With the big Fed meeting this week, there continues to be some debate about whether they will cut by 25 basis points or 50.

But the direction matters more than the magnitude.

It signals the end of the Fed’s “policy damage” to emerging markets.

Higher U.S. rates have meant a stronger dollar. And with the economy moving north, the dollar moving north and rates moving north, global capital has moved toward the U.S. — and away from riskier emerging markets.

It's not that the U.S. economy can't handle a 2.5% Fed Funds rate, it's that the EM world can't handle it (in the current post-financial crisis economic environment).

As the Dallas Fed put it last year: “Emerging economies have suffered a general decline in forecast GDP growth … The tightening of monetary policy in advanced economies, both through rate hikes and other policy actions such as forward guidance, results in capital outflows from emerging economies with low reserves relative to their foreign debt.”

This official direction change from the Fed should weaken the dollar. Moreover, a key piece in the continuation of the global economic recovery will likely be a weaker dollar.

It will drive a more balanced U.S. and global economy, and it will reflect strength in emerging markets (i.e. capital flows to emerging markets).

If you haven't signed up for my Billionaire's Portfolio, join now — get your risk free access here.

We've talked about the set up for a positive surprise coming into this morning's first reading on Q2 GDP.

We did, indeed, get a positive surprise. The economy grew at 2.1% pace in the second quarter. That's better than the Wall Street estimate (1.8%), and a lot better than the Atlanta Fed's estimate of 1.3%.

As we've discussed over the past two weeks, the first half of Q2 earnings season has been better than expected, because of a strong consumer. With that, it was a safe bet that we would see the strong consumer show up in GDP this morning. Consumer spending was up 4% in the quarter. Domestic demand grew by 3.5%.

Things are pretty good.

This leaves some people wondering if the Fed's case for rate cuts has been damaged.

The answer is no. While consumer confidence has been stabilized and underpinned by central bank rhetoric, business confidence has been a different story.

And this is something the Fed has been emphasizing. Business fixed investment declined (in Q2) for the first time in three years. This is clear concern about an indefinite trade war — and monetary policy that is too tight, relative to the rest of the world, if trade protectionism were to spread and amplify.

That's where the Fed has plenty of jusitification to make their move next week.

If you haven't signed up for my Billionaire's Portfolio, join now — get your risk free access here.

We heard from the ECB this morning. Draghi was expected to step up his "ready to act" rhetoric, but was unlikely to do anything. That was the case.

As we discussed yesterday, an official change in policy direction by the Fed next week (cutting rates, a three year rate hiking campaign), should be enough to ease the pressure on the global economy, without requiring a move by the ECB and more stimulus from the BOJ.

Let's talk about earnings and tomorrow's GDP report.

The theme of the year has been concern about the slowing economy. While it hasn't reflected much in the data, the fear has been driven by the prospects of eroding global confidence.

The first place that tends to show up is in financial markets. We saw it late last year, as U.S. and global stocks plunged.

But if we look at how the consumer has done through the first half of 2019, there are no signs of a loss of confidence. The consumer discretionary sector is up 25% year-to-date, outperforming the broader market (which is up 20%).

Earnings have continued to beat expectations in consumer related businesses. We saw it early in the earnings seasons in Q1 and Q2, from the performance of the consumer businesses within the big banks. Today, Starbucks gave us another barometer on the consumer (a beat on earnings, with 26% year-over-year earnings growth). Expedia, the online travel booking site beat on earnings, with 9% growth in booking revenue from the same period a year ago.

Why has the consumer held in strong this year, in the face of a confidence shock to end 2018?

The Fed (and global central banks) answered the call. The did what they've done for the past decade — promising to do whatever it takes to keep the economy moving forward, and to avert any economic shocks. That's enough to keep people spending and investing. But a trade deal will be needed (soon) to keep it going.

We get the first look at Q2 GDP tomorrow morning. The Atlanta Fed model is looking for just 1.3% growth in the quarter. With consumption contributing 70% of that reading, this GDP number looks setup for a positive surprise.

If you haven't signed up for my Billionaire's Portfolio, join now — get your risk free access here.

Over the next five business days we'll hear from the European Central Bank, the Bank of Japan and the Fed.

The ECB will kick it off tomorrow morning. And we head into this major central bank meeting with U.S. stocks sitting on new record highs. And with German bond yields trading very near record lows (at negative 37 basis points).

We already know all three of these major central banks have made it clear over the past seven months that they will do more easing, more unconventional policies if needed. The question is, will the ECB, just seven months removed from ending its QE program, announce a new stimulative program? Will the BOJ add to its QE program? Doubtful. I suspect, a reversal of course by the Fed next week (from a three year rate hiking campaign, to cutting rates), will be enough to ease the pressure on the global economy, without more official action from the ECB and BOJ.

Any pressure on the ECB and BOJ to do more would be further eased, if a U.S./China trade deal were to follow the Fed's move.

The Trump administration appears to be putting the timeline in place. U.S./China trade negotiations will restart in China next Tuesday through Wednesday (the day we expect to get a Fed cut). And then the Treasury Secretary said today, they plan to have meetings come back to D.C.

Remember, Trump is in the position of strength on the China negotiations. At anytime, he can make any concessions necessary to do a deal, and remove the overhang of uncertainty on the global economy. Heading into next year's election, he would have a tailwind of a booming economy.

Now, with U.S. stocks sitting on record highs, let's take a look at a couple of stock market charts that should offer bigger opportunity over the next five months, following the global economic relief of a Fed pivot (rate cut).

Here's a look at German stocks. The S&P 500 is on record highs, the DAX is 9% off of the record highs (from January of last year).

And here's a look at Japanese stocks. You can see the Nikkei looks like a technical breakout is coming (i.e. going higher). The S&P 500 is on record highs, and the Nikkei is 13% away from the October 2018 highs.

If you haven't signed up for my Billionaire's Portfolio, join now — get your risk free access here.

Earnings continue to come in strong. Remember, we entered the earnings season with market expectations of a 3%decline in year-over-year in earnings.

With about a fifth of the companies now reported, close to 80% have surprised positively on earnings, on an earnings growth rateof about 7%.

If we look at some of the blue chip American brands reporting today, the year-over-year earnings growth looks solid, if not strong. Kimberly-Clark, the paper/consumer products company, grew earnings by 5% compared to the same period a year ago. The big conglomerate, United Technologies grew earnings by 12%. Lockheed Martin grew earnings by 23%.

With these three companies we get signals on three of the components of the economy: Consumption (Kimberly-Clark), Investment (UTX), Government Spending (LMT). The fourth component is net exports. One of the largest exporters in the S&P 500, International Paper, reports on Thursday.

With the above in mind, we get the first reading on Q2 GDP this Friday, which is expected to have slowed from 3.1% in the first quarter, to 1.6% (Atlanta Fed's estimate) in the second quarter.

Remember, we talked last week about the set up for positive surprises in earnings (which we're getting) AND in the economic data. This growth number looks like it includes an assumption of an economic storm. But in the word's of the Coca Cola CEO today, the storm (for Q2) never arrived.

Add to that, any meltdown that might have been underway in global confidence, has been warded off by global central banks (either easing or setting expectations for easier financial conditions).

If you haven't signed up for my Billionaire's Portfolio, join now — get your risk free access here.

On Friday, we talked about the strong Microsoft earnings.

Thanks to the strategy reset that took place five years ago, Microsoft is part of the duopoly in cloud computing. And that has led Microsoft to stand alone (at the moment) as the only trillion-dollar company in the world. By the end of the week, we will likely see them joined (again) by the other half of the cloud computing duopoly, Amazon.

When we think about the great "disrupters" of the past decade, and how the industries that they've disrupted will be left, when it has all shaken out, I think this MSFT/AMZN story is a good analog.

The giants of industry, if they move aggressively with the disrupters, have the distribution to compete, if not beat, the disrupters.

The Walmart/Amazon battle is another great example. The market has priced Amazon like a runaway monopoly — killer of all industries, especially retail. And the perception has been that Walmart was destined to become another rise and fall story of a dominant American retailer. Sears, Toys R Us and about 70 other retailers have gone under in the last four years.

But Walmart has been transforming.

Walmart has been aggressively investing in online. They bought Jet.com in 2016, an American online retailer. That same year they took a large stake in the number two online retailer in China, JD.com. Walmart now owns 12% of JD.

JD.com already has a big share of ecommerce in China. They are number two to Alibaba, but gaining ground due to some clear competitive advantages. JD owns and controls its logistics infrastructure, and does quality control from the supplier to delivery. And unlike Alibaba, JD sources product to its warehouses to fight the counterfeit goods risk – a big problem in China. JD has 500+ warehouses around the country, and they now source product and service customers from one of the more than 400 Walmart stores in China.

So Walmart is positioned well to take advantage of the growth in the middle class in China. Amazon has yet to find its way in China. It has about 1% market share. Add to this, Google came in last year with a $550 million investment to help position JD to challenge Alibaba and Amazon on a global scale. Walmart is still about a third of the value of Amazon, but the gap has been closing (slowly).

Lastly, let's look at Netflix and the response underway at Disney. In recent years, Netflix has been thought to be taking over the entertainment industry with its disruptive direct-to-consumer model.

Fox responded early and aggressively (thanks the activist investor, Jeff Ubben). They made an aggressive move to build the direct-to-consumer model (taking stakes in Hulu, Star India and Sky). That set the company up as an acquisition target. And now with the Disney acquisition of Fox, Disney is positioned with a dominant duel threat — among the world's deepest and most valuable library of content and the distribution to take it to the consumer. This makes the world's preeminent entertainment company.

The result? Disney's valuation has leapfrogged Netflix. Disney now has a market cap of $250 billion. And Netflix has plunged $50 billion in value, to a market cap of $135 billion, since the Disney/Fox marriage last year.

If you haven't signed up for my Billionaire's Portfolio, join now — get your risk free access here.

This week, earnings have been a nice distraction from the market’s Fed watching obsession.

Second quarter earnings have gotten off to a good start with very strong earnings from the big banks. And those earnings have been driven by strong consumer business.

Today we heard from Microsoft. The company grew earnings by 20% year-over-year, and with 12% revenue growth.

We talked about MSFT earnings back in April, when Microsoft became the third trillion-dollar company. The first was Apple. And then Amazon.

But despite the market sitting on new record highs, Microsoft now stands alone as the only trillion-dollar company.

Let’s revisit the story from my April note, on how Microsoft has transformed itself from a path of obsolescence to quadrupling in value in just six years.

The CEO, Satya Nadella, gets the credit, but it has everything to do with a guy named Jeff Ubben.

Back in April of 2013, an activist investor named Jeff Ubben took a $2 billion stake in MSFT. That same month Business Insider wrote a story titled: “Microsoft Could Be Obsolete By 2017.” The stock had gone nowhere for more than a decade.

Ubben won a board seat and he pushed for stock buybacks and a strategy reset. He pushed out the CEO, Steve Balmer. He replaced him with Satya Nadella, who was running the Miscrosoft cloud business. His job was to turn Miscrosoft into a cloud computing company. He has done it.

Microsoft is now the number two cloud computing platform globally, behind Amazon. For perspective, cloud computing is a $200 billion market growing at close to 20% a year. And Microsoft’s cloud business, Azure, grew revenue by 64% last quarter.

Bottom line: Amazon and Microsoft have a duopoly in the high growth digital storage business (i.e. cloud computing).

Amazon’s retail business gets all of the attention, but it’s cloud business has been subsidizing it’s retail business for a long time. The hyper-growth in cloud and the market dominance held by Amazon and Microsoft are why their market value has gone to a trillion-dollars, and why their charts look so similar …

If you haven’t signed up for my Billionaire’s Portfolio, join now — get your risk free access here.

With 12 days until the July Fed decision, the Trump administration has attempted to dial DOWN expectations of a China trade deal coming anytime soon.

And today the Fed marched out two Fed officials (one of which is the vice chair) ramping UP the rhetoric to telegraph rate cuts at the end of the month.

After the Fed comments, the market swung from expectations of just a 25 basis point cut to a near 80% chance (at one point in the day) of a 50 basis point cut coming on July 31.

That was good enough to drive a technical breakout in gold. Gold finishes the day just shy $1,450. That’s the highest level since mid-2013.

Let’s take a look at the chart ….

So, we’re about 32% away from the 2011 highs. Those highs were, of course, induced by fears that QE would lead to runaway inflation. That is, the gold trade was a hedge against inflation. Inflation didn’t materialize. And the price of gold was nearly cut in half over the next few years. After all, following massive global QE, deflation remains the bigger risk.

But now money is moving into gold as a hedge against global currency devaluations. In both scenarios, the gold trade is about hedging against inflating away global buying power.

With the above in mind, remember we’ve discussed the prospects that this trade war with China may end with a grand and coordinated currency agreement— perhaps with a big depreciation of the dollar, similar to the 1980s “Plaza Accord.”

If you haven’t signed up for my Billionaire’s Portfolio, join now — get your risk free access here.

With Bank of America earnings today, we’ve now heard from all of the big four banks (JPM, BAC, WFC and C).

We’ve had positive earnings surprises in each, for an average earnings growth of 21% for the group. That’s 21% yoy earnings growth for the biggest banks in the country, in a quarter where the broader market is expected to shrink earnings by 3%.

The positive surprises in bank earnings have been driven by the consumer business. And keep in mind, the consumer (personal consumption) makes up 70% of the U.S. economy.

Perhaps Q2 will turn out better than the sub 2% growth expected by economists. The first reading on Q2 growth is due to be reported next Friday.

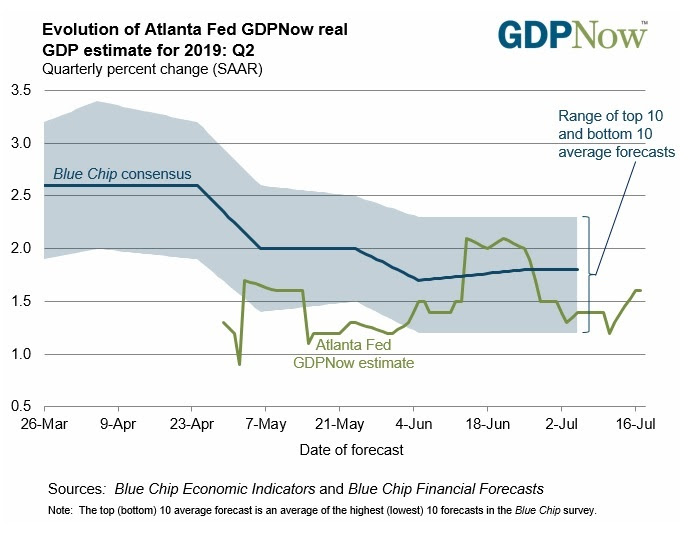

Here’s what the Atlanta Fed model on GDP growth looks like, as we continue to get Q2 data incorporated, going into the first GDP reading …

Remember, back in April, the first look at Q1 GDP came in as a huge positive surprise (at 3.2%). Many were expecting it to be a terrible quarter. Goldman Sachs thought the quarter would produce just 0.7% growth. They were wrong, and they weren’t alone. At the end of the first quarter, the Atlanta Fed’s GDP model was estimating that the economy grew at only 0.3% in Q1.

If you haven’t signed up for my Billionaire’s Portfolio, join now — get your risk free access here.

Today we heard from two more of the “big four banks” on Q2 earnings.

Yesterday, Citi kicked it off with 11% earnings growth compared to the second quarter of last year. This morning, JP Morgan beat expectations, reporting 23% yoy earnings growth. Wells Fargo followed with an earnings beat, growing earnings by 32% yoy.

The banks continue to put up big numbers. And it’s, in large part, thanks to consumer banking. With record low unemployment, record high net worth and record high credit worthiness, the consumer business is strong.

Last year, one of the best value investors of the past twenty years, Jeff Ubben, said the U.S. banking system has the lowest risk profile “than any time in our investing lifetime.” A decade following the financial crisis, he thought the timing is finally right for major banks. He has been right.

With that in mind, if we look back at the sector weightings in the S&P 500, financials were the heaviest weighted sector in the years leading up to the financial crisis — at 22% of the index. The financials currently make up just 13% of the S&P 500. Meanwhile, the average P/E on the big four banks is just better than 10 – well below the long-term average on the broader market of 16. The banks are cheap (still).

If you haven’t signed up for my Billionaire’s Portfolio, join now — get your risk free access here.