As we know, one of the pillars of the Trump administration’s growth policies has been deregulation. With that, today the head of the EPA signaled the withdrawal from the Clean Power Plan – an Obama regulation to fight climate change.

What does this mean for coal stocks?

Let’s take a look at the two largest American coal producers, both of which filed bankruptcy last year: Peabody Energy and Arch coal.

These are now two post-bankruptcy stocks!Peabody emerged from bankruptcy earlier this year after shedding about $5 billion in debt. Similar story for Arch coal. They filed early last year and emerged from bankruptcy late last year, eliminating $5 billion in debt in the process. So shareholders were wiped out and debt holders became stock holders in new low debt, cash flow positive companies with deregulation coming down the pike. With that, you would think the stocks would be screaming higher. That hasn’t been the case.

Here’s a look at the charts…

So we now have Peabody Energy, the leading coal producer in America with a $3 billion market cap. And Arch Coal, number two, has just a $1.7 billion market cap.

Are these cheap stocks?

Let’s take a look at who owns them…

The biggest shareholder in Peabody is billionaire Paul Singer’s hedge fund, Elliott Management. They own half a billion dollar’s worth of the stock and it’s a top ten position. As for ARCH – the top shareholder is the $5 billion hedge fund Monarch Alternative Capital. ARCH makes up 20% of their highly concentrated long equity portfolio (their biggest single stock position). If you’re going to dip your toe in the water on a post-bankruptcy stock, there are few better places to look for guidance than Paul Singer – a former attorney, turned one of the most influential and successful investors in the world.

As we head into the weekend, today I want to talk a bit about the 401k.

I’m looking today at a relatives 401k offering. Nothing has made Wall Street richer than the advent of the 401k. They get a constant monthly stream of fresh capital to skim fees and commissions from, and you get all of the market risk.

For the average person, selecting from the “options” in their 401k plan is a practice of picking the highest number. No surprise, the fund providers know that, and play plenty of games to show you the best numbers possible.

Here’s an example: As I’m looking through the limited choices in this particular 401k plan provider, there is a common theme in the “inception date” of most of the company’s mutual fund offerings. They tend to have track records that start in 2002 at or near the bottom of the internet bubble-induced stock market crash, OR they start in 2009 AFTER the 50% collapse in stocks, OR they start in late 1987 AFTER the crash.

Clearly the long-term returns will look quite a bit better when you’re starting from a bottom, after a crash. And clearly returns will look better without hanging a negative 30%-50% in 2008 and then another negative 30%-40% in the early 2000s.

Maybe they are newer, better strategies and had the good fortune of launching at the right time?

More often, they close them down and reopen them under a new, tweaked name. Add to that, they are constantly launching and running hundreds, if not thousands of funds, so that at any given time they can cherry pick the best performers over a certain period, to put them in front of a captive audience.

Bottom line: Big mutual fund giants are mass asset gatherers feeding on the passive 401k flow of capital, rather than astute investment managers. And the long term returns, after fees, prove it. People are locking their money up for a very long time, and getting a fraction of the market return.

When Congress invented the 401k in the 70s to transfer risk and obligations from the employer (traditional defined benefit pensions) to the employee (defined contributions), they didn’t do you any favors.

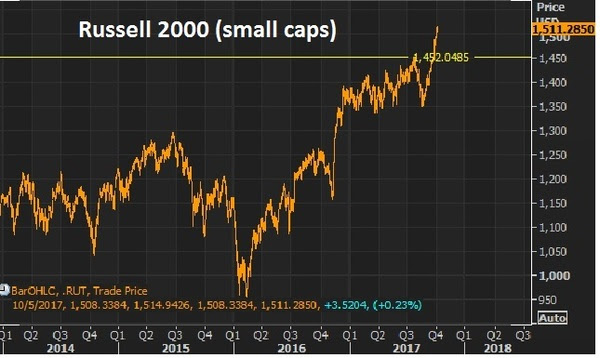

We looked at small caps last week when the the Russell 2000 broke to new highs.

Remember, at that point, small–caps had done only 9% on the year at this point. That’s against 13% for the S&P and Dow.

Here’s the chart now…

The Russell 2000 is now up 12% since the lows of August (up 11% ytd) and if you bought the small cap index on the Monday before the elections last year, you’re up 26%. But small caps continue to lag the bigger cap market. And that makes the last quarter a very intriguing opportunity to own small caps.

Bull markets tend to lift all boats. And with that, equal-dollar weighted small caps tend to outperform equal-dollar weighted large caps in bull markets (in some cases by a lot). This one (bull market) looks like plenty of room to go in that regard. And small cap companies should have more to gain from a corporate tax cut as the tend to have fewer ways to shelter income (relative to big multinationals).

Now, with that bull market assertion, let’s talk about the general uneasiness that seems to exist (and has for a while) from watching the continued climb in stocks.

As we’ve discussed, you often here the argument that the fundamentals don’t support the level of stocks. It’s just not true. The fundamental backdrop continues to justify and favor higher stocks. We have the prospects of fiscal stimulus building, which will be poured onto an already fertile economic backdrop — with low rates, cheap commodities, record consumer high credit worthiness and low unemployment.

As the old market adage goes, “bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” I don’t think anyone could argue we are currently in the state of euphoria for stocks. And as the great macro trader Paul Tudor Jones has said, “the last third of a great bull market is typically a blow-off, whereas the mania runs wild and prices go parabolic” (i.e. euphoria can last for a while).

Finally, let’s revisit this analysis from billionaire Larry Robbins on the influence of low interest rates, Fed policy and oilon markets. He says every time ONE of these (following) conditions has existed, the market has produced positive returns. Here they are:

When the 30 year bond yield begins the year below 4%, stocks go up 22.1%.

When investment grade bonds yield below 4%, stocks go up 16%.

When high yield bonds yield below 8%, stocks go up 11.6%.

When cash as a % of asset for non-financials is above 10%, stocks go up 17.6%.

When the Fed tightens 0-75 basis points in the year, stocks go up 22%.

When oil falls more than 20%, stocks go up 27.5%.

Again, his study showed that there has NEVER been a down year stocks, when any ONE of the above conditions is met.

It worked in 2015. It worked in 2016. And now, not only does ONE of these conditions exist, but ALL of these conditions are (or have been) met for 2017.

The media is giving more attention today to the potential change in power at the Fed. We talked about this on Monday. Remember, the President said last week that he expected an announcement to be made in the next two or three weeks on the future Fed Chair.

Along with any advancement on the fiscal stimulus front, the appointment of the next Fed Chair will be the most important news for markets and economy this year (though Yellen isn’t officially done until January of 2018).

Back in March I made the case for Trump ousting Yellen and hiring the Fed newbie, Neel Kashkari. Admittedly, I didn’t think Yellen would last this long. While Bernanke (the former Fed Chair) can be credited for averting a global apocalypse and keeping the patient alive, for as long as it took to bridge the gap to a real recovery. Under Yellen’s leadership, the Fed has been doing it’s best to kill the patient, at precisely the time the real recovery could be taking shape, with the assistance of fiscal stimulus finally in the works.

If the Fed continues on its path, borrowing costs (or, as importantly, the perception of where they may go) may strangle the economy before fiscal stimulus gets out of the gate. This is why I’ve said Kashkari should be the President’s best friend at the Fed. He’s the lone dissenter on the rate hiking path, and he’s been vocal about leaving monetary policy alone until the inflation data warrants a move.

Kashkari released an essay on Monday where he blames the Fed for creating its own low inflation surprise by tightening money and forecasting a tighter path for monetary policy, therefore creating a contractionary effect on the economy as consumers/businesses anticipated the negative effects of higher rates on the economy.

Guess who made this same case? Bernanke. He did so in a blog post last year, around this time. It was just as the world was spiraling into negative rates. He said the Fed shot itself in the foot by publishing an overly optimistic trajectory and timeline for normalizing rates. And that the communication alone resulted in an effective tightening.

This is why the ten year yield (still at just 2.34% after four rate hikes) is pricing in something that looks a lot more like recession than a hot economy.

With the above in mind, there has been a roster of candidates for Fed Chair floated today, which did not include Neel Kashkari. That was until word began to circulate that Jeff Gundlach, manager of the world’s biggest bond fund, said yesterday that he thinks Kashkari will get the nod, because he’s the most easy money guy. Still, it was refuted in the media that he was even a candidate.

Stocks open the week with another record high. The dollar continues to do better. And as we open the new month, yields are now up 32 basis points from the lows of early last month.

That’s a dramatic shift in the interest rate environment. And in recent days, underpinning that strength, is the idea that a hawk could be taking over for Janet Yellen when her term ends at the end of January.

Over the past few days the President has met with candidates for the Fed Chair job, and has said he will be announcing his decision in the next two to three weeks. That’s a big deal for markets and the economy — something to keep a close eye on.

His interview last Thursday was with a known hawk, former Fed governor Kevin Warsh – who has publicly criticized the Fed for keeping rates too low. He was also a hawk through some of the darkest days of the recovery – he’s been proven wrong for that view. As for Yellen: She has been among the most dovish Fed members throughout the crisis but has been leading the rate normalization phase (i.e. higher rates), which has proven to be questionable judgment, with missteps along the way resulting from the Fed’s overly optimistic and hawkish outlook.

Interestingly, though Trump criticized the Fed for keeping rates too low throughout the recovery, it’s higher rates, now, that are a significant threat to his growth policies. So he needs the Fed to step out of the way, and do no harm to the hand-off from a monetary policy-driven recovery, to a fiscal policy driven-recovery. Higher rates can choke off the positive effects of tax cuts and government spending.

On that note, his friend on monetary policy should be (and I think will be) Neel Kashkari (a new Fed member). Kashkari has been the lone dissenter on the Fed’s tightening path, arguing along the way to let the economy run hot, to ensure a robust recovery, before moving on rates.

Over the past two years, Yellen has blamed their pauses in their tightening program to the lack of evidence that the economy is overheating. It’s safe to say that the economy is not overheating (nor has it been), with both growth and inflation still undershooting long run averages.

With a Fed decision queued up for tomorrow, let’s take a look at how the rates picture has evolved this year.

The Fed has continued to act like speculators, placing bets on the prospects of fiscal stimulus and hotter growth. And they’ve proven not to be very good.

Remember, they finally kicked off their rate “normalization” plan in December of 2015. With things relatively stable globally, the slow U.S. recovery still on path, and with U.S. stocks near the record highs, they pulled the trigger on a 25 basis point hike in late 2015. And they projected at that time to hike another four times over the coming year (2016).

Stocks proceeded to slide by 13% over the next month. Market interest rates (the 10 year yield) went down, not up, following the hike — and not by a little, but by a lot. The 10 year yield fell from 2.33% to 1.53% over the next two months. And by April, the Fed walked back on their big promises for a tightening campaign. And the messaging began turning dark. The Fed went from talking about four hikes in a year, to talking about the prospects of going to negative interest rates.

That was until the U.S. elections. Suddenly, the outlook for the global economy changed, with the idea that big fiscal stimulus could be coming. So without any data justification for changing gears (for an institution that constantly beats the drum of “data dependence”), the Fed went right back to its hawkish mantra/ tightening game plan.

With that, they hit the reset button in December, and went back to the old game plan. They hiked in December. They told us more were coming this year. And, so far, they’ve hiked in March and June.

Below is how the interest rate market has responded. Rates have gone lower after each hike. Just in the past couple of days have, however, we returned to levels (and slightly above) where we stood going into the June hike.

But if you believe in the growing prospects of policy execution, which we’ve been discussing, you have to think this behavior in market rates (going lower) are coming to an end (i.e. higher rates).

As I said, the Hurricanes represented a crisis that May Be The Turning Point For Trump. This was an opportunity for the President to show leadership in a time people were looking for leadership. And it was a chance for the public perception to begin to shift. And it did. The bottom was marked in Trump pessimism. And much needed policy execution has been kickstarted by the need for Congress to come together to get the debt ceiling raised and hurricane aid approved. And I suspect that Trump’s address to the U.N. today will add further support to this building momentum of sentiment turnaround for the administration. With this, I would expect to hear a hawkish Fed tomorrow.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

As I said on Friday, people continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

We constantly hear about how the fundamentals don’t support the move in stocks. Yet, we’ve looked at plenty of fundamental reasons to believe that view (the gloom view) just doesn’t match the facts.

Remember, the two primary sources that carry the megahorn to feed the public’s appetite for market information both live in economic depression, relative to the pre-crisis days. That’s 1) traditional media, and 2) Wall Street.

As we know, the traditional media business, has been made more and more obsolete. And both the media, and Wall Street, continue to suffer from what I call “bubble bias.” Not the bubble of excess, but the bubble surrounding them that prevents them from understanding the real world and the real economy.

As I’ve said before, the Wall Street bubble for a very long time was a fat and happy one. But the for the past ten years, they came to the realization that Wall Street cash cow wasn’t going to return to the glory days. And their buddies weren’t getting their jobs back. And they’ve had market and economic crash goggles on ever since. Every data point they look at, every news item they see, every chart they study, seems to be viewed through the lens of “crash goggles.” Their bubble has been and continues to be dark.

Also, when we hear all of the messaging, we have to remember that many of the “veterans” on the trading and the news desks have no career or real-world experience prior to the great recession. Those in the low to mid 30s onlyknow the horrors of the financial crisis and the global central bank sponsored economic world that we continue to live in today. What is viewed as a black swan event for the average person, is viewed as a high probability event for them. And why shouldn’t it? They’ve seen the near collapse of the global economy and all of the calamity that has followed. Everything else looks quite possible!

Still, as I’ve said, if you awoke today from a decade-long slumber, and I told you that unemployment was under 5%, inflation was ultra-low, gas was $2.60, mortgage rates were under 4%, you could finance a new car for 2% and the stock market was at record highs, you would probably say, 1) that makes sense (for stocks), and 2) things must be going really well! Add to that, what we discussed on Friday: household net worth is at record highs, credit growth is at record highs and credit worthiness is at record highs.

We had nearly all of the same conditions a year ago. And I wrote precisely the same thing in one of my August Pro Perspective pieces. Stocks are up 17% since.

And now we can add to this mix: We have fiscal stimulus, which I think (for the reasons we’ve discussed over past weeks) is coming closer to fruition.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We’ve past yet another hurdle of concern for markets this past week. Last Friday this time, we had a potential catastrophic category 5 hurricane projected to decimate Florida.

Though there was plenty of destruction in Irma’s path, the weakening of the storm through the weekend ended in a positive surprise relative what could have been.

So we end with stocks on highs. And remember, we’ve talked over past month about the quiet move in copper (and other base metals) as a signal that the global economy (and especially China) might be stronger than people think. Reuters has a piece today where they overlay a chart of economist Ed Yardeni’s “boom-bust barometer” over the S&P 500. It looks like the same chart.

What does that mean? The boom-bust barometer measures the strength of industrial commodities relative to jobless claims. Higher commodities prices and lower unemployment claims equals a rising index as you might suspect (i.e. suggesting economic boom conditions, not bust). And that represents the solid fundamental back drop that is supporting stocks.

With that in mind, consider this: In the recent earnings quarter, earnings and revenue growth came in as good as we’ve seen in a long time for S&P 500 companies. We have 4.4% unemployment. The rise in equities and real estate have driven household net worth to $94 trillion – new record highs and well passed the pre-crisis peaks (chart below).

Now, people love to worry about debt levels. It’s always an eye-catching headline.

But what happens to be the key long-term driver of economic growth over time? Credit creation (debt). The good news: The appetite for borrowing is back. And you can see how closely GDP (the purple line, economic output) tracks credit growth.

Meanwhile, and importantly, consumers have never been so credit worthy. FICO scores in the U.S. have reached all-time highs. So despite what the media and some of Wall Street are telling us, things look pretty darn good. Low interests have produced recovery, without a ramp up in inflation.

But as I’ve said, it has proven to have its limits. We need fiscal stimulus to get us over the hump – on track for a sustainable recovery. And we now have, over the past two weeks, improving prospects that we will see fiscal stimulus materialize — i.e. policy execution in Washington.

To sum up: People continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

Yesterday we looked at the charts on oil and the U.S. 10 year yield. Both were looking poised to breakout of a technical downtrend. And both did so today.

Here’s an updated look at oil today.

And here’s a look at yields.

We talked yesterday about the improving prospects that we will get some policy execution on the Trumponomics front (i.e. fiscal stimulus), which would lift the economy and start driving some wage pressure and ultimately inflation (something unlimited global QE has been unable to do).

No surprise, the two most disconnected markets in recent months (oil and interest rates) have been the early movers in recent days, making up ground on the divergence that has developed with other asset classes.

Now, oil will be the big one to watch. Yields have a lot to do, right now, with where oil goes.

Though the central banks like to say they look at inflation excluding food and energy, they’re behavior doesn’t support it. Oil does indeed play a big role in the inflation outlook – because it plays a huge role in financial stability, the credit markets and the health of the banking system. Remember, in the oil price bust last year the Fed had to reverse course on its tightening plan and other major central banks coordinated to come to the rescue with easing measures to fend off the threat of cheap oil (which was quickly creating risk of another financial crisis as an entire shale industry was lining up for defaults, as were oil producing countries with heavy oil dependencies).

So, if oil can sustain above the $50 level, watch for the inflation chatter to begin picking up. And the rate hike chatter to begin picking up (not just with the Fed, but with the BOE and ECB). Higher oil prices will only increase this divergence in the chart below, making the interest rate market a strong candidate for a big move.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

After a week away, I return to markets that look very similar to where we left off 10 days ago. Stocks lower. Yields lower. The dollar lower. But commodities higher!

Now, this takes into account, another week of political volatility in Washington. It takes into account another week of uncertainty surrounding North Korea.

What’s important here, is distinguishing between a price correction and a real thematic change. If we’re not making new record highs in stocks every day, and stocks actually retrace 5% or so, does that represent the derailing of the slow but steady economic recovery and, as important, the dismissal of potential policy fuel that could finally lift us out of the post-crisis stall speed growth regime?

The narrative in the media would have you believe the answer is yes.

But the reality is, the economic recovery is stable and continuing. The policy stimulus has been a tough road, but continues to offer positive influence on the economy. And there are strong technical reasons to believe we’re seeing the early stages of a price driven correction in stocks.

Remember, we looked at the big technical reversal signal (the “outside day”) back on August 8th. That was the technical signal, and it was about as good a signal as it gets. The Dow had been plowing to new highs for eleven consecutive days — culminating in another new record high before. And the last good ‘outside day’ in the S&P 500 was into the rally that stalled December 2, 2015 and it resulted in a 14% correction.

Here’s another look at that chart, plus the first significant trend line that we discussed in my last note, August 11th.

I thought this line would give way, which it has today, and that we would see a real retracement, which should be a gift to buy stocks. If you’re not a highly leveraged hedge fund, a 5%-10% retracement in broader stocks is a gift to buy. Remember, the slope of the S&P 500 index over time is UP.

Prior to the reversal signal in stocks, we had already addressed the influence of the FAANG stocks. And I suggested the miss in Amazon earnings was a good enough excuse to cue the profit taking in what had been a very lucrative trade in the institutional investment community. Amazon is now down 12% from the highs of just 18 days ago.

What should give you confidence that the economic outlook isn’t souring? Commodities!

The base metals, as we’ve discussed in recent weeks, continue to move higher and continue to look like early stages of a bull market cycle — which would support the idea that the global economic recovery is not only on track, but maybe better than the consensus market view (which seems to be still unconvinced that better times are ahead).

The leader of the commodities run is copper. We looked at this chart in my last note (Aug 11). I said, “this big six-year trend line in copper (below) will be one to watch closely. If it breaks, it should lead the commodities trend higher.”

Here’s an updated chart of Copper. This trend line was broken today.

Join me in our Billionaire’s Portfolio and get my recommendation on a commodities stock with potential to be a six-fold winner in the commodities recovery. Click here to learn more.

As we know, one of the pillars of the Trump administration’s growth policies has been deregulation. With that, today the head of the EPA signaled the withdrawal from the Clean Power Plan – an Obama regulation to fight climate change.

As we know, one of the pillars of the Trump administration’s growth policies has been deregulation. With that, today the head of the EPA signaled the withdrawal from the Clean Power Plan – an Obama regulation to fight climate change.