has now predicted this 15.8% decline in the fourth largest publicly traded company. And it’s dictating the continued correction in the broader market.

If you’re a loyal reader of this daily note, you’ll know we’ve been discussing this theme for the better part of the last year. The regulatory screws are tightening. And the tech giants, which have been priced as if they are, or would become, perfect monopolies, are now in the early stages of repricing for a world that might have more rules to follow, hurdles to overcome and a resurrection of the competition they’ve nearly destroyed.

As we know, Uber has run into bans in key markets. We’ve had the repeal of “net neutrality” which may ultimate lead big platforms like Google, Twitter, Facebook and Uber, to transparency of their practices and accountability for the actions of its users. Trump is going after Amazon, as a monopoly and harmful to the economy. Tesla, a money burning company, is being scrutinized for its inability to mass produce — to deliver on promises. For Tesla, if sentiment turns and people become unwilling to continue plowing money into a company that’s lost $6 billion over the past five years (while contributing to the $18 billion wealth of its CEO), it’s game over.

With that said, this all creates the prospects for a big bounce back in those industries that have been damaged by tech “disruption.” And this should make a stock market recovery much more broad-based than we’ve seen.

With the sharp decline in stocks today, we’ve retested and broken the 200-day moving average in the S&P 500. And we close, sitting on this huge trendline that describes the rise in stocks from the oil-crash induced lows of 2016.

Today we neared the lows of the sharp February decline. I suspect we’ll bottom out near here and begin the recovery. And that recovery should be fueled by very good Q1 earnings and a good growth number — brought to us by the big tax cuts.

The sharp swings continue in stocks, with the bias toward the downside. And as we’ve discussed over the past two weeks, it’s all led by the tech giants. Remember, on Friday we looked at the most important chart in the stock market: the chart of Amazon (as a proxy on the tech giants). Early this afternoon, Amazon was outpacing the S&P 500 to the downside by 4-to-1, and finally the broader market cracked to follow it.

This all continues to look like the market is beginning to price in a world where the tech giants, that have taken dangerously significant market share over the past decade, are on the path of tighter regulation and a leveling of the playing field, which will result in higher costs of doing business. That will change their position of strength and open the door to a resurrection of the competition.

Remember, on the stock slide of this past Friday, the S&P 500 hit the 200-day moving average and bounced sharply. It now looks like we’ll get another test of it, probably a break, and maybe take another peak at the February lows.

Here’s a look at the chart ….

You can see in the chart above the technical significance of these levels. This represents the trend from the oil price induced lows of 2016. And the slope of this trend incorporates the optimism from the Trump election and the outlook on pro-growth policies.

With that significance at play, a breach of this support, at least for a short time, would all play into the scenario that we’ll see more swings in stocks (pain for the bulls) until we get to earnings season, which kicks into gear on April 13. And as we discussed, that should begin the data-driven catalyst for stocks (earnings and growth, fueled by fiscal stimulus).

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here for the best stocks to buy in this market correction.