As we said yesterday, oil on the mend is the key proxy right now for global economic stability. With that, after closing above $40 yesterday, oil continued its surge today, up 4%. And global stocks had a good day, up 1% in the U.S.

Remember, we get key inflation data over the next couple of days, namely from Europe and the U.S. A hotter inflation number in the U.S. would further support the signal that oil is giving to markets (a positive one).

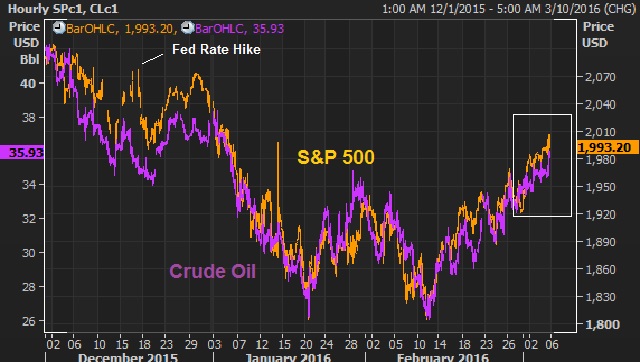

Today we want to look at a few of very key charts. This first chart is an update on the crude oil/stock market relationship. We’ve looked at this a few times over the past few months. The last time we revisited this chart, oil and stocks had started to diverge from stocks with its recent move back into the mid 30s.

So oil is sustaining above $40 for the first time since November. We know three of the top oil traders in the world are betting on $70-$80 oil by next year. We know central banks have stepped in (in coordination) since the low in oil on February 11 and the result has been a 50%+ bounce in oil. Now, technically, oil looks like a technical breakout is here.

In the above chart, you can see oil breaking above the high of March 22 (which was 41.90). In fact, we get a close above that level – technically bullish. And we also now have a technically bullish pattern (an impulsive C-wave of an Elliott Wave structure) that projects a move to $51.50, which happens to be right about where this big trendline comes in.

Now, with the inflation data in the pipeline for the week, we’ve talked about the negative signal that ultra-weak yields are sending to markets. And German yields have been leading the way on that front. But guess what? German yields reversed sharply off of the lows yesterday, and continued higher today, putting in a long term bullish reversal signal (an outside day – technical jargon, but can be very predictive of tops and bottoms). And that coincides with the U.S. 10-year yield, which is on the verge of breaking the recent downtrend and projecting a move back to 2.15%. We’ll take a look at these very important charts for financial markets and for the global economic outlook tomorrow.

These key markets are signaling what could be the beginning of a big shift in sentiment and the beginning of positive surprises in markets and economies, which tends to happen when expectations have been ratcheted down so dramatically, as we discussed yesterday with the sour earnings outlook and pessimistic economic backdrop.

This is the perfect time to join us in our Billionaire’s Portfolio. We have just added the billionaire’s macro trade of the year to our Billionaire’s Portfolio — a portfolio of deep value stocks owned by the best billionaire investors in the world. You can join us here.

Central bank posturing has put a bottom in oil and stocks in the past month. Rising stocks and oil, in this environment, have a way of restoring sentiment and the stability of global financial markets. Those efforts were underpinned by more aggressive stimulus from the European Central Bank last week.

And the Fed furthered that effort today.

Just three months ago, the Fed projected that they would hike rates an additional full percentage point this year. Today they backed off and cut that projection down to just 1/2 percent (50 basis points) by year end.

That’s a big shift. In the convoluted post-QE, post-ZIRP world, that’s almost like easing.

What’s happened in the interim? Janet Yellen was asked that today and said it was: Slowing growth in China … A negative fourth quarter GDP number in Japan … Europe has had weaker growth … and Emerging markets have been weighed down by declines in oil prices.

Aside from the negative GDP print in Japan, none of these were new developments (even Japan was no shocker). Meanwhile, during the period from the Fed’s December meeting to its meeting today, oil did a round trip from $37 to $26 and back to $37.

So what happened? It appears that the Fed completely underestimated the threat of weak oil prices to the global economy and financial system. We’ve talked extensively about the danger of persistently weak oil prices, which, at sub $30 was pushing the world very close to the edge of disaster. That threat became very clear in late January/early February, culminating when the one of the biggest oil and natural gas companies in the world, Chesapeake, was rumored to be pursuing the path of bankruptcy (which was of course denied by the company). It was that moment, it appears, that policymakers woke up to the risk that the oil bust could lead to another global financial crisis — with a cascade of defaults in the energy sector, leading to defaults in weak oil exporting countries, spilling over to banks and another financial crisis.

Today’s move by the Fed, while confusing at best, led to higher stocks and higher oil prices. The market has been pricing in a much more accommodative path for the Fed for the better part of the past three months, and today the Fed dialed down to those expectations (i.e. they have now followed the ECB’s bold easing with some easier policy/guidance of their own), which should provide more fuel for the stabilization of financial markets and recovery of key markets (i.e. the continued bottoming of key industrial commodities, more stable and rising stocks and aggressive recovery in oil).

Were they just that wrong, or are they doing their part in coordinating stimulus from last month’s G20 meeting?

Bryan Rich is a macro trader and co-founder of Billionaire’s Portfolio. If you’re looking for great ideas that have been vetted and bought by the world’s most influential and richest investors, join us at Billionaire’s Portfolio.

Intervention has been the common theme we’ve discussed for the better part of the past two months. And this week, that theme is heating up.

We’ve explained why oil at $30 has posed a threat to the global financial system and global economy. And we explained the parallels of the systemically threatening (current) oil price bust and the 2007-2008 housing bust. But we also noted the key differences, and why and how this “cheap oil” problem could be easily solved, unlike the housing bust.

Buffett’s famed annual letter is due to be released this weekend. With that, today we want to talk a bit about his record, his philosophy on markets and successful investing and the high conviction stocks that he has in his $130 billion plus Berkshire Hathaway stock portfolio.

First, only one living investor has a length of track record that can compare to Buffett’s. That’s fellow billionaire Carl Icahn. Icahn actually has a better record than Buffett, and it spans a little longer. But he gets a fraction of the attention of the man they call the Oracle of Omaha.(more…)

Today the rebound in oil led a significant turnaround for stocks. With that, the broader sentiment of uncertainty across markets tends to abate. Broader commodities swung from negative to positive. And yields on the U.S. 10-year Treasury, which were in deep decline this morning, swung to positive territory by the afternoon.

If you own stocks, a house, have a job or need to eat, you should cheer for higher oil prices.

As we’ve talked about quite a bit in recent weeks, cheap oil, at this point in the global economic recovery, is a catalyst to destabilize the global economy. While consumers gain a few bucks from cheaper gas, the oil industry leans closer to the edge of bankruptcies and weak oil exporting countries toward default. That would be very bad news (global financial crisis, round 2). So the longer we’re down here, and the more persistent these low levels appear, the riskier the world looks. And when the world looks risky, people sell stocks, and other relatively risky assets and they hold cash or buy U.S. Treasuries (which pushes yields lower).

For proof, here’s a look at the 10-year yield on the U.S. Treasury note.

Keep in mind, the Fed raised rates in December! They did so when the 10 year was trading at a yield of 2.20%. The yield is now 45 basis points lower. And even though a voting Fed member said yesterday that in her view, a second hike was still on the table for next month, the market has still virtually priced out the possibility of any further hikes for the rest of the year.

Why? Because other parts of the world are moving (or are moving deeper) into negative rate territory, because economic conditions continue to soften, mostly driven by sentiment and weakening inflation prospects. A big driver of that mix is the oil price crash.

In the next chart, you can see how yields, despite the December rate hike, have tracked oil lower.

Again, when people think the world looks risky, they pile into the safest parking place for capital on the planet, U.S. Treasuries –and that drives yields on Treasuries lower. While that flow of capital has certainly occurred, the pressure on yields from speculators is also a big component.

If you recall, we discussed a couple of weeks ago how markets can have it wrong – sometimes very wrong. If indeed, the market is wrong on this one, there is a tremendous opportunity to ride yields back to the 2.25% area. And it may be a violent move.

But oil will be the driver.

As we said, oil turned the tide for stocks today. Here’s a look at the relationship of oil and stocks over the past three months.

In this longer term chart above, you can get perspective on where oil prices stand relative to history. You can see in this chart the sharp rise, the sharp fall and the rebound from the depths of the global financial crisis.

That rebound was all China. China stepped in and used their three trillion dollars in foreign currency reserves AND their massive fiscal stimulus package to gobble up cheap commodities.

And you can see this most recent price crash was triggered by move by the Saudis to block an OPEC production cut in November 2014. It was the night of the Thanksgiving holiday in the U.S. and oil was trading about $73. We haven’t seen that price since.

The low at the depths of the financial crisis was 32.40. That’s about where oil closed today. We’ve made the case in recent weeks that, if OPEC refuses to cut production (likely), the central banks could/should step in and buy oil (the ECB, BOJ and/or China).

Bryan Rich is a macro trader and co-founder of Billionaire’s Portfolio,a subscription-based service that empowers average investors to invest alongside the world’s best billionaire investors.

People continue to blame softness in global markets on China. For years, there has been fear and speculation of “hard landing” for the Chinese economy.

When we talk about China, it’s all relative. China was growing at double digit pace for the better part of the past 25 years. Now Chinese growth has dropped to below 7%. That’s recession-like territory for the Chinese economy.

But the Chinese have powerful tools to promote growth. And we expect them to use those tools, sooner rather than later.

As we know their biggest and most effective tool is their currency. They ascended to the second largest economy in the world over the past two decades by massively devaluing their currency, and then pegging it at ultra-cheap levels. It allowed them to corner the world’s export market, sucking jobs and valuable foreign currency out of the developed world. This is precisely what Donald Trump is alluding to when he says “China is stealing from us.”

Interestingly though, it’s China, most recently, that has been getting hurt by currency. Over the past four years, the Bank of Japan has devalued their currency against the dollar by nearly 40%. And other export-driven emerging market economies have had massive declines in their currencies (Brazil, Mexico, Argentina, Russia). Given that China has actually been appreciating its currency against the dollar for the past 10 years (albeit gradually), they’ve given back a lot of ground on their export advantage.

Source: Reuters, Billionaire’s Portfolio

In the chart above, you can see the yen weakening dramatically against the dollar (the purple line moving higher = stronger dollar, weaker yen). The orange line is the dollar vs. the Chinese yuan. You can see the relative advantage that the BOJ’s QE program has created (the gap between the purple and orange lines). With that, the orange line rising, since 2014, represents China backing off of its pledge to appreciate its currency. They are fighting to preserve their export advantage by weakening the yuan again.

In August, they devalued by less than 2% in a day and global markets went haywire. That move is nothing extreme in currencies, especially an emerging market currency. But given China’s currency history and their policy stance, since 2005, to allow their currency to appreciate under a “managed float” (managing a daily range for the currency), it has markets confused. When people are confused, they “de-risk” or sell.

Now, China will likely continue this path. Our bet is that markets will finally realize that, in the shorter term, this will be good for global growth and good for the health and stability of global financial markets. Better growth in China, at this stage, is good.

Among their other tools to stimulate growth, China has interest rates. While most of the world is pegged at zero rates (or close to it, if not negative) China’s benchmark interest rate is still 4.35%. And their inflation rate is running 1.5%, well below their target of 3%. That’s a recipe for aggressive rate cuts, which would be a boon for the Chinese economy and for the global economy.

We have an explosive growth Chinese internet stock in our Billionaire’s Portfolio that is positioned to benefit from aggressive Chinese policy moves. We are following one of the best billionaire technology investors on the planet. He has a massive stake in the company. Click here to join us!

The word China is often thrown around to explain why markets are in turmoil. China doing well was a threat to western civilization. China doing poorly is now a threat to Western civilization.

Which one is true?

First, a bit of background. Over the past twenty years, China’s economy has grown more than fourteen-fold! … to $10 trillion. It’s now the second largest economy in the world.

During the same period, the U.S. economy has grown 2.5x in size.

So how did China achieve such an ascent and position in the global economy? One word: Currency.

To follow the stock picks of the world’s best billionaire investors, subscribe at Billionaire’s Portfolio.

For a decade, China maintained a fixed exchange rate policy — the yuan was pegged against the dollar. One U.S. dollar bought 8.27 yuan. This allowed China to undercut the rest of the world, churning out cheap commoditized goods, competing on one thing: Price.

But in 2005, China changed its currency policy. It abandoned the peg.

After political tensions rose between China and its key trading partners, namely the U.S., China adopted a “managed float.” Under this policy China agreed to let the yuan trade in a defined daily trading band, while gradually allowing it to appreciate. This was China’s way of pacifying its trading partners while maintaining complete control over its currency.

Over the next three years the Chinese yuan climbed 17 percent against the dollar, enough to ease a politically sensitive issue, but far less than the relative economic growth would warrant. In fact, China’s economy grew by 43 percent while the U.S. economy grew only 10 percent.

That timeline leads us up to the bursting of the global credit bubble. What caused it? The housing bubble can be credited to a key decision made by the government sponsored credit agencies (Fitch, Standard and Poors, Moody’s), all of which stamped AAA ratings on the mortgage bond securities that Wall Street was churning out.

With a AAA rating, massive pension funds couldn’t resist (if they wanted to keep their jobs) loading up on the superior yields these AAA securities were offering. That’s where the money came from. That’s the money that was ultimately creating the demand to give anyone with a pulse a mortgage. That mortgage was then thrown into a mix of other mortgages and the ratings agencies stamped them AAA. They rinsed and they repeated.

But where did all of the credit come from in the first place, to fuel the U.S. (and global) consumption, the stock market, jobs, investment, government spending … a lot of the drivers of the capital that contributed to the pin the pricked the global credit bubble (i.e. the U.S. housing bust)? It came from China.

China sells us goods. We give them dollars. They take our dollars and buy U.S. Treasuries, which suppresses U.S. interest rates, incentives borrowing, which fuels consumption. And the cycle continues. Here’s how it looked (and still looks):

The result: China collects and stockpiles dollars and perpetuates a cycle of booms and busts for the world.

That’s the structural imbalance in the world that led to the crisis, and that problem has yet to be solved. And the outlook, longer term, for a solution looks grim because it requires China to move to develop a more robust, and consumer led economy. That structural shift could take decades. And going from double digit growth to low single digit growth in the process is a recipe for social uprising of its billion plus people.

In the near term, the likelihood that China will fight economic weakness with a weaker currency is high. We’ve seen glimpses of it since August. And the hedge fund community is ramping up bets that it’s just starting, not ending.

Above is a look at the dollar vs the yuan chart (the line going lower represents yuan appreciation, dollar depreciation). Longer term, China’s weak currency policy is a threat to economic stability and geopolitical stability. But short term, it could be a shot in the arm for their economy and for the global economy.

To get our best of the best portfolio of billionaire owned stocks at our new Billionaire’s Portfolio, subscribe today.

The goal of the Billionaire’s Portfolio is simple: to provide retail investors with the same plain-vanilla stock investments that the world’s greatest billionaire investors and hedge funds own. And our subscribers can invest alongside these billionaires without the typical $5 million minimum investments and paying big hedge fund management and performance fees. Instead, they get access to our best of the best portfolio of billionaire owned stocks for just $297 a quarter.

As we headed into this past weekend, we talked about the threat that the oil bust poses to the global financial system (not too dissimilar from the housing bust), and we talked about the prospect of central bank intervention over the thinly traded U.S. holiday (Monday).

Both the Bank of Japan and the European Central Bank did indeed go on the offensive, verbally, promising more action to combat the shaky global financial market environment.

To follow the stock picks of the world’s best billionaire investors, subscribe at Billionaire’s Portfolio.

The result was a 9.5% rally in the Japanese stock market from Friday’s close. And all global markets followed suit. Within the white box in the chart below, you can see the central bank induced jump in the Nikkei (in orange) and the S&P 500 futures (in purple).

Source: Billionaire’s Portfolio

This is purely the influence on confidence by the two central banks that are now driving the global economic recovery (the BOJ and the ECB). However, the potency of the verbal threats and promises has been waning. Big words have marked bottoms along the way over the past several years for stocks, and the overall ebb and flow of global risk appetite. But it’s becoming more evident that real, bold action is required. And given that it’s cheap oil that represents the big risk to financial stability at the moment, we’ve argued that central banks should outright buy commodities (particularly oil). And we think they will.

Source: Billionaire’s Portfolio

In 2009, despite the evaporation of global demand, oil prices spiked from $32 to $73 in four months after China tapped its $3 trillion currency reserves to snap up cheap commodities. Within two years, oil was back above $100.

China’s role in the commodity market was a huge contributor to the recovery in emerging markets from the depths of the global financial and economic crisis. Brazil went from recession to growing at close to 8%. Many were saying emerging markets had survived the recession better than advanced markets, and that they were driving the global economic recovery. And Wall Street was claiming a torch passing from the developed world to the emerging world as the future of growth and leadership.

How are emerging markets doing now? Terrible. Not surprisingly, it turns out the emerging market economies need a healthy developed world to survive. And now with the additional hit of the plunge in commodity prices, Venezuela (heavily reliant on oil exports) is very near default. Brazil and Russia are both in recession. The longer oil prices stay down here, Venezuela will be the first domino to go, and others will follow. With that, we expect intervention to come. And as you can see in the response to the Nikkei overnight, it will pack a punch – and if it’s bold, a lasting one. Remember, as we said last week, historical turning points for markets often come from some form of intervention (public or private policy).

Billionairesportfolio.com, run by two veterans of the hedge fund industry, helps self-directed investors invest alongside the world’s best billionaire investors. To see which ideas we follow in our Billionaire’s Portfolio, join us at BillionairesPortfolio.com.

When housing prices stalled in 2006 and then collapsed over the next three years, the subprime lending schemes quickly became exposed.

Mortgage defaults led to a banking crisis. Due to the highly interconnectedness of banks globally, the problems quickly spread to banks around the world. A banking crisis led to a global credit freeze. When people can’t access credit, that’s when it all hits the fan. Companies can’t meet payroll, don’t have the liquidity to make new orders. Jobs get cut. Companies go bust. Finally, the microscope on overindebtedness of consumers and corporates, turns to countries. Deficits leads to debt. Debt leads to downgrades. Downgrades leads to defaults.

For the most part, defaults were averted because central banks and governments stepped in, in a coordinated way, to backstop failing banks, failing companies and failing countries. From that point, continued central bank stimulus has 1) enabled banks to recapitalize, 2) foiled additional shock events, and 3) restored confidence to employers (to hire), to investors (to invest) and to consumers (to spend again).

As we’ve discussed in the past two weeks, persistently low oil prices represent a risk on par with the housing bust. And in recent days we’re seeing the signs of another global financial and economic crisis creeping uncomfortably closer to a “part two.”

As we’ve said, this time would be much worse because governments and central banks have exhausted the resources to bailout failing banks, companies and countries. But central banks, namely the Bank of Japan and/or the European Central Bank do have the opportunity to step-in here, become an outright buyer of commodities (particularly oil), as part of their QE programs, to avert disaster. But time is the oil industries worst enemy and therefore a big threat to the global economy. The longer policymakers drag their feet, the closer we get to the edge of global crisis — a crisis manufactured by OPEC’s price war.

Unfortunately, there are the building signs that the market is beginning to position for the worst outcome…

Key bank stocks in Europe are trading at levels lower than in the depths of both the global financial crisis (2009) and the European sovereign debt crisis (2012).

Source: Reuters, Billionaire’s Portfolio

The credit default swap market for key industries is sending up flares. This is where default insurance can be purchased against a company or country – and the place speculators bet on a company’s demise. Billionaire John Paulson famously made billions betting against the housing market via credit default swaps. Now the fastest deteriorating companies in Europe are banks. And the fastest deteriorating companies in North America are insurance companies (a sector that tends to have investments in high yield debt … in this case, exposure to the high yield debt of the oil and gas industry).

Source: Markit

The early signal for the 2007-2008 financial crisis was the bankruptcy of New Century Financial, the second largest subprime mortgage originator. Just a few months prior the company was valued at around $2 billion.

On an eerily similar note, a news report hit this morning that Chesapeake Energy, the second largest producer of natural gas and the 12th largest producer of oil and natural gas liquids in the U.S., had hired counsel to advise the company on restructuring its debt (i.e. bankruptcy). The company denied that they had any plans to pursue bankruptcy and said they continue to aggressively seek to maximize the value for all shareholders. However, the market is now pricing bankruptcy risk over the next five years at 50% (the CDS market).

Still, while the systemic threat looks similar, the environment is very different than it was in 2008. Central banks are already all-in. On the one hand, that’s a bad thing for the reasons explained above (i.e. limited ammunition). On the other hand, it’s a good thing. We know, and they know, where they stand (all-in and willing to do whatever it takes). With QE well underway in Japan and Europe, they have the tools in place to put a floor under oil prices.

In recent weeks, both the heads of the BOJ and the ECB have said, unprompted, that there is “no limit” to what they can buy as part of their asset purchase program. Let’s hope they find buying up dirt-cheap oil and commodities, to neutralize OPEC, an easier solution than trying to respond to a “part two” of the global financial crisis.

Source: Billionaire’s Portfolio, Reuters

Source: Billionaire’s Portfolio, Reuters

{kind=link}