Oil is up over 3% today, trading up to the highest levels since June of 2015.

We were already at new highs for the year as of Friday’s close, and then we get news over the weekend of the political shakeup and arrests in Saudi Arabia.

We’ve talked about the fundamental case for much higher oil prices throughout the recovery last year, and again this summer. You never know what catalyst may come in to accelerate the move in price. We may have had it with this Saudi news.

Among the reasons to expect a potential violent move in oil prices: OPEC has been cutting production into a (ex OPEC, ex U.S.) world that’s not producing (i.e. there’s negative production growth). Given the scars of last year’s oil price bust, oil producers haven’t been spending on new production.

Meanwhile, there’s U.S. supply that is supposed to fill that void, but U.S. supply has been in consistent draw down, 26 of the past 31 weeks, to the tune of 8% lower supply.

Add to this, we have a global economy that’s improving, and with that, demand is increasing. And we have U.S. fiscal stimulus entering to stoke those flames.

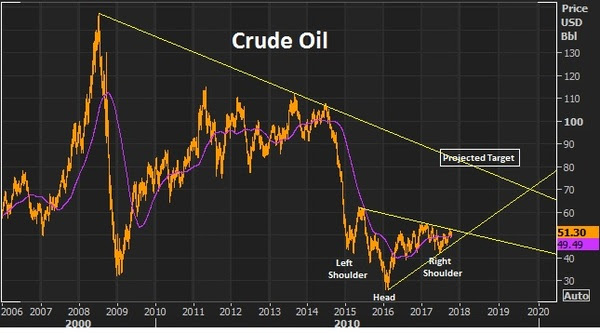

We looked at this chart last month.

Source: Billionaire’s Portfolio

We had this this inverse head and shoulders (in the chart above) that projected a move back to the low $80s. And as part of that technical picture, we were setting up for a break of a big two-year trendline that would open the doors to a move back into the $70+ oil area.

That line broke at around $51.50, confirming that head and shoulders pattern, and the move has been aggressive since. We now have this chart …

Source: Billionaire’s Portfolio

This is beginning to play out according to script for the star commodity investors we talked about this summer, Leigh Goehring and Adam Rozencwajg. They’ve been wildly bullish oil calling for $75 to $110 oil. Earlier in the summer, they said “when inventory gets this low we run the risk of triple digit oil prices.” And they suspected a supply disruption could give us a sharp move higher.

Do the events in Saudi Arabia present a potential supply disruption? Earlier this year, Stratus Advisors, an energy research and consulting shop, projected potential oil-supply disruption scenarios. Among the scenarios, was “internal instability in Saudi Arabia.”

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Over the past two weeks we’ve talked about the two big central bank events. The first was the ECB’s decision last week. As expected, they signaled they will be exiting QE. The second was the anticipated announcement of a new Fed chair. This is a high consequence decision.

I thought early on that the President would show Yellen the door, given that the rate hiking campaign she has been leading at the Fed poses a threat to choke off the impact of the big fiscal stimulus efforts that have been the hallmark of the Trump Presidency.

She stayed longer than I expected. But today we get her replacement: the current voting Fed governor Jerome Powell. Powell has voted with Yellen, along the way. So, it doesn’t appear to be a philosophical change and it doesn’t appear to be a person Trump can influence – but he offers the President party alignment.

I thought Neel Kashkari had postured perfectly to get the job. He has experience at the Treasury overseeing the TARP program through the ugliest period of the financial crisis. And he’s a newbie Fed governor, but one that has dissented on rate hikes and argued to wait for inflation to take hold before moving on rates (to ensure sustainability of the recovery). That view aligns much friendlier with the Trump administrations economic plan.

The Fed chair role was, arguably (unquestionably, to me), the most important role in the world under the Bernanke reign. Bernanke was the right guy, in the right place, at the right time. As a student of the Great Depression he led the Fed through decisions that pulled the world back from the edge of total collapse. At stages through the crisis, the Fed and Bernanke took a lot of heat – and a lot of it came from world leaders, and even global central banks. But had the Fed not swiftly acted to help foreign banks early on (that were frozen from the lack of access of U.S. dollars), the global financial system would have imploded.

Other central banks then underestimated the scale of the crisis and started hiking rates too early, in 2010 and 2011, which ultimately put them back in to recession (most notably, Europe). The Fed stayed put.

Over time, Bernanke’s Fed (and his aggressive QE) proved to be right, and ultimately provided the playbook for major central banks to follow.

Under the Yellen regime, the track record has been spotty, nearly killing the recovery last year, by continually telegraphing a much tighter credit environment ahead. But the policy course was bailed out by the election of a new President and administration that is hell-bent on pumping up the economy.

Now Powell takes over at a more critical juncture. The execution on fiscal stimulus is beginning to materialize, and we’ll get to see how he navigates it. Hopefully, he’ll let the economy run a little hot (chase inflation from behind), and not allow rates (or the perception of tighter credit) to kill the animal spirits that can accompany big tax cuts and government spending programs.

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

The Fed decision today was a snoozer, as expected. The market continues to think we get a third rate hike for the year in December (fourth since the election).

Thus far, with three hikes, we’ve had just about the equivalent (just shy of 75 basis points) priced-in to the 10-year Treasury market. Yields popped from about 1.70% on election night (just about a year ago) to a high of 2.64%. We’ve had some swings since, but we sit now at roughly 2.40% (70 basis points higher over the past year).

We revisited yesterday, the prospects for some significant wage growth (and therefore inflation), with the fuel of fiscal stimulus feeding into an already tight (but underemployed) labor market.

The Treasury market isn’t pricing that scenario in, at all.

In fact, the yield curve continues to look more like a world that doesn’t fully believe fiscal stimulus is happening (or will happen), and does believe the Fed is more likely damaging the economy through its rate “normalization.”

That’s a bet that continues to underprice the prospects of fiscal stimulus. And, therefore, that’s a bet that continues to be disconnected from the message other key markets are sending. Over the past six months, we’ve talked the case for stocks to go much higher. We’ve talked about the opportunities in European and Japanese stocks (German stocks hitting new record highs and Japanese stocks nearing new 26-year highs today). We’ve talked a lot about the building bull market in commodities. We’ve talked about the positive signals that copper has been sending, as the leading indicator of a global economic turning point. We’ve talked about the outlook for much higher oil prices – oil hit $55 today. (July 30: Explosive Move Coming For Oil And Commodities Stocks).

And oil prices, whether the central banks like to admit it or not, heavily impact inflation, inflation expectations and policy making decisions.

With that, this next chart suggests that market interest rates are about to make a move (higher).

Source: Billionaire’s Portfolio

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Let’s take a look today at what fiscal stimulus might do to inflation.

The central banks have been able to boost asset prices. They’ve been able to restore stability so that people felt confident enough to hire, spend and invest again. But the scars from over-indebtedness have left demand weak. And because of that, despite the recovery of the unemployment to under 5%, the quality of jobs haven’t returned. And, therefore, the leverage to command higher wages hasn’t been there. That’s been the missing piece of the recovery puzzle.

And with that, we’ve had an ultra-low inflation recovery. That sounds great (low inflation).

But inflation at these low levels has had us (through much of the past decade) teetering on the edge of deflation. That’s bad news.

Among the many threats throughout the crisis period, a deflationary spiral was one of the Fed’s most feared. Central bankers can fight inflation (by raising rates). But they can’t fight deflation when consumer psychology takes over. When people hold on to their money thinking things will be cheaper tomorrowthan they are today, that mindset can bring the economy to a dead halt. It’s a formula that can become irreversible.

And that’s what has kept the Fed (and global central banks) sitting at ultra-low levels of interest rates – to keep the recovery momentum moving so that they don’t have to fight a deflationary spiral (as they have in Japan, unsuccessfully, for two decades).

Now, enter fiscal stimulus. We’re getting fiscal stimulus into an already tight employment market.

Real wages (employee purchasing power) has barely budged for two decades. Introducing big tax cuts and government spending into an economy that has low unemployment and the best consumer credit worthiness on record should pop demand. And that should finally give us some wage growth – maybe bigwage growth.

All of the inflationists that thought QE was going to cause hyper-inflation were wrong – they didn’t understand the severity and breadth of the crisis. Now, after global unlimited QE has barely moved the needle on inflation, the inflation hawks have been lulled to sleep. It may be time to wake them up.

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click hereto learn more.

Since the election, almost a year ago, we’ve talked about the great passing of the torch, from a monetary policy-driven global economic recovery (which proved dangerously weak and shallow) to a fiscal stimulus-driven recovery (which finally gives us a chance to return to trend growth).

Now, almost a year in, policy execution on the fiscal stimulus front is moving. The Fed has hiked rates three times. In the past week, the ECB has signaled the end of QE in Europe is coming. And this Thursday the Bank of England is expected to raise rates for the first time in a decade.

Again, if you can block out the day-to-day noise, this is all confirming the exit of the post-crisis deleveraging era of the past decade – it’s all playing out fairly close to script.

With that, I want to revisit my note from early January of this year, which argues the case for this “passing of the torch” and emphasizes the value of having some bigger picture perspective…

From my Market Perspectives piece: JANUARY 18, 2017

“Two weeks ago, in my daily Market Perspectives note, I talked about the five reasons, even at Dow 20,000, that stocks look extraordinarily cheap as we head into 2017.

Today I want to talk a bit more about the idea that the timing is right for a pop in economic growth.

For the past ten years, we’ve heard experts pontificate about ‘what inning we’re in,’ during the crisis era. I think there are good reasons to believe the game is over, and it was ended on election night–that was the catalyst.The policy responses and regime shift have more to do with the evolution of the global financial crisis and human psychology, than it does with the character behind it all.

I want to focus on a study from Carmen Reinhart and Kenneth Rogoff – the two economists that laid out the script, back in 2008, for precisely what the world has experienced over the past ten years. Fortunately, Bernanke was a believer in it. That’s why the Fed kept its foot on the gas, even in the face of a lot of scrutiny from people that blamed the Fed on extending the crisis.

Reinhart and Rogoff studied eight centuries of financial crises and they found striking commonalities in the aftermath. They found that financial crises tend to lead to sovereign debt crises. And sovereign debt crises tend to be contagious. Clearly, we’ve seen it.

Reinhart went on to look at the 15 severe financial crises since World War II and found that they were typically driven by credit bubbles. Check.

Importantly, they found that the credit bubble typically took as long to unwind (or de-lever) as it took to build. And the deleveraging period tends to mean ultra-slow economic activity as consumers, businesses and governments are paying down debt, not spending. And because of this, the research suggested that throughout this ten-year deleveraging period we should expect: 1) economic growth will trend at lower levels than pre-crisis growth, 2) housing prices will remain anywhere from 20% to 50% below peak levels and 3) unemployment will hover around 5% higher than pre-crisis levels. Check, check and check.

In the current case, Reinhart and Rogoff said the credit bubble was built over about a decade. That means we all should all have expected a decade long deleveraging period.

Now, with that, you can mark the top in the bubble as the 2006 housing top, or in 2007 when we the first big mortgage company and Bear Stearns hedge fund failed, or 2008, when consumer credit peaked. We’re somewhere in the middle of this window now and major turning points in markets tend to come with significant events. It’s a fair argument to make that the Trump election was a significant event for the world. With that, we may find that the crisis period officially ended with the election, when the history books look back on this current period of time.’

So that was my take back in January. It’s not easy to watch the process play out. It can be slow and ugly. But we’re seeing the reaction in stocks to this thesis – now at 23k in the DJIA. And we’re getting some momentum building on the policy making side that further supports this structural turning point is here (or has been here).

Join our Billionaire’s Portfolio subscription service today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We talked yesterday about the move in interest rates. We have the collision of two big events nearing for the interest rate markets.

Event number one, as we discussed yesterday, is the President’s decision on the next Fed chair. Event number two will come tomorrowmorning with the European Central Bank meeting. The ECB has been setting expectations for the eventual tapering of its QE program.

At this point, the market view is that Draghi and company will tell us their plans to extend the existing end date of QE, but with a methodical decline in the amount of assets they will be buying. Translation: It’s the beginning of the end of QE in Europe.

Why is that important? When the Fed (Bernanke) first uttered the words taper in May of 2013, U.S. yields went crazy – rising from 1.61% to 2.74% in two months, topping out just above 3% in the months following. Stocks were hit for about 8% in the month following the taper talk.

Could it happen in Europe? Likely. As we discussed yesterday, the 10 year yield there remains under 50 basis points, and 2 year government debt has a negative 70 basis points yield.

Will it hit stocks?

The world is in a different place now. And the ECB isn’t the Fed. But it’s safe to expect that there will be speculators with a finger on the trigger trying to sell stocks on an ECB taper theme, assuming that is discussed tomorrow.

With this in mind, ahead of tomorrow’s ECB meeting, we get this in stocks today…

You can see the trend break on this acceleration higher in stocks of the past two months. It wouldn’t be surprising to see stocks pull back a bit on these interest rate events. But any weakness on this type of speculation will be a nice opportunity to buy at cheaper prices in front of coming fiscal stimulus.

We’ve a lot about the positive outlook for stocks on a valuation basis, relative to historical ultra-low interest rate environments. And we’ve talked about the influence on valuation on a corporate tax cut – which will make stocks cheap.

Here’s a look at how stocks would look if we applied the long run average return of 8% to the pre-crisis peak (back in 2007). You can see the orange line, with the S&P growing at 8% annualized from the peak in 2007. And you can see the actual path for stocks in the blue line.

source: Billionaire’s Portfolio

Despite the nice run we’ve had in stocks, off of the bottom in 2009, we still have a big gap to make up (the difference between the blue line and the orange line)!

If you believe that the country will continue to innovate, become more efficient, productive and better, over time, as we have through history, and if you believe that we will ultimately return to long-term trend economic growth, then you believe that we’ll have hotter than average economic growth going forward. We have a catalyst for that: It’s fiscal stimulus.

And that hotter growth would argue for bigger than average stock market returns going forward, to put us back on the path of the long term growth rate in the S&P 500 – closing that gap in the chart above.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Forbes has just ranked the top 400 richest people in America for 2017.

Among the top 50, a fifth have created their wealth from some sort of Wall Street activity (mostly hedge funds, but also brokerage and asset management). There’s not much new there–the rich have gotten richer on Wall Street despite the challenges of the past decade. But as we’ve discussed, the torch was, in many respects, passed to Silicon Valley over the past decade, as the best spot to create–that’s where the biggest proportion of the wealthiest 50 have built their wealth.

But much of that technology wealth can be refined down to the very industries that are being displaced on the wealth list, such as publishing, energy and retail.

That makes you wonder how long some of these companies can command a software-like valuation when the core of their business models are rather traditional things like selling ads, distributing content, making cars or selling retail products.

To this point, as long as they started in Silicon Valley, they tend to get a very long leash. They can lose money with immunity.

Consider this: GM is valued at $66 billion. Telsa is valued at $57 billion. GM has made (net profit) $43 billion over the past six years. Tesla has lost$2.5 billion over the past six years. Meanwhile, Elon Musk, Tesla’s founder, has amassed a $20 billion net worth.

The question is how defensible are these businesses (Facebook, Netflix, Tesla, Twitter)? How wide is their moat? A couple of years ago, the answer was probably very wide–very defensible given the adoption, the scale, and the deep pocket investors that were willing to continue plowing money into them. But, as we’ve discussed, if the regulatory environment becomes less favorable and the money dries up (in the case of private companies, like Uber), the operating advantages can begin to evaporate. This bubble-up of regulatory scrutiny on tech is something to keep a close eye on. It may become one of the big themes in the coming year.

Interest rates and stocks are on the move today (higher), following the vote last night in the Senate to pass the budget. This opens the way for an approval on the tax plan.

As stocks continue to print new record highs, so does policy execution for the Trump administration (the latter the cause, the former the effect).

So we’re seeing more and more of the pro-growth plan fall into place. Markets have been telling us this (betting on this) for a while.

Remember, we talked about the prospects that hurricane aid could kickstart the Trump infrastructure plan (proposed at $1 trillion over 10 years). There’smore progress on that front in the past week.

Among the pillars of Trump’s growth plan, this one (infrastructure/government spending) looked to be among the long shots given the politicians can always play the debt card to fight it. But then the hurricanes hit.

After Irma rolled through Florida the estimated damages for both Harvey and Irma were estimated at $200 billion. Then Hurricane Maria decimated Puerto Rico. Estimated damages there are now $95 billion. I’ve thought we’ll ultimately see a 12-figure package out of Congress in response to the hurricanes. The ultimate federal aid on Katrina was $120 billion.

In September Congress approved $15 billion in aid for hurricane victims. They just approved another $35 billion! This quiet government spending piece, that will substantially grow from here, may turn out to be the most powerful in terms of driving wage growth and economic growth.

So tax reform and infrastructure, two big pillars of Trumponomics continue to progress. And on the deregulation front, Trump has already been aggressively peeling back regulations that have crushed some industries, while ramping UP regulatory scrutiny on Silicon Valley, as we discussed yesterday.

Some of the top venture capitalists in Silicon Valley said this week that they expect to see some failures this year of startups once valued north of a billion-dollar. That’s a result of less money flowing that direction, less government favor, and more money flowing back into publicly traded stocks.

With that in mind, let’s take a look at the chart on Amazon to finish the week …

We talked about Amazon’s miss on earnings back on July 27th as the catalyst to take profit on the FAANG trade (the loved tech giants). The top continues to hold in Amazon.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Yesterday we talked about the case for commodities and the opportunity for a rotation into commodities stocks.

The valuation of commodities relative to stocks has only been this disconnected (stocks strong, commodities weak) twice, historically over the past 100 years: at the depths of the Great Depression in the early 30s and toward the end of the Bretton Woods currency system.

That supports the case that we’re in the early days of a bull market in commodities, especially considering where we stand in the global economic recovery, underpinned by the “reflation” focus at both the monetary and fiscal policy levels. It’s a recipe for hotter demand for commodities.

With that, let’s take a look at a few charts as we close the week.

Copper

We talked about copper yesterday. This continues to ring the bell, alerting us that better economic growth is coming – maybe a boom.

Copper is up 6.5% in the past two weeks, back of $3 and closing in on the highs of the year – which is a three year high. And remember, we looked at the potential break of this big six-year downtrend back in August. That has broken, retested and confirms the trend change.

Crude Oil

We talked about the fundamental case for oil this week. And we looked at the technical case, as it made a brief test of the 200 day moving average and quickly bounced back. It’s up about 4% on the week.

We have this inverse head and shoulder (in the chart below) that projects a move back to the low $80s. And as part of that technical picture, we’re setting up for a break of a big two-year trendline that should open the doors to a move back into the $70+ oil area.

Iron Ore

Iron ore was the biggest mover of the day – up 6% today. This has been a deeply depressed market through the post-financial crisis era. In addition to the broad commodities weakness, iron ore prices have suffered from the dumping of poor quailty iron ore by Chinese producers. Those times seem to be changing.

This week there was a fraud claim on a big Japanese steel maker for fudging it’s quality data. Keep an eye on this one as it could lead to more, and could lead to a supply disruption in industrial metals.

Then today we had Chinese data that showed record imports of iron ore. This is a signal that there’s both an envirionmental movement and an anti-dumping movement against low grade iron ore that has been influencing supply and prices (and crushing producers). This big Chinese data point is also in line with the message copper is sending: perhaps the Chinese economy is doing better than most think.

With that, let’s take a look at a few charts as we close the week. The valuation of commodities relative to stocks has only been this disconnected (stocks strong, commodities weak) twice, historically over the past 100 years: at the depths of the Great Depression in the early 30s and toward the end of the Bretton Woods currency system.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

For much of the summer, while the world has been obsessed with Trump tweets, we’ve talked about the sharp but under-acknowledged move in copper and the message it was sending about the global economy and China (the biggest consumer of commodities), specifically. As I’ve said, people should Stop Watching Trump And Start Watching Copper.

Why copper? It is often an early indicator of economic cycles. People love to say copper ‘has a Ph.D. in economics’ because it tends to top early at economic peaks and bottom early at economic troughs. And it tends to lead a bull market in broader commodities.

Well, copper bottomed on January 15. Fast forward to today; the most important industrial metal in the world is up 24% on the year and sniffing back toward three-year highs. While the world continues to focus on Washington drama, this continues to be the proverbial “bell” ringing to signal a pop in economic growth is coming, and a big run for commodities investors is ripe for the taking.

With that in mind, we’ve talked in recent days again about the research from the top minds in commodities investing, Leigh Goehring and Adam Rozencwajg (managers of the commodities funds, ticker GRHIX and GRHAX). We know they like oil. In fact they think we see triple-digit oil prices by early next year.

They love the commodities trade in general. They have one of the most compelling charts I’ve seen in my 20-year career, to support the view that there is a generational bull breaking lose in commodities.

Stocks minted billionaires in the 1980s. Currencies minted billionaires in the 1990s. Tech and housing (bust) minted billionaires in the early 2000s. Then it was equity activism (stocks). The next opportunity looks like commodities.

In this chart below you can see, as Goehring and Rozencwajg say, commodities are as cheap today as they have ever been. “Only in the depths of the Great Depression and at the end of the dying Bretton Woods Gold Exchange Standard did commodities reach this level of undervaluation relative to equities.”

With this, they say, for those that can block out the noise, “there is a proverbial fortune to be made if they invest today.”

Here’s an excerpt from their most recent investor letter on their work on the stocks to commodities valuation:

“When commodities are this cheap relative to stocks, the returns accruing to commodity investors have been spectacular. For example, had an investor bought the Goldman Sachs Commodity Index (or something equivalent) in 1970, by 1974 he would have compounded his money at 50% per year. From 1970 to 1980 commodities compounded anually in price by 20%. If the same investor had bought commodities in 2000, he would have also compounded his money at 20% for the next ten years–especially attractive considering the broad stock market indicies returned nothing over the same period.”

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

Oil is up over 3% today, trading up to the highest levels since June of 2015.

Oil is up over 3% today, trading up to the highest levels since June of 2015.

Let’s take a look today at what fiscal stimulus might do to inflation.

Let’s take a look today at what fiscal stimulus might do to inflation. Since the election, almost a year ago, we’ve talked about the great passing of the torch, from a monetary policy-driven global economic recovery (which proved dangerously weak and shallow) to a fiscal stimulus-driven recovery (which finally gives us a chance to return to trend growth).

Since the election, almost a year ago, we’ve talked about the great passing of the torch, from a monetary policy-driven global economic recovery (which proved dangerously weak and shallow) to a fiscal stimulus-driven recovery (which finally gives us a chance to return to trend growth). Forbes has just ranked the top 400 richest people in America for 2017.

Forbes has just ranked the top 400 richest people in America for 2017. Interest rates and stocks are on the move today (higher), following the vote last night in the Senate to pass the budget. This opens the way for an approval on the tax plan.

Interest rates and stocks are on the move today (higher), following the vote last night in the Senate to pass the budget. This opens the way for an approval on the tax plan.

Yesterday we talked about the case for commodities and the opportunity for a rotation into commodities stocks.

Yesterday we talked about the case for commodities and the opportunity for a rotation into commodities stocks.

Iron Ore

Iron Ore

The Fed decision today was a snoozer, as expected. The market continues to think we get a third rate hike for the year in December (fourth since the election).

The Fed decision today was a snoozer, as expected. The market continues to think we get a third rate hike for the year in December (fourth since the election).

We talked yesterday about the move in interest rates. We have the collision of two big events nearing for the interest rate markets.

We talked yesterday about the move in interest rates. We have the collision of two big events nearing for the interest rate markets.