After a week away, I return to markets that look very similar to where we left off 10 days ago. Stocks lower. Yields lower. The dollar lower. But commodities higher!

Now, this takes into account, another week of political volatility in Washington. It takes into account another week of uncertainty surrounding North Korea.

What’s important here, is distinguishing between a price correction and a real thematic change. If we’re not making new record highs in stocks every day, and stocks actually retrace 5% or so, does that represent the derailing of the slow but steady economic recovery and, as important, the dismissal of potential policy fuel that could finally lift us out of the post-crisis stall speed growth regime?

The narrative in the media would have you believe the answer is yes.

But the reality is, the economic recovery is stable and continuing. The policy stimulus has been a tough road, but continues to offer positive influence on the economy. And there are strong technical reasons to believe we’re seeing the early stages of a price driven correction in stocks.

Remember, we looked at the big technical reversal signal (the “outside day”) back on August 8th. That was the technical signal, and it was about as good a signal as it gets. The Dow had been plowing to new highs for eleven consecutive days — culminating in another new record high before. And the last good ‘outside day’ in the S&P 500 was into the rally that stalled December 2, 2015 and it resulted in a 14% correction.

Here’s another look at that chart, plus the first significant trend line that we discussed in my last note, August 11th.

I thought this line would give way, which it has today, and that we would see a real retracement, which should be a gift to buy stocks. If you’re not a highly leveraged hedge fund, a 5%-10% retracement in broader stocks is a gift to buy. Remember, the slope of the S&P 500 index over time is UP.

Prior to the reversal signal in stocks, we had already addressed the influence of the FAANG stocks. And I suggested the miss in Amazon earnings was a good enough excuse to cue the profit taking in what had been a very lucrative trade in the institutional investment community. Amazon is now down 12% from the highs of just 18 days ago.

What should give you confidence that the economic outlook isn’t souring? Commodities!

The base metals, as we’ve discussed in recent weeks, continue to move higher and continue to look like early stages of a bull market cycle — which would support the idea that the global economic recovery is not only on track, but maybe better than the consensus market view (which seems to be still unconvinced that better times are ahead).

The leader of the commodities run is copper. We looked at this chart in my last note (Aug 11). I said, “this big six-year trend line in copper (below) will be one to watch closely. If it breaks, it should lead the commodities trend higher.”

Here’s an updated chart of Copper. This trend line was broken today.

Join me in our Billionaire’s Portfolio and get my recommendation on a commodities stock with potential to be a six-fold winner in the commodities recovery. Click here to learn more.

James Bullard, the President of the St. Louis Fed, said today that even if unemployment went to 3% it would have little impact on the current low inflationevironment. That’s quite a statement. And with that, he argued no need to do anything with rates at this stage.And he said the low growth environment seems to be well intact too — even though we well exceeded the target the Fed put on employment years ago. In the Bernanke Fed, they slapped a target on unemployment at 6.5% back in 2012, which, if reached, they said they would start removing accomodation, including raising rates. The assumption was that the recovery in jobs to that point would stoke inflation to the point it would warrant normalization policy. Yet, here we are in the mid 4%s on unemployment and the Fed’s favored inflation guage has not only fallen short of their 2% target, its trending the other way (lower).

As I’ve said before, what gets little attention in this “lack of inflation” confoundment, is the impact of the internet. With the internet has come transparency, low barriers-to-entry into businesses (and therefore increased competition), and reduced overhead. And with that, I’ve always thought the Internet to be massively deflationary. When you can stand in a store and make a salesman compete on best price anywhere in the country–if not world–prices go down.

And this Internet 2.0 phase has been all about attacking industries that have been built upon overcharging and underdelivering to consumers. The power is shifting to the consumer and it’s resulting in cheaper stuff and cheaper services. And we’re just in the early stages of the proliferation of consumer to consumer (C2C) business — where neighbors are selling products and services to other neighbors, swapping or just giving things away. It all extracts demand from the mainstream business and forces them to compete on price and improve service. So we get lower inflation. But maybe the most misunderstood piece is how it all impacts GDP. Is it all being accounted for, or is it possible that we’re in a world with better growth than the numbers would suggest, yet accompanied by very low inflation?

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

As we know, inflation has been soft. Yet the Fed has been moving on rates, assuming that they have room to move away from zero without counteracting the same data that is supposed to be driving their decision to increase rates.

Thus far, after four (quarter point) increases to the Fed funds rate, the moves haven’t resulted in a noticeable tightening of financial conditions. That’s mainly because the interest rate market that most key consumer rates are tied to have remained low. Because inflation has remained low.

A key contributor to low inflation has been low oil prices (though the Fed doesn’t like to admit it) and commodity prices in general that have yet to sustain a recovery from deeply depressed levels (see the chart below).

But that may be changing.

Commodities have been lagging the rest of the “reflation” trade after the value of the index was cut in half from the 2011 highs. Remember, we looked at this divergence between the stocks and commodities last month. Commodities are up 6% since.

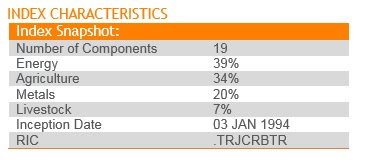

Things are picking up. Here’s the makeup of the broadly followed commodities index.

You can see, energy has a heavy weighting. And oil, with another strong day today, looks like a break out back to the $50 level is coming.With today’s inventory data, we’ve now had 12 out of the past 14 weeks that oil has been in a draw (drawing down on supply = bullish for prices). And with that backdrop, the CRB index, after being down as much as 13% this year, bottomed following the optimistic central bank commentary last month, and is looking like it may be in the early stages of a big catch-up trade. And higher oil (and commodity prices in general) will likely translate into higher inflation expectations.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

With some global stock barometers hitting new highs this morning, there is one spot that might benefit the most from this recently coordinated central bank promotion of a higher interest environment to come. It’s Japanese stocks.

First, a little background: Remember, in early 2016, the BOJ shocked markets when it cut its benchmark rate below zero. Counter to their desires, it shook global markets, including Japanese stocks (which they desperately wanted and needed higher). And it sent capital flowing into the yen (somewhat as a flight to safety), driving the value of the yen higher and undoing a lot of the work the BOJ had done through the first three years of its QE program. And that move to negative territory by Japan sent global yields on a mass slide.

By June, $12 trillion worth of global government bond yields were negative. That put borrowers in position to earn money by borrowing (mainly you are paying governments to park money in the “safety” of government bonds).

The move to negative yields, sponsored by Japan (the world’s third largest economy), began souring global sentiment and building in a mindset that a deflationary spiral was coming and may not be leaving, ever—for example, the world was Japan.

And then the second piece of the move by Japan came in September. It was a very important move, but widely under-valued by the media and Wall Street. It was a move that countered the negative rate mistake.

By pegging its ten-year yield at zero, Japan put a floor under global yields and opened itself to the opportunity to doing unlimited QE. They had the license to buy JGBs in unlimited amounts to maintain its zero target, in a scenario where Japan’s ten-year bond yield rises above zero. And that has been the case since the election.

The upward pressure on global interest rates since the election has put Japan in the unlimited QE zone — gobbling up JGBs to push yields back down toward zero — constantly leaning against the tide of upward pressure. That became exacerbated late last month when Draghi tipped that QE had done the job there and implied that a Fed-like normalization was in the future.

So, with the Bank of Japan fighting a tide of upward pressure on yields with unlimited QE, it should serve as a booster rocket for Japanese stocks, which still sit below the 2015 highs, and are about half of all-time record highs — even as its major economic counterparts are trading at or near all-time record highs.

Without a doubt, there was a significant shift in the outlook on central bank monetary policy this week. In fact, the events of the week may represent the official market acceptance of the “end of the easy money” era.

Draghi told us deflation is over and reflation is on. Yellen told us we should not expect another financial crisis in our lifetimes. Carney at the Bank of England told us removal of stimulus is likely to become necessary, and up for debate “in the coming months.” And even the Finance Minister in Japan joined in, saying Japan was recovery from deflation.

With that, in a world where “reflation” is underway, rates and commodities lead the way.

Here’s a look at the chart on the 10-year yield again. We looked at this on Tuesday. I said, the “Bottom May Be In For Oil and Yields.” That was the dead bottom. Rates bounced hard off of this line we’ve been watching …

This reflation theme confirmed by central banks has put a bid under commodities…

That’s especially important for oil, which had been trading down to very dangerous levels, the levels that begin threatening the solvency of oil producers.

That’s a 9% bounce for oil from the lows of last week!

This all looks like the beginning of another leg of recovery for commodities and rates (with the catalyst of this central bank guidance). Which likely means a lower dollar (as we discussed earlier this week). And a quieter broad stock market (until growth data begins to reflect a break out of the sub 2% GDP funk).

Have a great weekend.

Join the Billionaire’s Portfolioto hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

Yesterday we talked about the Draghi remarks (head of the European Central Bank) that were intended to set expectations that the ECB might be moving toward the exit doors on QE and zero interest rate policy. That bottomed out global rates — which popped U.S. rates further today. The Bank of England piled on today, talking about rate normalization soon.

We’ve gone from 2.12% in the U.S. ten year yield to 2.25% in about 24 hours. These are big swings in the interest rate market – a big bounce and, as I’ve said, the bottom appears to be in for rates.

As importantly, this prepared speech by Draghi could very well cement the top in the dollar. It begins to tighten a very wide interest rate spread between the U.S. and global rates. We entered the year with the Fed going one way (tightening) while the rest of the world was going the other way (easing). That’s a recipe for capital to storm into U.S. assets — into the dollar. And now that may be over.

I’ve been researching long-term cycles in the dollar for a very long time and throughout the global financial crisis period, it these cycles in the world’s reserve currency have been my guidepost for drawing a lot of conclusions on markets and the outlook for capital flows over the past several years.

Despite the choppiness in the dollar for much of the crisis, if we look back at the cycles following the failure of the Bretton Woods system, we were able, very early on, to determine the dollar was in a bull cycle.

This view came in the face of all of the negative global sentiment toward the dollar in 2010. Foreign leaders were taking shots at the Fed, accusing the Fed of trying to destroy the dollar. People were calling for the end of the dollar as the world’s reserve currency. All the while, the dollar held firm and ultimately made an aggressive climb.

Take a look below at my chart on the long term dollar cycles…

I’ve watched this chart for quite some time, defining the five complete dollar cycles over the past nearly 40 years, and the most recent bull cycle.

If we mark the top of the most recent cycle in early January, this bull cycle has matched the longest cycle in duration (at 8.8 years) and comes in just shy of the long-term average performance of the five complete cycles. The most recent bull cycle added 47%. The average change over a long term cycle has been 56%. This all argues that the dollar bull cycle is over. And a weaker dollar is ahead. That should go over very well with the Trump administration.

Join the Billionaire’s Portfolioto hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

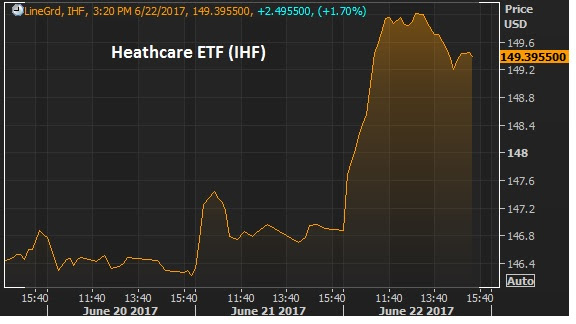

Healthcare was the story of the day today. With the Senate having had its go at the house healthcare bill, it goes back to the house, then back through Senate before it gets to the President’s desk.

Still, policy progression is very positive in this environment. Healthcare stocks were up big today — the IHF healthcare ETF was up over 2%. This is the ETF that tracks insurers, diagnotic and specialized treatment companies.

And despite all of the debate around healthcare, it has been the hottest sector to invest in since the election.Since election day, the IHF is up 35% since the lows of November 9th, the day after the election. Here’s a look at S&P sector performance over the past sixmonths.

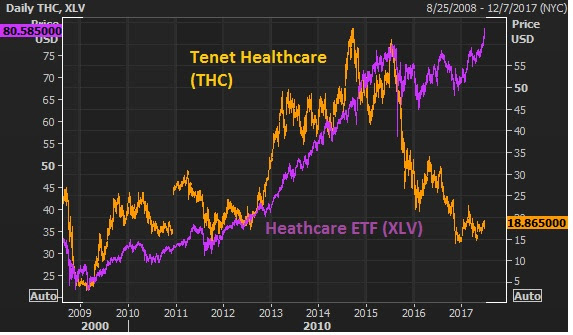

Most interesting, the healthcare sector has been beaten up badly since the cracks in Obamacare became clear back in 2014. But as of the past week, the healthcare sector trackers have finally broken back above those 2014 Obamacare–optimism–driven highs. With that, the divergence in this next chart of one of the biggest hospital companies in the country becomes quite an intriguing trade.

Join the Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

Today I want to take a look back at my March 7th Pro Perspectives piece. And then I want to talk about why a power shift in the economy may be underway (again).

Big Picture .. Market Perspectives March 7, 2017

“A big component to the rise of Internet 2.0 was the election of Barack Obama. With a change in administration as a catalyst, the question is: Is this chapter of the boom in Silicon Valley over? And is Snap the first sign?

Without question, the Obama administration was very friendly to the new emerging technology industry. One of the cofounders of Facebook became the manager of Obama’s online campaign in early 2007, before Obama announced his run for president, and just as Facebook was taking off after moving to and raising money in Silicon Valley (with ten million users). Facebook was an app for college students and had just been opened up to high school students in the months prior to Obama’s run and the hiring of the former Facebook cofounder. There was already a more successful version of Facebook at the time called MySpace. But clearly the election catapulted Facebook over MySpace with a very influential Facebook insider at work. And Facebook continued to get heavy endorsements throughout the administration’s eight years.

In 2008, the DNC convention in Denver gave birth to Airbnb. There was nothing new about advertising rentals online. But four years later, after the 2008 Obama win, Airbnb was a company with a $1 billion private market valuation, through funding from Silicon Valley venture capitalists. CNN called it the billion dollar startup born out of the DNC.

Where did the money come from that flowed so heavily into Silicon Valley? By 2009, the nearly $800 billion stimulus package included $100 billion worth of funding and grants for the “the discovery, development and implementation of various technologies.” In June 2009, the government loaned Tesla $465 million to build the model S.

When institutional investors see that kind of money flowing somewhere, they chase it. And valuations start exploding from there as there becomes insatiable demand for these new ‘could be’ unicorns (i.e. billion dollar startups).

Who would throw money at a startup business that was intended to take down the deeply entrenched, highly regulated and defended taxi business? You only invest when you know you have an administration behind it. That’s the only way you put cars on the street in NYC to compete with the cab mafia and expect to win when the fight breaks out. And they did. In 2014, Uber hired David Plouffe, a senior advisor to President Obama and his former campaign manager to fight regulation. Uber is valued at $60 billion. That’s more thanthree times the size of Avis, Hertz and Enterprise combined.

Will money keep chasing these companies without the wind any longer at their backs?”

Now, this was back in March. And that was the question — will it keep going under Trump? Can they continue to thrive/ if not survive without policy favors. Most importantly for the billion dollar startup world, will the private equity capital dry up. This is what it’s really all about. Will the money that chased the subsidies from D.C. to Silicon Valley for eight years (i.e. the trillion dollar pension funds) stop flowing? And will it begin chasing the new favored industries and policies under the Trump administration?

It seems to be the latter. And it seems to be happening in the form of a return to the public markets — specifically, the stock market.

And it may be amplified because of the huge disparity in what is being favored. In Silicon Valley, innovation is favored. Profitability? Remember, the 90s tech bubble. The measure of success for those companies was “eyeballs.” How much traffic were they getting to their websites? Today, when you hear a startup founder talk about the success benchmarks, it rarely has anything to do with with revenue or profit. It’s all about headcount (how many people they’ve hired) and money raised (which enables them to hire people). They are validated by convincing investors to fund them (mostly with our pension money).

Now, the other side of this coin: Trumponomics. Remember, among the Trump policies (corporate tax cuts, repatriation, deregulation, infrastructure spend), the most common sense play in the stock market has been flooding money into companies that make a lot of money. Those that make a lot of money have the most to gain from a slash in the corporate tax rate — it falls right to the bottom line. Leading the way on that front, is Apple. They make a lot of money. And they will make a lot more when a tax cut comes, making the stock even cheaper. That’s why it’s up 25% year-to-date. That’s 2.5 times the performance of the broader market.

Meanwhile, let’s take a look back at the Snapchat. Snapchat doesn’t make money. And even after a 1/3 haircut on the valuation, trades about 35 times revenue. And now, as a public company, probably doesn’t get the protection from the venture capital/private equity community that may have significant investments in its competitors. So the competitors (like Facebook) are circling like sharks to copy their business.

What about Uber? The Uber armor may be beginning to crack as well, with the leadership shakeup in recent weeks. Maybe a good signal for how Uber may be doing? Hertz! Hertz has bounced about 20% from the bottom this week.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

The Nasdaq trade unwound some today. From the peak this morning in the futures of 5898 the tumble started around 11am, falling to as low as 5660. That’s 238 Nasdaq futures points or 4% – quite a sharp move.

Remember, it seems like an overdone trade (driven by the big tech stocks). But as we discussed last week, the tech heavy Nasdaq has simply been a catch up trade — something that has lagged the strength in the broader market.

Here’s the chart we looked at last week.

This chart goes back to the lows driven by the oil price crash that bottomed out earlier last year.

Still, with the Nasdaq at +18% ytd and S&P 500 +9% ytd, as of this morning, as we’ve seen many times in this post-crisis era, the air pockets of illiquidity in stocks can give back gains very, very quickly. As they say, stocks go up on an escalator and down in an elevator.

The Trump trend, in the chart above, was nearly tested today — the same day a new all-time high was marked!

If we get another few days of sharp downside, it will be a tremendous buying opportunity – get your shopping list ready. And if that downside slide does indeed come, it could come at a very interesting time. It would add another (but very signficant) reason the Fed may balk on a rate hike next week. The other reasons? We discussed them yesterday (here).

Have a great weekend.

What stocks should be on your shopping list, to buy on a big market dip? Join my Billionaire’s Portfolio to find out. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

Last week we looked at the some of the clear evidence that the economy is as primed as it can possibly get for a catalyst to come in and pop growth.That catalyst, despite all of the scrutiny, will be Trumponomics.

At the very least, a corporate tax cut will directly hit the bottom line of corporate America. And one of the huge drags on demand, structurally, is the lack of wage growth. And as we discussed, the big winner in a corporate tax cut will be workers/wage growth — a non-partisan tax think tank thinks it can pop wage growth, by as much as doublethe current growth rate. That would be huge, especially for one of the key pillars of the recovery — housing.Remember, the two biggest drivers of recovery have been: 1) stocks, and 2) housing. Those two assets have done the lion’s share of work when it comes to restoring confidence. And a lot of other key pieces fall into place when confidence comes back.

On the housing front, over the past year, both mortgage rates and house prices have gone UP – a new dynamic in the post crisis recovery (adding higher rates into the mix). So owning a house has become more expensive over the past year. But how much?

Let’s take a look at how that has affected the monthly outlay for new homeowners over the course of the past year.

From March 2016 to March 2017, the average 30 year fixed mortgage went from 3.70% to 4.20%.

The Case-Shiller housing price index of the top 20 markets in the U.S. is up 6% over that twelve month period (the most recent data). That’s increased the monthly outlay (principal and interest) for new homeowners by 11% over the past year.

Now, with that said, we look at the recent behavior of the 10 year note (the benchmark government bond yield that heavily influences mortgage rates). It’s been in world of its own — sliding back to seven month lows, while stocks are hitting record highs. Manipulation? Likely. As I’ve said before, don’t underestimate the value of QE that is still in full force around the world — namely in Japan and Europe. That’s freshly printed money that can continue to buy our Treasuries, keeping a cap on interest rates, which keeps a cap on mortgage rates, which keeps the housing recovery and the recovery in consumer credit demand intact.

What stocks are cheap?Join me today to find out what stocks I’m buying in my Billionaire’s Portfolio. It’s risk-free. If for any reason you find it doesn’t suit you, just email me within 30-days.

With some global stock barometers hitting new highs this morning, there is one spot that might benefit the most from this recently coordinated central bank promotion of a higher interest environment to come. It’s Japanese stocks.

With some global stock barometers hitting new highs this morning, there is one spot that might benefit the most from this recently coordinated central bank promotion of a higher interest environment to come. It’s Japanese stocks.